- Higher grades see sharp gains tracking LME rise

- Buyers cautious despite positive price outlook

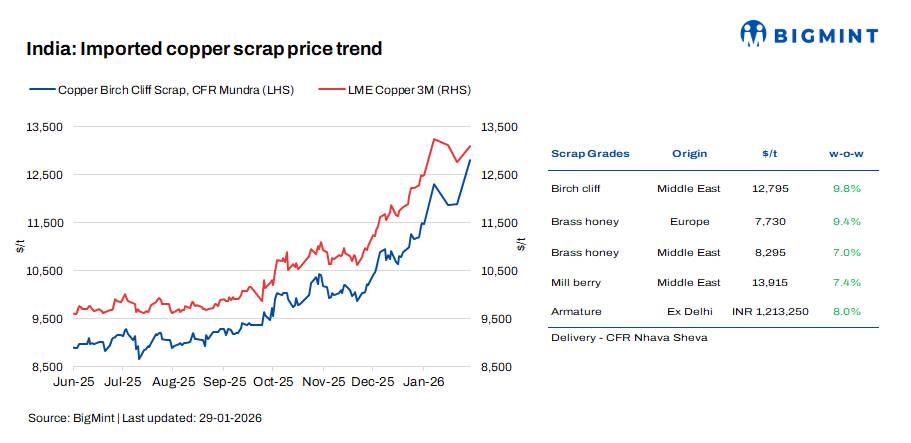

Imported copper scrap prices in India recorded a strong upswing w-o-w, in the week ended 29 January, tracking a rebound in benchmark copper futures on the London Metal Exchange (LME). Domestic copper scrap prices also moved higher, supported by firm replacement costs and improving market sentiment, though buying activity remained measured.

According to BigMint’s assessment, Middle East-origin Birch Cliff scrap was assessed at $12,795/t CFR Mundra, up sharply by 9.8% w-o-w. Brass Honey prices also rose across origins, with European-origin material assessed at $7,730/t, up 9.4% w-o-w, while Middle East-origin Brass Honey increased 7% w-o-w to $8,295/t. Millberry prices surged 7.4% w-o-w to $13,915/t. In the domestic market, armature scrap prices jumped 8% w-o-w to INR 1,213,250/t ex-Delhi.

US motors mix prices also strengthened notably, rising 3% w-o-w to around $1,500/t CFR Mundra from $1,450/t last week, reflecting firm demand for motor scrap despite higher offer levels.

LME copper rebounds

LME three-month copper prices rebounded during the week, rising 2.6% to $13,087/t on 29 January, up from $12,754/t on 21 January. The recovery followed improved market sentiment and renewed buying interest after a correction registered in the previous week. Meanwhile, LME copper inventories rose to 173,925 t from 159,400 t over the same period, partially tempering bullish momentum, though participants continue to cite expectations of further upside amid supportive global cues.

Imported market scenario

Imported copper scrap prices in India firmed sharply this week, driven by higher LME prices and strong replacement costs. Market participants noted that higher-grade scrap continued to command significant premiums, with sellers pushing offers higher in line with the exchange-led rally.

Despite the price rise, buying interest remained cautious, as consumers were reluctant to book large volumes at prevailing elevated levels. However, overall sentiment turned positive, with many participants anticipating further upside in copper prices in the near term.

Motors scrap demand stayed firm, with trades reported around $1,500/t, even as buyers focused on smaller, hand-to-mouth purchases. Market sources indicated that while inventories remain manageable, higher LME prices have lifted overall scrap valuations.

Indian market updates

Domestic copper scrap market activity improved w-o-w, supported by higher global prices and firm demand. However, traders highlighted that Indian buyers remain selective, preferring short-term procurement strategies rather than bulk stocking, despite the improving price outlook.

Global market updates

Global copper supply remained mixed, with major producers reporting lower full-year output despite a strong second-half recovery.

Glencore’s copper production fell 11% y-o-y to 851,600 t in 2025, pressured by lower ore grades and recoveries at Collahuasi, Antamina, and Antapaccay. However, H2 output rebounded nearly 50% over H1, offering near-term supply support.

Antofagasta reported strong Q4 output of 177,000 t, up 9% q-o-q, though full-year production slipped 1.6% y-o-y to 653,700 t. Net cash costs dropped 27% to a five-year low of $1.19/lb, while 2026 output is guided at 650,000-700,000 t.

Outlook

Indian copper scrap prices are likely to remain firm in the near term, supported by higher LME copper prices, strong replacement costs, and improving market sentiment. While buying activity may stay cautious due to elevated prices and liquidity challenges, higher-grade scrap is expected to continue trading at a premium. Market participants remain watchful of LME movements, with further upside potentially drawing in stronger buying interest.

Leave a Reply