- Mill’s list price hike fails to lift tradable values

- Labour shortages continue to disrupt operations

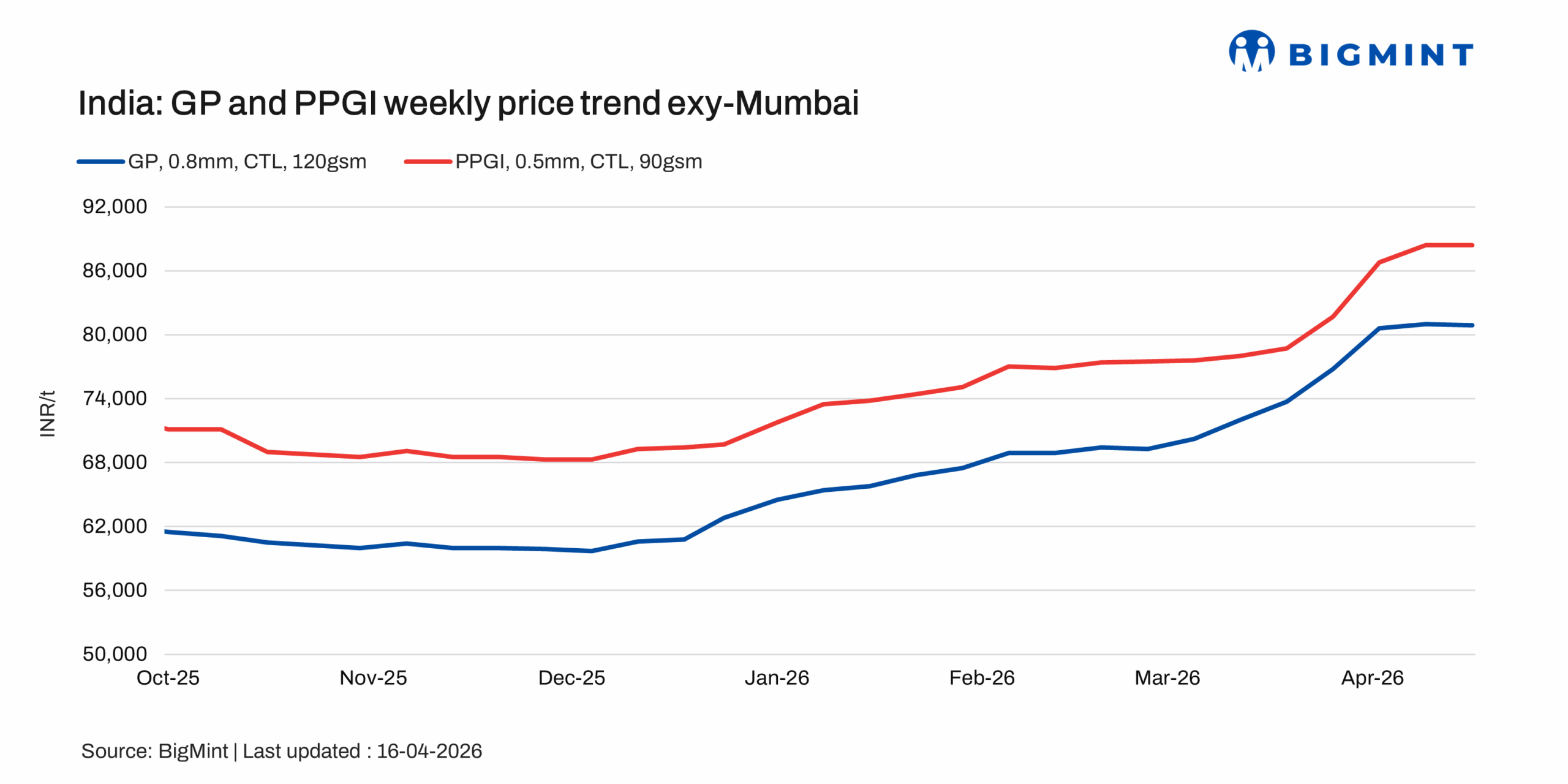

Indian galvanised plain (GP) and pre-painted galvanised iron (PPGI) coated flat steel prices remained under pressure during the week ending 16 April 2026, despite a major mill announcing a fresh INR 2,500/t hike across both product segments. However, the increase has not been reflected in the spot market, as transaction prices across several regions continued to soften amid weak demand and panic selling by traders.

Market sentiment remained dull, with buying activity strictly need-based and actual deal prices heard below revised mill offers. This continues to highlight a clear disconnect between mill-led price hikes and prevailing spot market realities, as the broader market has yet to absorb the increase.

Price updates

Galvanised plain (GP) coil (exy-Mumbai, India; 0.8mm / CTL, 120 GSM, IS 277) was assessed at INR 80,900/t ($877/t) on 16 April 2026, down by INR 100/t w-o-w. Tradable ranges were heard at INR 80,500-81,500/t, reflecting cautious buying sentiment amid mixed market conditions.

Pre-painted galvanised iron (PPGI) (exy-Mumbai, India; 0.5mm / CTL, 90 GSM, IS 14246) prices remained stable w-o-w at INR 88,400/t ($948/t), with market offer ranges heard at INR 87,000-89,000/t. Mills continued to maintain pricing discipline, although demand remained largely need-based.

Galvalume/bare galvalume (BGL) (exy-Mumbai, India; 0.5mm / CTL, 1220mm, AZ150) was assessed at INR 90,200/t ($967/t), down by INR 800/t w-o-w. Offers were indicated in the range of INR 90,000-90,500/t.

Overall, prices remained mixed across coated flat steel segments, with GP and BGL witnessing marginal corrections, while PPGI held steady amid dull sentiment and regionally uneven demand.

Hot-dip galvanised iron (HDGI) export offers remained stable w-o-w at $770/t as of 09 April 2026, with market activity indicating cautious buying interest alongside firm mill pricing.

Raw material prices

India’s zinc ingot (99.995%) prices increased marginally by INR 1,000/t w-o-w to INR 343,000/t ex-Delhi on 14 April, against INR 342,000/t a week earlier, supported by stable spot demand and slightly firmer global cues. The rise came despite Hindustan Zinc Ltd (HZL) revising its list prices downward by INR 4,200/t to INR 342,700/t ex-Chanderiya on 13 April, compared with INR 346,900/t on 9 April.

On the substrate side, BigMint’s bi-weekly HRC benchmark (IS2062, Gr E250, 2.5-8 mm/CTL) declined by INR 600/t w-o-w to INR 59,300/t ($637/t) as of 14 April from INR 59,900/t ($643/t) on 7 April. Similarly, CRC prices (IS513, Gr O, 0.9 mm/CTL) were assessed at INR 66,900/t ($719/t), also lower by INR 600/t w-o-w from INR 67,500/t ($725/t) in the previous assessment. Prices are assessed ex-Mumbai for the distributor-to-dealer segment, excluding 18% GST.

Market update

Market sentiment remained subdued during the week, with demand across all major regions continuing to stay slow and trading activity largely restricted to immediate requirements. Despite the increase in galvanised steel prices in the previous weeks, buying interest remained weak as most market participants adopted a cautious stance amid uncertain downstream offtake. In addition, ongoing labour shortages due to the election and seeding season, gas supply disruptions, and limited availability of key raw materials continued to weigh on production schedules of both end-users and steelmakers, as well as market confidence.

Sources across regions indicated that buyers are currently prioritising the liquidation of existing inventory and finished stock, with panic selling also emerging in select markets as traders attempted to reduce exposure amid weak offtake and uncertainty over near-term price sustainability. This distress-led selling has further weighed on executable market levels, even as mill offers remained firm. The cautious approach is also being driven by concerns over the ability to pass on higher costs to end consumers.

As a result, most participants expect to reassess procurement plans in May, once current inventories are cleared, and there is better visibility on price direction and demand recovery. Overall, slow regional demand, panic-led inventory liquidation, labour-related operational constraints, and cautious buyer sentiment remained the key themes during the assessment period, limiting market momentum despite firm mill offers.

Outlook

The coated flat steel market is likely to remain under pressure this month, as the recent mill-led price increase has yet to gain traction in the spot market. The continued gap between announced offers and executable deal levels suggests that buyers are still unwilling to accept higher prices in the absence of demand support.

Over the next few weeks, market movement is expected to remain largely sentiment-driven, with stock liquidation and cautious procurement likely to continue dominating trade activity. A clearer direction may emerge in May, once existing inventories are absorbed and participants return to the market with revised buying plans. Unless demand shows a visible pickup across key regions, spot prices may continue to witness mild corrections even as mills attempt to hold offers firm.

Leave a Reply