- Imports rise as steel mills resume pre-winter restocking

- Russia raises shipments to India amid soft China demand

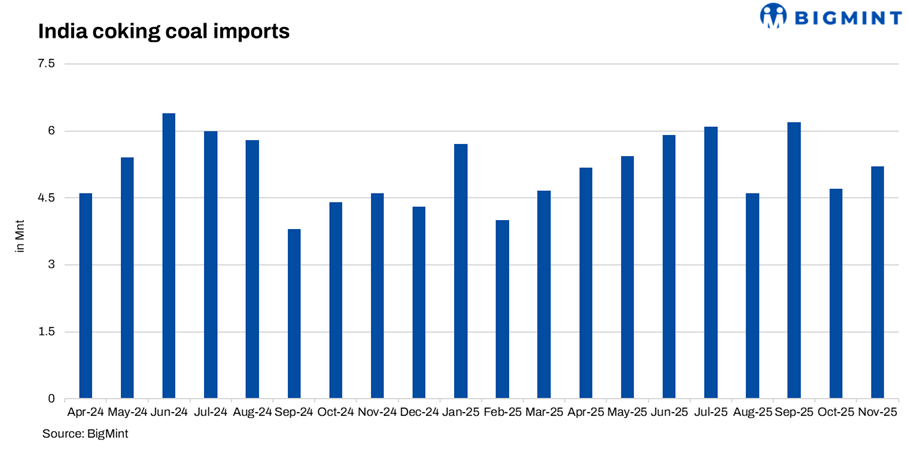

India’s coking coal imports increased 13% m-o-m to 5.2 mnt in November 2025, up from 4.6 mnt in October, as steelmakers replenished inventories after the festive lull and ahead of winter demand. Imports, however, remained broadly aligned with last year’s levels, reflecting steady but selective buying.

Suppliers: Higher flows from US, Russia, Mozambique

Australian supplies held stable at 2.8 mnt, continuing to dominate India’s intake. The US increased shipments to 0.9 mnt from 0.7 mnt, supported by competitive offers. Russian volumes doubled to 0.8 mnt as sellers targeted India amid softer Chinese buying. Mozambique also raised supply to 0.6 mnt from 0.4 mnt, aided by improved logistics. Smaller volumes arrived from Canada and Indonesia, underscoring diversified sourcing.

Buyers: JSW and Tata lift intake; SAIL trims slightly

JSW Steel increased imports significantly to 1.1 mnt from 0.7 mnt, while Tata Steel raised receipts to 0.8 mnt from 0.7 mnt. SAIL marginally reduced procurement to 1.2 mnt versus 1.3 mnt last month, whereas RINL and Jindal Steel upped intake to 0.4 mnt each. The rise across private mills signals pre-winter restocking and stabilising steel order books.

Why did imports rise in Nov’25?

Improved buying appetite: Mills resumed cargo bookings after holding back in October due to weak steel prices and heavy inventories. The early-December BF-rebar revisions showed mixed signals, but higher list prices at some mills helped restore confidence.

Coking coal cost dynamics: BigMint’s PHCC CFR India index moved up by $7-8 m-o-m to $215/t in November following firmer global cues and Chinese buying. Though bid-offer gaps persisted, mills accepted slightly higher prices to secure Q1 delivery cargoes.

Met coke trends supportive: Eastern India’s BF-grade met coke stayed firm at INR 32,000/t, supported by higher coking coal costs and thin supply. Western India remained steady. These stable coke fundamentals encouraged restocking of raw material coal.

Market overview

India’s buying remained selective but steady, with preference for reliable Australian coal supplemented by opportunistic procurement from Russia and the US. Marginally higher seaborne prices did not deter bookings, as several mills aimed to normalise inventory cycles before year-end.

Outlook

Imports are expected to remain volatile in December as mills buying stay with price-sensitive given persistent bid–offer gaps and cautious steel demand recovery. Recent hike in imported coking coal prices amid weakness in Chinese demand could shift trade flows in India’s favour.

Leave a Reply