- Korean buyers pay premiums over India

- Indian buyers remain selective amid liquidity stress

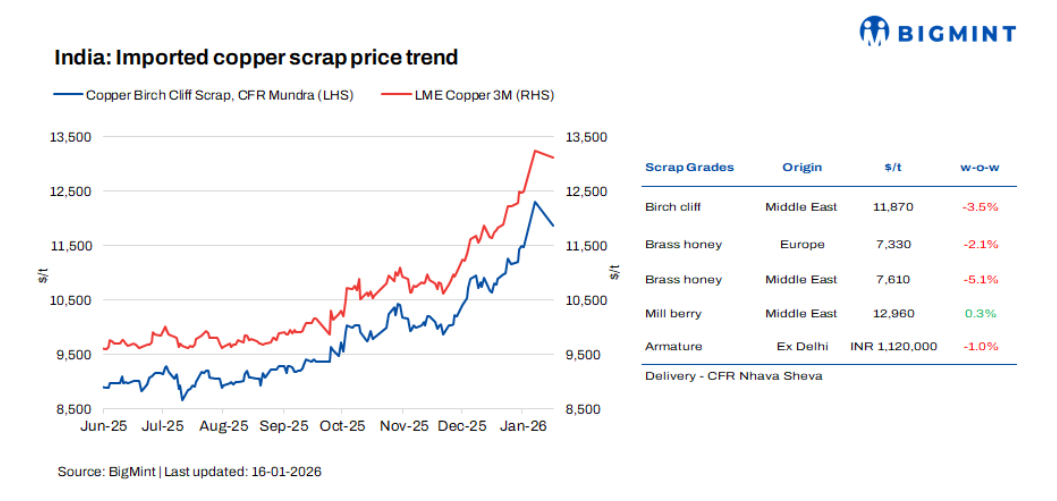

Imported copper scrap prices in India fell w-o-w in the week ended 16 January tracking a mild correction in London Metal Exchange (LME) copper futures. Meanwhile, domestic copper scrap prices showed mixed trends w-o-w.

According to BigMint’s assessment, Birch Cliff scrap was assessed at $11,870/t, down by 3.5% w-o-w, while US motors mix stood at $1,410/t (both CFR Mundra), slightly up by 1% w-o-w.

LME copper eases after recent highs

LME three-month copper prices corrected slightly after scaling recent highs earlier in the month. The benchmark contract settled at $13,106/t on 15 January 2026, down from the all-time high of $13,238/t on 7 January, though still significantly above the $12,497/t level seen on 1 January. The recent pullback follows profit-taking at elevated levels, even as overall sentiment remains supported by strong global cues and improved post-holiday trading activity.

Imported market scenario

Copper scrap prices in India remained largely stable this week, supported by elevated LME levels, as western suppliers returned to the market following New Year holidays. Fresh trade discussions resumed after a prolonged festive lull; however, offers mostly stayed rangebound, reflecting caution amid uneven physical demand despite stronger exchange cues.

Market participants noted a divergence in regional buying appetite. Korean buyers were reportedly paying premiums of $150-200/t above prevailing Indian levels for premium-grade copper scrap, underscoring stronger demand in Northeast Asia. In contrast, Indian buyers remained selective, with deal activity improving only gradually amid persistent liquidity constraints.

Imported scrap offers showed limited movement. EU-origin Bare Bright was heard at around 97.6% of 3M LME on a CIF China basis, while Candy Berry was indicated at 95.2% of LME and Birch/Cliff at 91.5%.

From the UAE, Birch/Cliff was offered at approximately 91.5% of 3M LME CIF Mundra, Brass Honey (4% impurities) at around 59% of LME, and Millberry at about 98.5% of LME.

Indian market updates

Domestic copper scrap market activity remained subdued, constrained by tight working capital availability and delayed receivables across key consuming hubs. Environmental restrictions in parts of north India further limited operating rates, reducing the ability of buyers to fully pass on higher global prices into the domestic market.

Armature scrap deals in the domestic market were reported around INR 1,130/kg ex-Delhi, supported by steady plant-level demand. However, sellers remained cautious, as persistent payment delays continued to weigh on confidence and restricted spot availability.

Demand from wire rod and copper alloy segments stayed stable but price-sensitive, keeping overall market sentiment cautious despite firm global cues. Traders noted that while interest has picked up following the holiday period, buyers are largely avoiding aggressive stocking and are focusing on hand-to-mouth procurement.

Outlook

While elevated LME levels and stronger demand from Northeast Asia are lending underlying support, domestic market sentiment continues to be tempered by liquidity constraints, delayed payments, and regulatory challenges. High-grade imported scrap may see selective buying, but broader price upside is likely to remain limited unless domestic cash flows and operating conditions improve.

Leave a Reply