- Rains disrupt activity in downstream segments

- Prices likely to decline further in near term

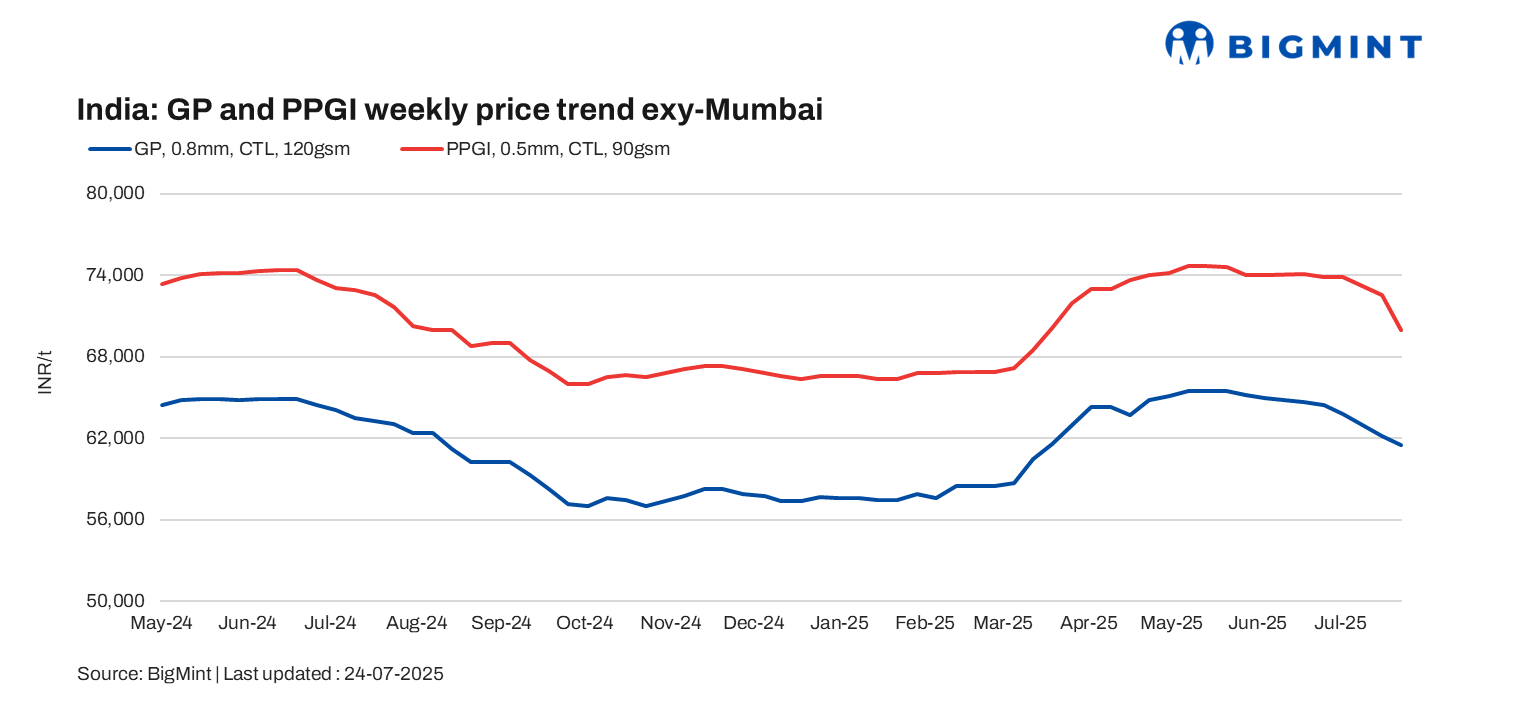

India’s coated flat steel market continued its downtrend through the week ending 24 July, driven by weak demand from core sectors and monsoonal disruptions. Traders highlighted negligible buying interest, with buyers facing severe liquidity stress, especially in western regions.

The latest weekly assessment on 24 July showed galvanised plain (GP) coil (0.8 mm/CTL, 120 gsm, IS277) prices at INR 61,500/t ($712/t) exy-Mumbai, down INR 700/t ($9/t) w-o-w, with offers ranging between INR 61,000 -62,000/t ($705-717/t).

Meanwhile, pre-painted galvanised (PPGI) (0.5 mm/CTL, 90 gsm, IS14246) was assessed at INR 70,000/t ($810/t) exy-Mumbai, with offers hovering between INR 69,500-70,500/t ($804-816/t). Prices are exclusive of 18% GST. (USD 1 = INR 86.4172) (INR 1 = USD 0.0115718)

Market updates

Demand from renewables segment stays soft: PPGI demand from the renewable segment remained soft, with engineering, procurement, and construction (EPC) activity slowing by 1-4% w-o-w. Weather-driven delays and regulatory issues disrupted solar and wind project execution. Gujarat’s Imandra Solar received a 315-day extension, underlining project-level stagnation.

Demand from infra, construction stagnant: Coated steel demand in the construction sector was stagnant. No fresh orders were reported for GP or PPGI. Rains disrupted metro and commercial project sites, halting movement and causing widespread material pile-up at stockyards.

“The confluence of persistent heavy rainfall, labor scarcities, and power disruptions is severely impacting productivity in the northern regions,” a source informed BigMint.

A West India-based distributor stated, “There is no movement in the market — cash flow is tight and buyers are cautious.”

Outlook

The near-term outlook for coated flat steel remains bearish, with prices likely to face further downside through August in the absence of a demand rebound. Monsoon-related logistical and operational constraints are expected to persist, while end-user sentiment stays cautious across infra and renewable sectors.

Leave a Reply