- Copper scrap prices firm on tight supply, strong demand

- CCR plants, smelters shift strategy amid rising cost

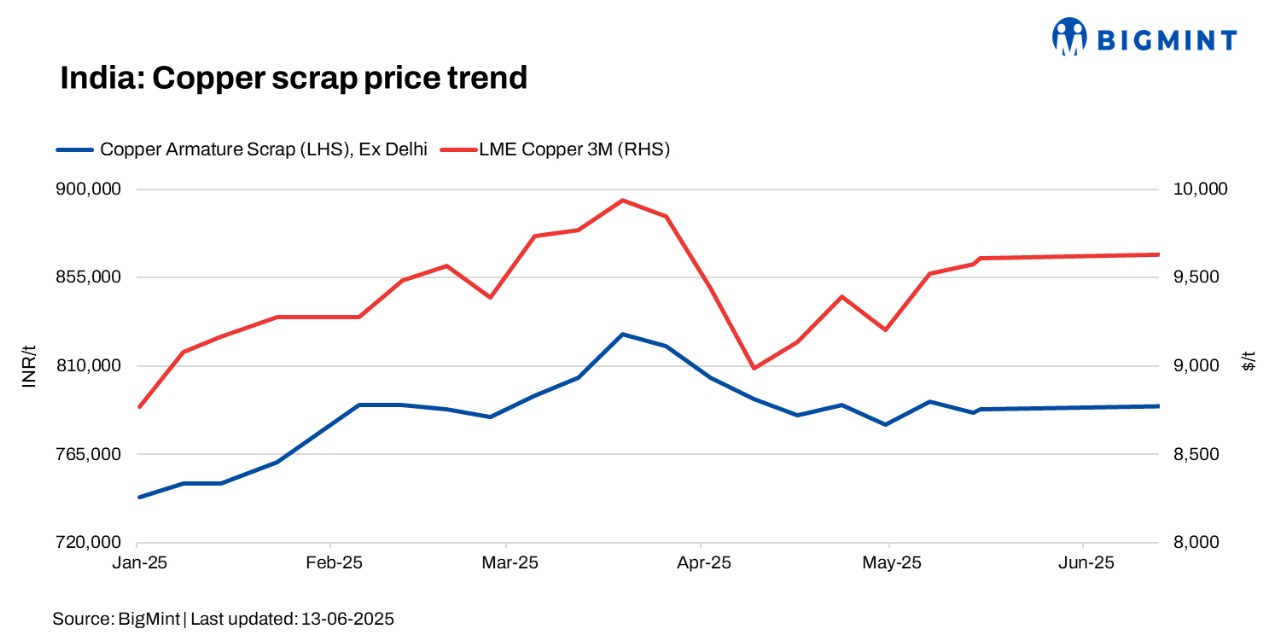

Indian copper scrap prices showed an uptrend this week, despite diverging trends prevailing on the London Metal Exchange (LME) platform. Copper armature scrap was assessed at INR 805,000/tonne (t) ex-Delhi, while motors mix was stable w-o-w at $1,160/t.

LME futures went down by $150/t to $9,590/t compared with last week’s $9,740/t. Meanwhile, copper stocks at LME-registered warehouses stood at 120,400 t, down 18,000 t compared to 138,000 t the previous week.

Secondary continuously cast rods (CCRs) (99.90%) were assessed at INR 868,000/t ex-Delhi, marginally up w-o-w. Meanwhile, primary CCR prices stood at INR 900,000/t, rising by up to 12,000/t w-o-w.

Global copper prices are climbing as primary supply faces pressure from declining ore quality. Global copper ore grades have steadily fallen averaging around 0.5% in 2022 compared to over 0.6% a decade ago-forcing miners to extract and process more material for the same yield. This has raised production costs and lowered refined output.

Market insight

Copper scrap demand remains strong, with buyers actively purchasing in expectation of further price increases.

Imported scrap inflows tight

Copper scrap inflows from the UAE and Europe have reduced as sellers prefer higher-paying markets like Pakistan and Southeast Asia. As a result, offers for Millberry copper scrap CIF India have strengthened to 100.5- 101% of LME. Fewer bulk shipments are reaching Indian ports, causing tightness in the imported scrap market.

Traders note that Pakistan is offering significantly better returns for copper motor scrap-reportedly $70-85/t above Indian prices-leading suppliers to prioritise exports. Simultaneously, Chinese buyers are quoting up to 98.5% for Candy/Berry grades, further boosting export demand from Australia. In contrast, Millberry copper remains steady in the Indian market, trading at par or with marginal premiums over LME. Australian-origin Millberry was heard at 100.5% LME, indicating tight supply and strong international sentiment.

Smelters holding back sales

Domestic recyclers are reportedly holding onto stock, anticipating further price increases after copper on the LME crossed $10,000/t in early June. This cautious selling behaviour is adding to the supply crunch in the Indian market.

A trader source stated: “Continuous Cast Rod (CCR) manufacturers in India, especially in hubs like Bhiwadi and Daman, have moved away from long-term fixed pricing and are now offering weekly or bi-weekly rates to Original Equipment Manufacturers (OEMs) producing fan motors, alternators, and other electrical components. This shift helps CCR plants avoid potential losses from sudden copper price surges, while OEMs benefit by making smaller, more flexible purchases that reduce their exposure to market volatility”.

Scrap imports hit 5-month high

India’s copper scrap imports rose to nearly 30,800 t in April, marking the highest monthly inflow since November 2024, when volumes stood at around 31,100 t.

After the fiscal yearend, demand has picked up from the wire and cable industry, especially from power utilities and the EV sector. Manufacturers are buying more Berry and Candy scrap to meet high conductivity needs. At the same time, secondary smelters in Delhi, Bhiwadi, Daman, and Ludhiana are restocking Birch/Cliff and ICW scrap to supply construction and informal electrification markets. This shift in grade-wise demand is guiding Q2 buying plans.

Outlook

The Indian copper scrap market is likely to stay supported in the near term, with steady demand from secondary smelters and CCR manufacturers. Limited scrap availability and cautious selling by traders may sustain upward pressure on prices. Market participants expect continued competition for quality grades like Berry, Candy, and Millberry, which could keep domestic premiums elevated despite global prices remaining volatile.

Leave a Reply