- Rising input and logistics costs support prices

- Buyers cautious amid high prices and uncertainty

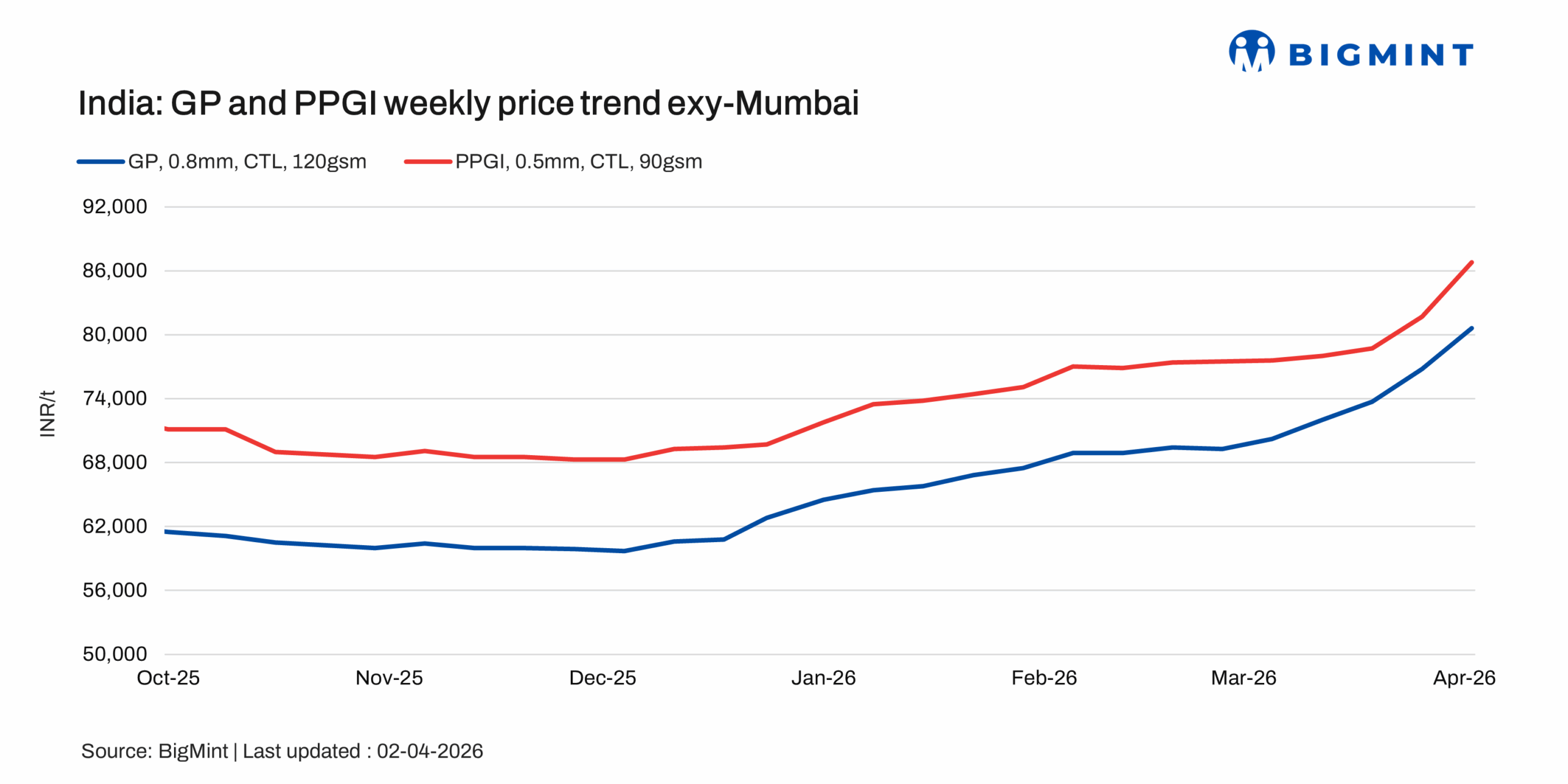

Indian coated flat steel prices recorded a sharp w-o-w increase, despite relatively slow demand conditions. The uptrend was largely driven by supply-side constraints and rising cost pressures rather than consumption strength.

Producers implemented notable price hikes, with galvanised plain (GP) increasing by INR 3,250/t ($35/t) and pre-painted galvanised iron (PPGI) rising by INR 2,500/t ($27/t). These revisions were primarily driven by escalating logistics costs and ongoing global geopolitical uncertainties impacting input prices.

Market feedback suggests that while demand remains subdued, mills have maintained firm pricing amid constrained availability and elevated production costs.

Overall, the sharp price increase reflects strong cost-push factors, with the near-term outlook remaining firm, contingent on logistics trends and input cost movements.

Price update

Benchmark assessment for GP coil (exy-Mumbai, India; 0.8mm / CTL, 120 GSM, IS 277) was assessed at INR 80,600/t ($856/t) on 2 April, up by INR 3,600/t ($39/t) w-o-w, with tradable ranges reported at INR 80,000-81,000/t, supported by tight availability and firm mill offers.

PPGI (exy-Mumbai, India; 0.5mm / CTL, 90 GSM, IS 14246) was assessed at INR 86,800/t ($920/t), up by INR 5,100/t ($54/t) w-o-w, with market offer ranges at INR 86,000-88,000/t, driven by improved demand traction and sustained pricing discipline from mills.

Galvalume/BGL (exy-Mumbai, India; 0.5mm / CTL, 1220mm, AZ150) was assessed at INR 89,600/t ($950/t), up by INR 3,600/t ($38/t) w-o-w, with indicative market offer prices heard at INR 86,000-87,500/t.

Market update

Trading activity in the coated flat steel segment remained slow across regions during the assessment period, primarily due to the recent sharp price increases implemented by mills. The uptrend has been driven by geopolitical tensions, rising input costs, and raw material shortages, which have collectively pushed up overall production expenses.

Market participants noted that higher prices have led to cautious buying, with procurement largely limited to immediate requirements. Additionally, the ongoing financial year-end and festival-related slowdown have further weighed on trading volumes.

However, sentiment remains cautiously optimistic, with participants anticipating a pickup in demand from next week as the new financial year begins and post-festival activity resumes. Mills are expected to maintain a firm pricing stance, supported by continued cost pressures and supply-side constraints.

Raw material prices

India’s zinc ingot (99.995%) prices edged higher by INR 11,000/t w-o-w to INR 3,28,000/t ex-Delhi as of 31 March, compared with INR 3,17,000/t in the previous week, reflecting improved buying interest and firmer spot sentiment. The increase followed a price revision by Hindustan Zinc Limited (HZL), which raised its offers by INR 8,500/t to INR 3,29,500/t ex-Chanderiya, further supporting market sentiment.

BigMint’s benchmark assessment (bi-weekly) for HRC (IS2062, Gr E250, 2.5–8 mm/CTL) increased by INR 2,000/t ($21/t) w-o-w to INR 59,500/t ($634/t) on 31 March, compared with INR 57,500/t ($613/t) on 24 March.

Similarly, CRC (IS513, Gr O, 0.9 mm/CTL) prices were assessed at INR 67,000/t ($713/t) on 31 March, up by INR 2,000/t ($21/t) w-o-w from INR 65,000/t ($692/t) on 24 March. These prices are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

Outlook

Market sentiment remains cautiously firm, underpinned by supply-side tightness and sustained cost pressures. Despite weak demand signals, mills’ pricing discipline indicates limited downside risk. A gradual normalisation in trade activity is expected, which could improve market liquidity, while the overall trend remains supported by supply constraints.

Leave a Reply