- Monsoon dampens trade momentum this week

- Global markets remain firm amid tight supply

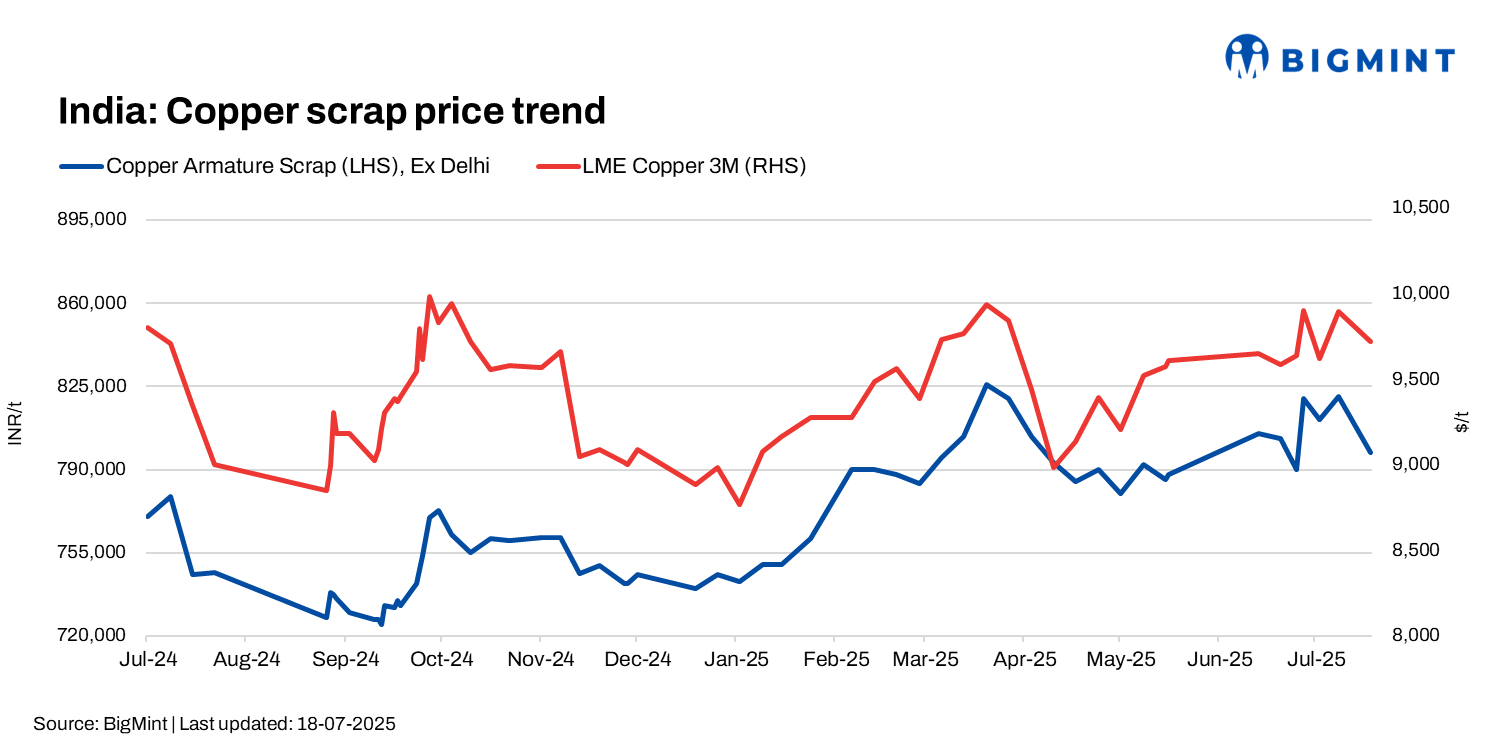

Indian copper scrap prices moved down further w-o-w, as London Metal Exchange (LME) futures remained lower than the three-month high of $10,005/t recorded on 3 July. Copper armature scrap was assessed at INR 797,000/tonne (t) ex-Delhi, down by 1.6% w-o-w, while motors mix stood at $1,150/t, down $10/t w-o-w.

Copper prices on the LME edged up by a minor $46/t w-o-w to $9,666/t, supported by persistent supply constraints and growing uncertainty over potential US import tariffs. However, the downtrend from early-July highs has pressured domestic prices since last week.

Secondary continuously cast rods (CCRs) (99.90%) were assessed at INR 850,000/t ex-Delhi, down 2.7% w-o-w. Meanwhile, primary CCR prices stood at INR 883,000/t, stable w-o-w.

Domestic market weakens

Last month, domestic copper market sentiment had turned more positive, with trading activity picking up slightly despite the monsoon. Steady inquiries for high-grade copper supported market confidence, and northern Indian producers began witnessing improved buying interest in early Q3. Strong movement in premium-grade material across key consumption hubs helped sustain momentum, even as cash flow concerns persisted.

This week, however, demand remains dull, with ongoing monsoon conditions slowing down work across regions. Trading activity softened again, and most deals were concluded for smaller quantities, reflecting a cautious buying approach.

Global markets remain firm

Chinese import cash spreads for copper scrap held steady as of 16 July, with overseas supply remaining tight due to elevated US tariffs. Buyers in China continued to actively seek alternative sources to replace US-origin scrap, supporting firm offers from overseas sellers.

Bare bright (Millberry) copper scrap was assessed at 98.5-99% of LME three-month contract prices, unchanged from the previous week. #1 copper scrap (Berry/Candy) stood at 97.3-98.2%, while #2 copper scrap (Birch/Cliff) remained at 94.5-95.5%.

One trader reported securing 100 t at 98.6-98.9% for bare bright and 97.7-98.2% for #1 scrap. Another confirmed deal was at 94.5-95.5% for #2 scrap, all consistent with last week’s levels.

Tight scrap availability continued to support premiums, with traders expecting limited supply through the rest of the year unless China lifts its 10% tariff on US-origin material.

In China’s domestic market, scrap trades slowed over the past week as refined copper prices fell. The spread between domestic scrap and refined copper narrowed below RMB 1,500/t (~$210/t), a level widely seen as too slim to be attractive for copper fabricators.

European copper scrap spreads held steady this week, reflecting firm overseas offers and limited availability.

- Millberry was assessed at 98.5-99% of LME cash.

- Candy/Berry trades were in the 97.3-98.2% range.

- Birch/Cliff remained at 94.4-95.5%.

Tight supply and stable buying interest supported these levels, with no significant shifts in market tone compared to last week.

China’s copper cathode, scrap market sentiment

In China, copper cathode import premiums softened slightly. Offers for Japanese-origin cathodes slipped to $90/t over LME cash, compared to $105/t a week earlier, as short-term demand moderated.

Meanwhile, the Kazakhstani government’s move to support a ban on unwrought copper exports until 31 December has sparked concern. In January-May, Kazakhstan supplied 98,140 t, or 4.9% of China’s total copper imports. If implemented, the ban could tighten regional supply and help stabilise or lift cathode premiums in the near term.

Outlook

In India, the copper scrap market is expected to remain range-bound in the near term, with the ongoing monsoon continuing to dampen construction and electrical sector demand. Although high-grade material has seen some support, overall trading activity is likely to stay subdued until post-monsoon recovery sets in.

In Europe, the copper scrap market is expected to stay firm, driven by tight availability and consistent overseas offers. However, weak end-user demand – particularly from downstream industries – may cap any significant price gains in the near term.

Leave a Reply