- Mills rollover fails to boost demand

- High inventories, weak enquiries pressure market

Indian coated flat steel prices remained under pressure as demand continued to stay weak across key consuming sectors. Market activity slowed further during the assessment period, with enquiries for coated products declining and buyers limiting purchases to immediate requirements amid cautious sentiment.

Major steelmakers rolled over their June 2026 coated steel list prices, reflecting the subdued demand environment. GP list prices were maintained in the range of INR 75,000-79,750/t, while PPGI list prices were kept at INR 84,750-85,500/t.

Ample material availability across the supply chain and weak downstream consumption continued to weigh on market sentiment. Industry participants expect demand conditions and buying interest to remain subdued, keeping the overall market outlook cautious.

Price Update:

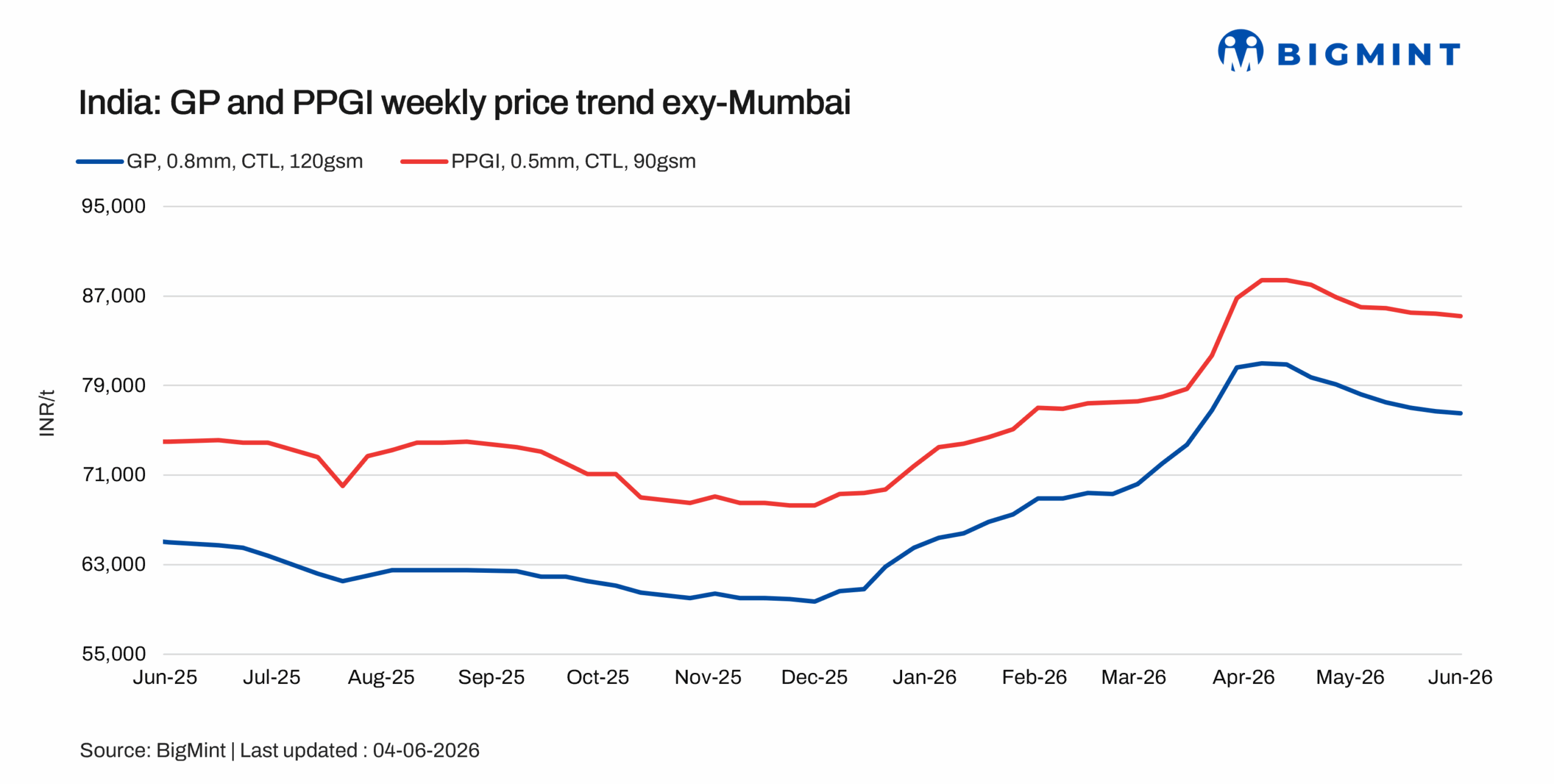

Galvanised plain (GP) coil (exy-Mumbai, India; 0.8mm / CTL, 120 GSM, IS 277) was assessed at INR 76,500/t, down by INR 200/t w-o-w amid continued weak demand and sluggish booking activity. Tradable offers were heard in the range of INR 75,500-78,000/t.

Pre-painted galvanised iron (PPGI) (exy-Mumbai, India; 0.5mm / CTL, 90 GSM, IS 14246) was assessed at INR 85,200/t, down by INR 200/t w-o-w. Offers were reported in the range of INR 84,500-86,500/t, while enquiries and bookings remained slow due to subdued market sentiment.

Galvalume/bare galvalume (BGL) (exy-Mumbai, India; 0.5mm / CTL, 1220mm, AZ150) was assessed at INR 89,300/t, down by INR 200/t w-o-w. Offers were indicated in the range of INR 88,500-90,500/t, while trading activity remained limited amid weak demand conditions.

Raw material prices

India’s zinc ingot (99.995%) prices increased moderately w-o-w by around INR 6,000/t ($63/t) to INR 384,000/t ($4,010/t) ex-Delhi on 3 June 2026, supported by firmer global zinc prices and sustained producer pricing discipline, although downstream demand continued to remain largely need-based due to subdued consumption from the galvanising sector.

BigMint’s bi-weekly benchmark assessment for HRC (IS2062, Gr E250, 2.5-8 mm/CTL) declined by INR 200/t ($2/t) w-o-w to INR 58,400/t ($610/t) as of 2 June against INR 58,600/t ($612/t) a week ago.

Meanwhile, CRC (IS513, Gr O, 0.9 mm/CTL) prices increased by INR 200/t ($2/t) w-o-w to INR 65,200/t ($681/t) on 2 June. These assessments are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

Market update

The Indian coated flat steel market remained subdued during the week, with overall demand continuing to stay weak across key consuming regions. Market sentiment remained cautious as enquiries for coated products were limited, while buyers largely restricted procurement to immediate requirements amid slow consumption trends.

The rollover of June coated steel list prices by major mills failed to improve buying interest, with market participants continuing to adopt a wait-and-watch approach. Several buyers, particularly in southern India, are anticipating additional discounts from mills before making fresh bookings.

Ample inventory availability across the supply chain continued to weigh on sentiment. Market participants indicated that inventory levels in the southern region remain elevated, with stocks exceeding 1.5 months of consumption in some locations. Weak spot demand and comfortable stock positions continued to limit trading activity across both GP and PPGI segments.

Overall, subdued demand, dull enquiries, and high inventory levels continued to keep the coated flat steel market under pressure.

Outlook

India’s coated flat steel market is expected to remain under pressure as cautious buying sentiment and elevated inventory levels continue to weigh on trade activity. With the monsoon season approaching, construction and infrastructure-related demand may slow further, resulting in weaker enquiries across key markets. Unless inventories decline significantly or demand shows signs of recovery, market sentiment is likely to remain subdued.

Leave a Reply