- US emerges as largest supplier, imports rise by 179% y-o-y

- Improved processing capacity supports scrap consumption

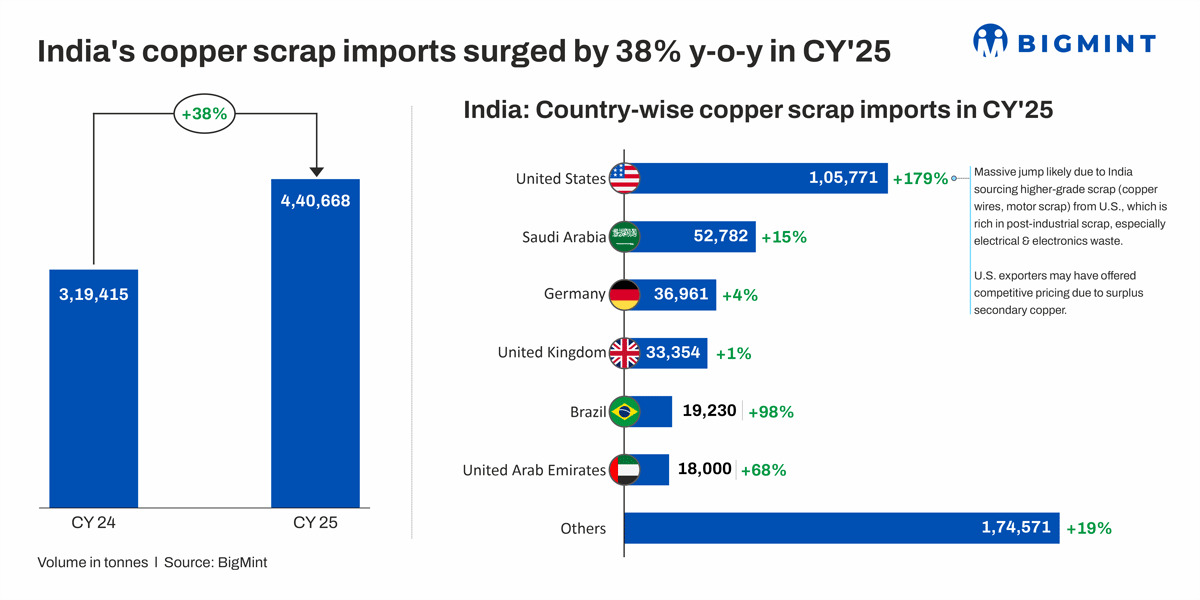

India’s copper scrap imports surged 38% y-o-y in CY’25 to 440,668 tonnes (t) from 319,415 t in CY’24, reflecting a sharp rise in reliance on secondary raw materials. The growth was supported by competitive pricing, persistent domestic supply gaps, robust downstream demand, and a decline in copper cathode imports due to regulatory bottlenecks. Firm scrap prices, tracking the rally in LME copper, also encouraged higher scrap imports.

Notably, average monthly scrap arrivals increased to around 36,700 t in CY’25, compared with 26,600 tonnes in CY’24, indicating stronger and more consistent buying interest. Monthly inflows rose steadily from about 24,600 t in January 2025 to nearly 36,700 t by year-end, reflecting aggressive procurement as scrap availability improved and higher scrap usage to offset domestic concentrate shortages and smelter constraints.

India’s refined copper output rises 20% y-o-y

Despite the rising volatility in prices and raw material constraints, India’s semi-finished (refined) copper production rose 33% y-o-y to 0.73 mnt in CY’25 from 0.55 mnt in CY’24. Hindalco led the increase, with output rising 24% to 0.51 mnt in CY’25 from 0.41 mnt in CY’24, supported by capacity optimisation and stronger downstream demand. Sesa Sterlite also recorded a notable rise of 25% to 0.17 mnt from 0.14 mnt over the same period. Additionally, Kutch Copper Ltd. contributed around 0.04 mnt in CY’25, emerging as a new contributor to India’s refined copper output. Overall, the y-o-y growth was driven by higher utilisation at existing players and the addition of new capacity.

Why did copper scrap imports rise in CY’25?

Policy tailwinds make scrap preferred feedstock: A key catalyst was the FY’26 Budget decision to maintain zero import duty on copper scrap, which significantly improved landed cost economics. This encouraged refiners, wire rod producers, cable manufacturers, and alloy makers to increase scrap procurement, especially as price volatility and supply uncertainty persisted in the refined copper market.

BIS norms, concentrate shortages drive scrap shift: Domestic supply constraints played an equally important role. Shortages of copper concentrates in India limited refined metal output, increasing reliance on secondary raw materials. This was compounded by QCO/BIS-related disruptions in cathode imports, especially during Q1 and Q2 of CY’25. Several overseas smelters faced certification delays or scaled back shipments due to BIS compliance requirements, creating multi-month gaps in primary metal availability. As a result, downstream units increasingly turned to scrap as a more predictable and flexible feedstock, with stable availability from the US, EU, and Middle East.

Improved processing capacity strengthens scrap usage: The structural shift towards scrap was further supported by upgraded refining and sorting capacities across key Indian clusters. Processors increasingly treated scrap as a strategic input rather than a marginal alternative, enabling smoother production planning for CCR units, brass manufacturers, and alloy producers. Improved recovery rates and processing efficiencies strengthened confidence in scrap-based operations, making secondary material the default choice for many consumers.

Country-wise imports – US leads scrap inflows as sourcing diversifies

Copper scrap imports from the US surged by 179% y-o-y to 105,771 t in CY’25, compared with 37,943 t in CY’24, making the US the single-largest supplier. This increase was driven by limited domestic smelting capacity in the US, subdued local consumption, and a strategic push by American exporters to offload accumulated post-industrial scrap.

At the same time, Saudi Arabia and the Middle East emerged as key alternative supply hubs, with imports from Saudi Arabia rising 15% y-o-y to 52,782 t and shipments from the UAE jumping 68% to 18,000 t. Brazil also recorded a sharp 98% increase, reflecting diversification of India’s sourcing base.

Grade-wise demand trends

Overall, imported scrap volumes across grades grew significantly in CY’25. Brass Honey imports rose by 13% to 128,513 t, Druid by 69% to 126,392 t, Birch by 36% to 63,007 t, and Berry by 79% to 44,655 t. Other grades such as Barley, Clove, and miscellaneous categories also posted strong growth, contributing to a total import increase of 38% y-o-y in CY’25.

Export demand boosts Brass Honey imports: Brass Honey accounted for the largest share of imports, with around 80% absorbed by Jamnagar. Strong demand was supported by positive Chinese brass ingot requirements, while India continued to act as a net importer of brass scrap and an exporter of finished brass products. In CY’25, India exported 111,188 t of finished copper products, up 16.6% from 95,262 t in CY’24, highlighting the sector’s strength in both domestic consumption and global trade.

Druid, Birch imports rise on infra projects, capacity expansions: Druid and Birch grades experienced higher demand, mainly from the cable and wire segment, driven by ongoing infrastructure projects and capacity expansions.

Recent developments in the sector reinforce this trend. Havells India has been allotted 1,58,200 square metre of land by Rajasthan State Industrial Development & Investment Corporation RIICO in Alwar to expand its cable manufacturing unit. The new parcel, adjacent to its existing facility, will support an investment of INR 715 crore aimed at increasing production capacity and strengthening the company’s position in the cables segment.

Similarly, this year, KEC International announced new orders worth INR 1,034 crore and is enhancing copper wire production, with capacities of 3,240 t/year for contact wire cables and 6 lakh fibre km for copper telecom cables. Meanwhile, KEI Industries commissioned a new plant in Sanand, Gujarat (Phase-1 by November 2025), adding 20-25% to its overall cable and copper-conductor manufacturing capacity and strengthening its export supply pipeline over the next two years.

Millberry saw rising consumption, particularly from the pure electric conductor segment, with even primary copper producers increasingly using it as an alternative feedstock to meet growing requirements.

What’s happening on supply, pricing side?

London Metal Exchange (LME) copper prices rose strongly in CY’25, with three-month prices averaging $9,961/t, up 7.5% y-o-y, while LME stocks fell 12.8% to 176,484 t, signalling tighter global supply. Prices remained supported by mine disruptions, limited concentrate availability, and long-term underinvestment in new capacity.

Global production cuts and operational challenges tightened the refined copper market. Glencore’s output fell 17% y-o-y to 583,500 t during January-September 2025, with full-year guidance of 850,000-875,000 t, while Freeport-McMoRan’s Grasberg mine remained under force majeure. Anglo American and Antofagasta also reduced production forecasts due to weaker ore grades in Chile. These factors kept LME copper prices elevated at $11,000-12,000/t by the end of December, though prices eased slightly as traders booked profits and Chinese smelters resumed partial output.

The rally extended into early 2026, with LME copper futures briefly crossing $13,000/t, driven by supply risks, pre-emptive stockpiling ahead of potential US tariffs, and strong demand from EVs, renewables, and data centres.

Meanwhile, Imported Birch Cliff copper scrap prices in India rose steadily through 2025, moving from $8,230/t in January to $10,881/t in December, marking a 32% increase over the year. This upward trend was largely aligned with LME copper price movements, reflecting tight global supply, structural market deficits, and strong premiums on high‑grade material. Prices rose gradually in the first half of the year, from $8,230/t to around $9,003/t in June, and accelerated in the latter half, crossing $10,000/t by October and reaching $10,881/t in December, driven by continued demand for high-quality imported scrap and limited prompt availability.

Higher refined copper prices pushed up domestic scrap values in tandem. In India, copper armature scrap (ex-Delhi) rose 11.5% y-o-y to INR 827,366/t in CY’25. Despite higher prices, imported scrap remained a viable alternative to expensive primary copper, supporting steady scrap demand.

What may happen in 2026?

Imported copper scrap is expected to remain elevated through early 2026, supported by a likely continuation of zero import duty and strong supply from the US and the Middle East. LME copper prices are expected to stay firm, keeping scrap prices high and sustaining its role as a critical feedstock for Indian refiners.

Even with the withdrawal of QCO/BIS requirements on cathodes, overseas smelters will need time to realign supply chains, meaning scrap will continue to dominate India’s copper imports. Limited domestic smelter capacity, favourable economics, reliable availability, and a flexible procurement environment will further support scrap demand.

Investments in sorting, refining, and grade optimisation are expected to enhance feedstock flexibility and manage cost volatility, while scrap’s structural share of India’s copper balance is likely to remain high due to cost advantages, lower compliance hurdles, and growing circularity initiatives.

Leave a Reply