- Gas shortage impacts downstream operations

- Rising domestic availability pressures scrap market

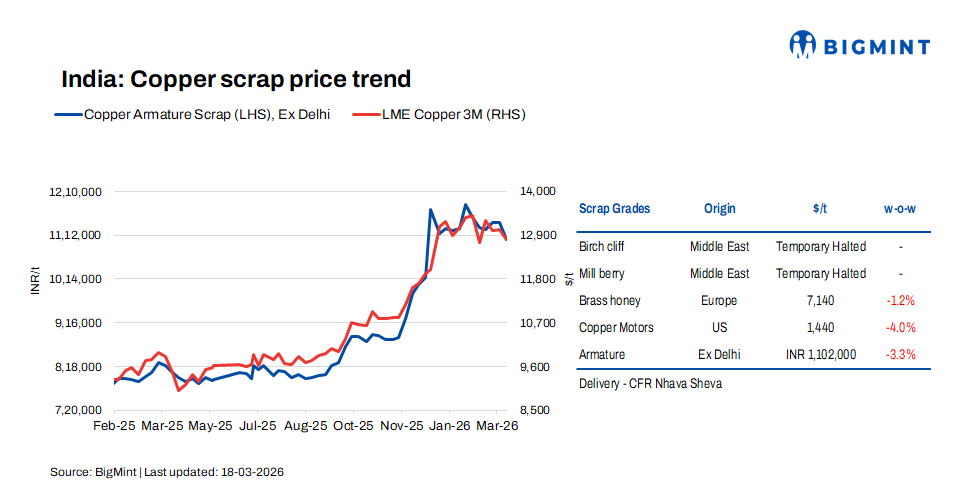

Imported and domestic copper scrap prices in India declined w-o-w, as on 17 March, weighed down by weaker demand fundamentals and easing global cues from the London Metal Exchange (LME). Market participants reported increased spot availability as suppliers actively destocked inventories to maintain cash flow amid slowing consumption.

Copper prices on the LME softened during the week. The three-month copper contract stood at $12,792/t on 17 March, down from $13,004.5/t on 12 March, reflecting a marginal correction amid cautious global sentiment and subdued downstream demand signals.

According to BigMint’s assessment, copper armature scrap, ex-Delhi, was assessed at INR 1,102,000/t, down 3.3% w-o-w. In the imported scrap segment, brass honey from Europe was assessed at $7,140/t CFR Nhava Sheva, down 1.2% w-o-w, while copper motors scrap from the US declined 4% to $1,440/t. Meanwhile, offers for Middle East-origin birch cliff and mill berry scrap were temporarily halted.

Market update

India’s copper market has witnessed a notable cooling down in recent weeks, with demand-side weakness becoming increasingly visible at the ground level. One of the key factors impacting consumption is the shortage of gas, largely linked to ongoing geopolitical tensions around the Strait of Hormuz. Several downstream plants reliant on gas have reduced or slowed operations, directly affecting copper demand.

Market dynamics have shifted significantly compared to previous weeks. Earlier, tight supply conditions kept scrap trading at premiums; however, the trend has now reversed, with material being offered at discounts. Suppliers have started offloading inventories more aggressively to improve liquidity, contributing to ample spot availability.

Export demand has also weakened considerably. Traders who were previously focused on overseas markets are now diverting material back into the domestic market due to reduced order inflows. This has further increased local supply and added downward pressure on prices. Some export-oriented players are offering material at discounted rates domestically to sustain cash flow.

Despite the current softness, market participants believe this is a temporary demand-side correction rather than a structural imbalance. Supply remains sufficient, but consumption has slowed. Notably, this trend appears specific to copper, while other non-ferrous metals such as aluminium continue to face tighter supply conditions, highlighting a divergence within the broader market.

LME market drivers

On the global front, copper prices remained under mild pressure, tracking cautious macro sentiment and limited buying interest. The decline in prices was also influenced by a lack of strong demand cues from major consuming regions.

Higher LME inventories during the week also weighed on sentiment, indicating relatively comfortable supply levels in the global market. In addition, the absence of strong recovery signals from key economies has kept buyers cautious.

Outlook

The Indian copper scrap market is expected to remain under pressure as weak demand and ample availability continue to weigh on prices. However, any improvement in downstream operations or easing of energy supply constraints could support a recovery in consumption.

Market participants will closely monitor global price trends on the LME, developments around energy supply, and export demand conditions to gauge the next direction of the market.

Leave a Reply