- Supply crunch in premium grades outweighs weaker LME prices

- Container shortages, Far East demand limit material inflows

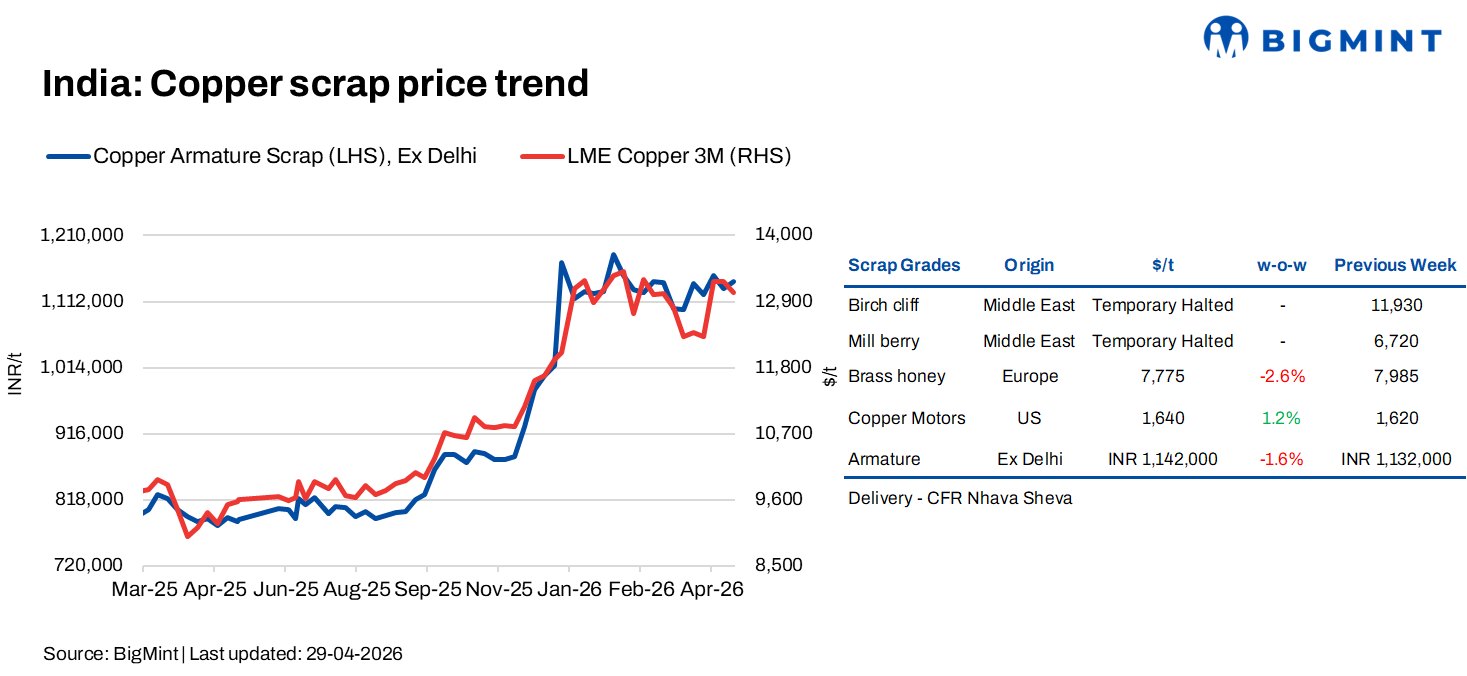

Copper scrap prices in India rose slightly w-o-w on 29 April, despite weaker London Metal Exchange (LME) prices, which stood at around $13,037/t, down by $194/t from last week’s $13,231/t. The decline in global prices had limited pass-through to the domestic market, as tight scrap inflows, constrained import availability, and steady secondary-sector demand continued to support sentiment, while spot liquidity remained selective.

At the domestic level, copper scrap prices remained firm, as buyers continued to secure material amid steady demand from secondary consuming sectors and tight spot availability. According to BigMint’s assessment, copper armature scrap, ex-Delhi, was assessed at INR 1,142,000/t, up by INR 10,000/t from INR 1,132,000/t in the previous week.

Market scenario

The Indian copper scrap market remained firm, supported by steady demand from recyclers, cable, wire rod, and secondary manufacturers. However, tight scrap availability, particularly in premium grades, continued to keep buyers under sourcing pressure.

Market participants noted that container availability from the Middle East to India remained constrained, with limited firm bids and offers being heard from the region, further tightening domestic supply conditions. In addition, concentrate shortages at the mining level continued to support scrap demand, as buyers increasingly relied on secondary raw materials to bridge supply gaps.

Material flow into India remained uneven, with a sizeable portion of good-quality scrap being diverted to Far East markets due to better realisations. This reduced domestic availability and intensified competition for prompt cargoes. Trade sources also highlighted increasing scrutiny of premium grades such as Birch/Cliff and Berry/Candy in overseas markets due to a mismatch between declared and actual material. Instances of mixed wires and higher impurities led to clearance delays, indirectly affecting availability in India.

Tight scrap availability and selective inventory management continued to restrict material flow. In the imported scrap segment, brass honey from Europe was assessed at 59.5% of 3M LME CFR Nhava Sheva, down from 60% last week, while US-origin copper motors scrap deals were heard in the range of $1,570-1,600/t against $1,620/t last week, with offers reported up to around $1,670/t, reflecting the ongoing tightness in the market.

European copper scrap premiums moved higher during the week, supported by improved second-quarter spot liquidity and fresh restocking demand despite softer LME prices. Berry/Candy rose to 95-96% of 3M LME, Millberry to 96.5-97.5%, while Birch/Cliff remained steady at 89.5-90.5%. Tighter prompt availability in Europe may continue to support global scrap premiums for Indian buyers.

Domestic consumers continued to seek regular supply, but tight inflows and quality-related uncertainties restricted smooth procurement. Buyers were either accepting higher offers or shifting towards lower grades to maintain production continuity. Unless supply conditions improve, copper scrap prices are expected to remain supported in the near term.

Outlook

BigMint expects the copper scrap market to remain firm in the near term, with sentiment driven by steady domestic demand and tight physical availability. Limited inflows of premium grades, constrained Middle East container availability, and selective procurement are likely to keep prices supported, although softer LME movements may cap sharper upside.

In the imported segment, firm overseas offers, elevated global scrap premiums, quality-related scrutiny, and freight uncertainties may continue to restrict fresh bookings. Global copper prices will remain sensitive to concentrate supply disruptions and exchange inventory trends, keeping the domestic copper scrap market sideways to mildly firm in the near term.

Leave a Reply