- UAE export restrictions add to scrap market uncertainty.

- India seeks EU relief over scrap export policy.

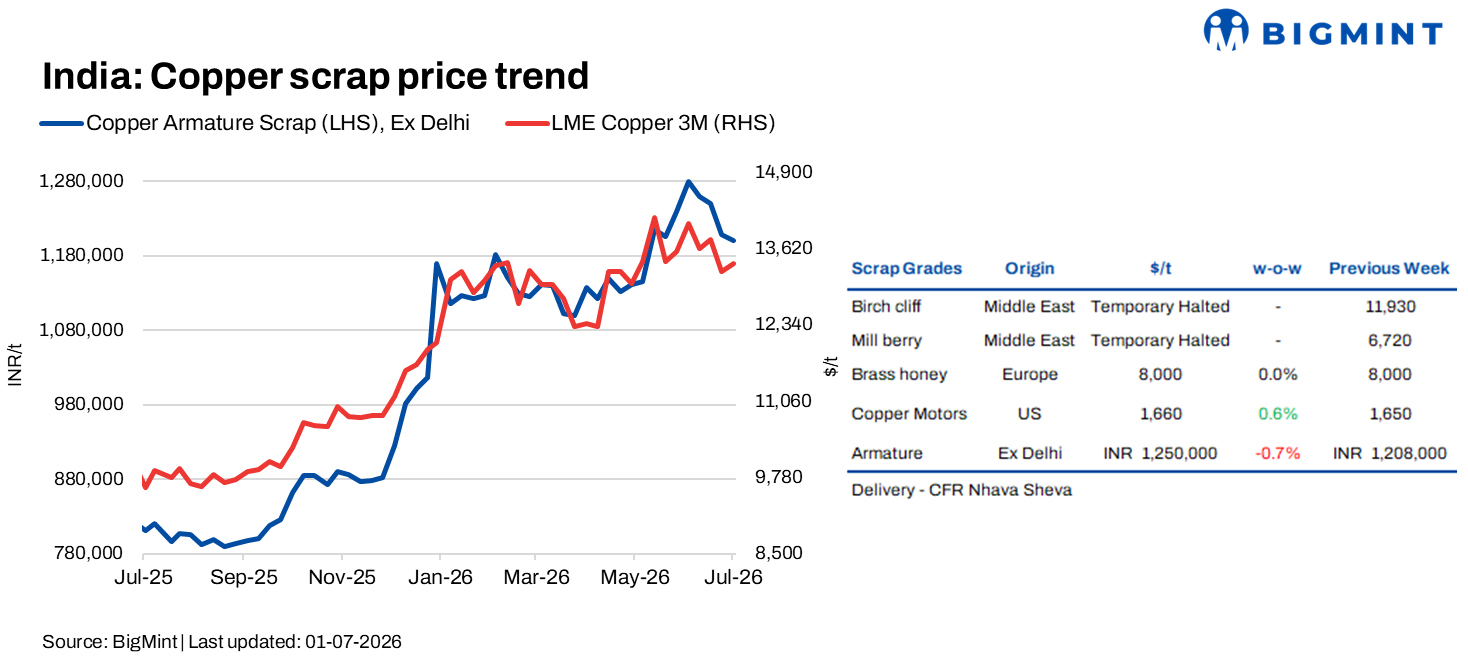

Copper scrap prices in India remained largely stable w-o-w on 1 July 2026, with only marginal fluctuations as weak domestic demand offset the recovery in benchmark prices. London Metal Exchange (LME) copper prices fell to around $13,050/t from nearly $13,300/t early in the week before rebounding to approximately $13,350/t by month-end, supported by stronger China’s manufacturing PMI. However, gains remained limited amid expectations of prolonged higher US interest rates and uncertainty over proposed US copper import tariffs.

At the domestic level, buying activity remained largely requirement-driven across major trading hubs. According to BigMint’s assessment, copper armature scrap, ex-Delhi, remained largely stable w-o-w, edging down by around 0.7% to INR 1,200,000/t from INR 1,208,000/t.

Market insight

Market participants indicated that trading activity remained sluggish across major copper scrap grades, with buyers continuing to procure material only against immediate production requirements. Weak downstream demand has reduced raw material consumption, as manufacturers and secondary smelters continue to receive fewer orders from end-users.

Sources said a majority of consumers had already booked both imported and domestic scrap at relatively higher prices in previous weeks, limiting the need for fresh purchases despite recent price corrections. The decline in copper prices also put pressure on traders holding high-cost inventories, resulting in cautious procurement and limited spot market activity.

Market participants said uncertainty surrounding the proposed US copper import tariffs, coupled with the UAE’s export restrictions on aluminium and copper scrap, continued to weigh on market sentiment. Premium imported scrap grades witnessed limited acceptance as buyers remained cautious amid weak downstream demand and volatile prices.

Trading activity in locally available scrap grades also slowed, with purchases largely restricted to immediate requirements. Meanwhile, traders and scrap yard owners preferred to hold inventories while awaiting better price clarity and improved demand.

EU scrap export curbs may tighten India’s import options

Meanwhile, market participants are closely monitoring the European Union’s proposed restrictions on metal scrap exports, which could tighten the availability of imported scrap for Indian consumers from May 2027. Under the revised Waste Shipment Regulation, exports of non-hazardous scrap to non-OECD countries would require EU approval, potentially limiting supplies of quality recyclable material.

India has reportedly sought relief from the proposed measures, with industry bodies urging the EU to consider export quotas instead of a complete restriction. Stakeholders believe the move could otherwise increase procurement costs and reduce the availability of imported ferrous and non-ferrous scrap for domestic recyclers and manufacturers.

The concerns have intensified following the UAE’s recent restrictions on aluminium scrap exports, with market participants warning that multiple export controls could further tighten global scrap availability. Industry representatives also highlighted that growing resource nationalism across major exporting countries may increase competition for recyclable metals, including copper.

Going forward, the immediate impact on the Indian copper scrap market is expected to remain limited due to subdued domestic demand. However, market participants believe tighter global scrap flows and evolving trade policies could increase procurement costs and influence import sourcing strategies over the medium to long term.

Deals level heard

- Armature scrap Ex Delhi at INR 1200/kg

- USA Large motors at $1410/t CIF West coast

- USA Candy berry at 97.5% CIF Nhava sheva

- Spain-origin alternators traded at $2,650/t CIF India

- USA-origin alternators traded at $2,750/t CIF India

- USA-origin starters traded at $1,940/t CIF India

Outlook

The Indian copper scrap market is expected to remain slow in July as buying interest stays weak. Dismantlers may continue to face difficulty selling processed scrap, while manufacturers and secondary smelters are likely to purchase only for immediate requirements due to limited order bookings.

Adequate material availability in the domestic market is expected to keep fresh procurement under pressure. Traders holding inventories may avoid aggressive buying until existing stocks are cleared and demand from end-users improves.

Leave a Reply