- Higher production, imports expand supply

- Rising carryover stocks may limit price upside

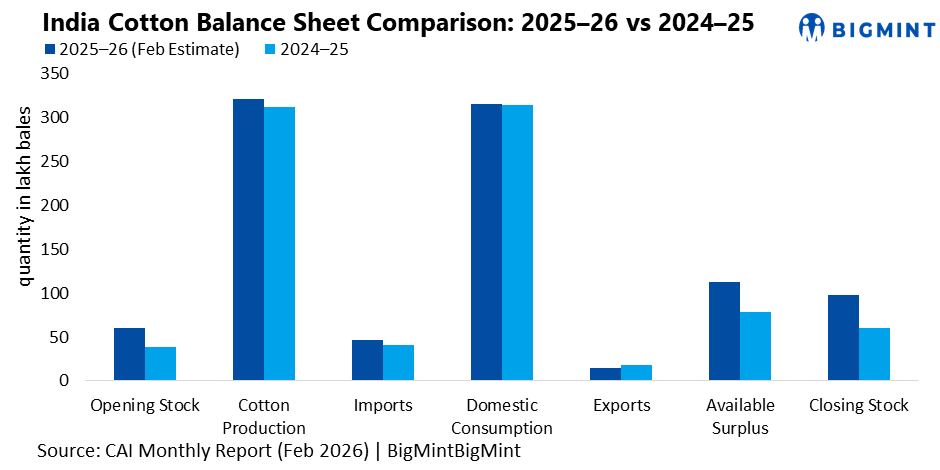

India’s cotton market for the 2025-26 season is moving toward a comfortable supply situation as production estimates have been revised upward, and overall availability remains significantly higher than last year. According to the latest monthly report released by the Cotton Association of India (CAI), overall cotton supply for the 2025-26 season is estimated at 428.09 lakh bales, significantly higher than 392.59 lakh bales recorded last year. This rise is supported by higher opening stocks, increased production, and larger imports.

As a result, the available surplus is estimated at 113.09 lakh bales, sharply higher than 78.59 lakh bales last season. Due to this comfortable supply scenario, as well as slower exports and only a marginal improvement in consumption, the projected closing stock is expected to reach 98.09 lakh bales, up by 37.50 lakh bales compared with last year’s closing stock of 60.59 lakh bales.

Moreover, India’s cotton pressing estimate for the ongoing season has been increased to 320.50 lakh bales, up by 3.50 lakh bales from the previous estimate and about 8.10 lakh bales higher y-o-y. This increase has largely been driven by improved production in Maharashtra and Andhra Pradesh, which offset reductions in northern states such as Punjab and Rajasthan.

On the demand side, domestic consumption has been revised upward to 315.00 lakh bales, compared with 305.00 lakh bales estimated earlier. However, the y-o-y increase in consumption is marginal, rising by only 1 lakh bales compared with 314.00 lakh bales last season. This suggests that while spinning millers have marginally increased raw cotton intake, overall yarn and textile demand growth remains moderate. Up to 28 February 2026, India had already consumed 131.25 lakh bales, reflecting steady offtake from spinning mills during the peak processing period.

Imports continue to play a significant role in the current season. Cotton imports are now estimated at 47.00 lakh bales, slightly lower than the earlier estimate of 50.00 lakh bales but still 6 lakh bales higher than the previous season’s imports of 41.00 lakh bales. By the end of February 2026, India had already imported 36.00 lakh bales, highlighting the continued reliance on foreign cotton, particularly for quality requirements and price arbitrage in the international market.

In contrast, exports remain relatively subdued. The export estimate for the current season is maintained at 15.00 lakh bales, lower than the 18.00 lakh bales exported in 2024-25. This indicates that India’s cotton prices are currently less competitive in the global market compared with major exporters such as Brazil and the United States. With only 7.00 lakh bales exported up to February, the pace of shipments remains slow, which could add to domestic availability in the coming months.

Outlook

For ginners and traders, the current balance sheet suggests that the domestic market will remain well supplied through the remainder of the season. The higher surplus and large carryover stocks could limit strong price rallies unless export demand improves or production revisions emerge later in the season. For spinning millers, however, the comfortable availability of cotton may provide stable raw material access and relatively controlled input costs in the months ahead.

Leave a Reply