- Hopes of post-monsoon demand recovery keep scrap buying steady

- UAE, Europe cap exports to India amid better margins in Pak, SE Asia

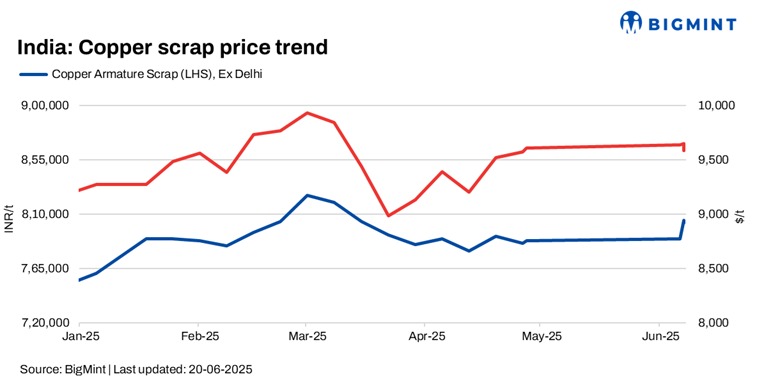

Indian copper scrap prices moved in a narrow range w-o-w, despite a drop in London Metal Exchange (LME) futures. Copper armature scrap was assessed at INR 803,000/tonne (t) ex-Delhi, down by INR 2,000/t w-o-w, while motors mix was stable w-o-w at $1,150/t.

LME futures fell by $58/t to $9,587/t compared with last week’s $9,645/t. Meanwhile, copper stocks at LME-registered warehouses stood at 103,325 t, down by roughly 11,000 t compared to 114,475 t the previous week.

Secondary continuously cast rods (CCRs) (99.90%) were assessed at INR 866,000/t ex-Delhi, up marginally w-o-w. Meanwhile, primary CCR prices stood at INR 905,000/t, range-bound w-o-w.

Market scenario

Copper scrap demand remained firm, as buyers continued to procure material in expectation of a post-monsoon demand recovery. Many stocked up ahead of the seasonal uptick expected once the rains subside. However, tradeable quantities remained limited during the monsoon, with supply tightness keeping spot availability constrained, especially for high-conductivity grades such as Berry and Millberry. This cautious buying and holding strategy shaped short-term market behaviour.

Millberry offers, CIF India, firmed up to 100.5-101% of LME, even as LME copper hovered near $9,580/t. This strength in offers was primarily driven by reduced inflows from traditional suppliers such as the UAE and Europe, who diverted material to higher-paying destinations such as Pakistan and Southeast Asia. These regions offered better realisations – up to $70-85/t higher in some cases – prompting exporters to prioritise those markets. At the same time, limited scrap generation and cautious selling by traders expecting further price gains tightened availability, supporting firmer offers to India despite LME’s slight dip.

A source stated, “Mills across Europe are struggling with tight supply as many sellers have already diverted shipments to the US, where they are fetching higher prices. With several suppliers running out of stock for cathodes, many buyers are now turning to copper scrap as an alternative. This has pushed up scrap demand and narrowed the usual price discounts between cathode and scrap grades, especially as clean high-grade scrap becomes harder to find.”

A significant drawdown of copper from LME and COMEX warehouses occurred in the first five months of 2025. This was largely driven by fears that former US President Donald Trump may reintroduce steep import tariffs on copper, prompting traders to move material quickly into the US ahead of any policy shift.

Additionally, US imports of refined copper surged to over 200,000 t in April 2025, marking the highest monthly import volume this decade, according to sources. This significant spike reflects the strong demand pull from the US market, largely driven by ongoing tariff-driven arbitrage and restocking needs across industries.

Outlook

The Indian copper scrap market is expected to remain firm in the near term, driven by consistent demand from secondary smelters and CCR manufacturers. With scrap availability tight and traders holding back sales, prices are likely to stay under upward pressure. Strong competition for high-grade scrap such as Berry, Candy, and Millberry may continue to support elevated domestic premiums, even as global price trends remain uncertain.

Leave a Reply