- Mill discipline outweighs cautious demand conditions

- Cost support and thin-gauge tightness stabilise prices

Indian coated flat steel prices remained largely steady to marginally firm as of 26 February 2026, supported by controlled mill supplies and selective price discipline across galvanised plain (GP), pre-painted galvanised iron (PPGI), and galvalume (BGL) segments. While material movement showed some improvement, overall buying interest continued to remain cautious, with trade largely driven by need-based procurement.

On the raw material front, zinc prices strengthened in the domestic market, lending cost support to coated flat steel. Zinc ingot (99.995%) prices rose by INR 10,000/t w-o-w to INR 3,37,000/t ex-Delhi as on 24 February, supported by firm global cues and tightening availability. Hindustan Zinc Limited also increased zinc ingot prices by INR 4,900/t to INR 3,38,200/t ex-Chanderiya. However, resistance is expected above the INR 3,40,000–3,45,000/t range amid margin pressure at the downstream level, with prices likely to stabilise near current highs in the near term.

Trade-level flat steel prices remained muted amid subdued sentiment. HRC prices were assessed at INR 52,200–54,500/t, while CRC prices stood at INR 56,200–61,700/t during the week ended 24 February. BigMint’s benchmark HRC inched up marginally by INR 100/t w-o-w to INR 53,700/t, while CRC prices held steady at around INR 59,500/t, ex-Mumbai, excluding 18% GST.

Hot-dip galvanised iron (HDGI) export offers remained stable w-o-w at $770/t as of 26 February 2026, reflecting continued cautious buying interest despite firm underlying mill pricing.

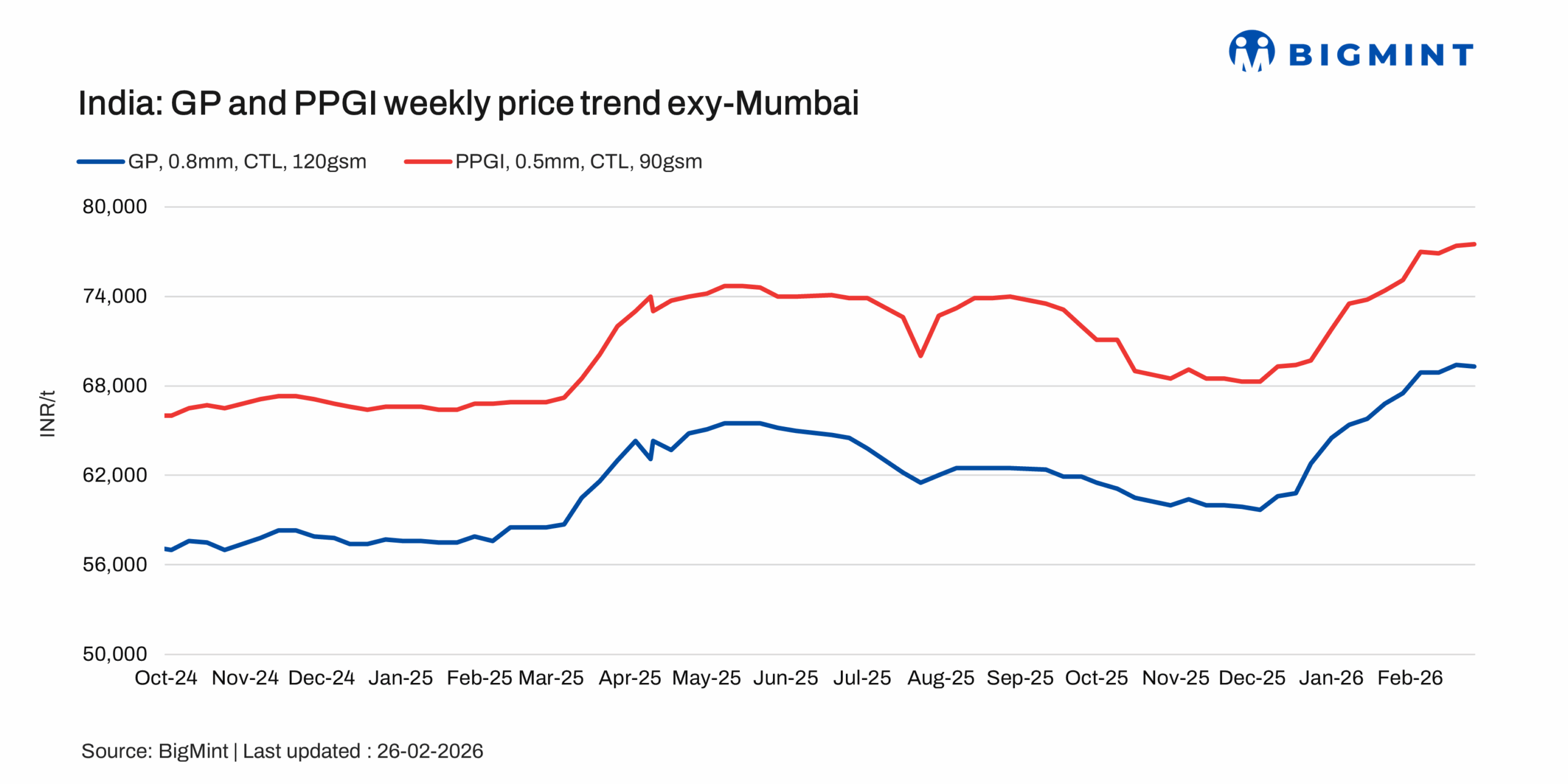

As per the latest assessment, BigMint’s benchmark for Mumbai indicated mixed price movements in the coated flat steel segment. GP coil prices edged down by INR 100/t ($1/t) w-o-w to INR 69,300/t ($762/t) exy-Mumbai, with market offers largely reported in the range of INR 69,000-70,000/t ($758-770/t) amid cautious trade sentiment.

PPGI prices inched up marginally by INR 100/t ($1/t) w-o-w to INR 77,500/t ($852/t)exy-Mumbai. Offers were mostly heard in the range of INR 77,000-78,000/t ($847-587/t), as mills maintained a firm stance despite subdued demand.

Meanwhile, BGL prices remained stable w-o-w at INR 81,000/t ($890/t) exy-Mumbai. Market offers were reported in the range of INR 80,500-81,500/t ($885-896/t) , supported by tight availability, although regional demand conditions remained mixed.

All prices are exclusive of 18% GST.

Market Update:

Regional demand trends showed early signs of improvement during the assessment period. Buying interest in the western and northern regions picked up modestly, with participants reporting gradual movement of material following recent mill-led price hikes, although transaction volumes remained measured. In contrast, sentiment in the southern region continued to remain dull, with purchases largely restricted to need-based buying.

Across regions, some market participants highlighted tight availability of thinner gauge material, which lent underlying support to prices. Looking ahead, mills are expected to consider price increases for March, supported by controlled supplies and improving demand sentiment in the west and north. However, participants informed BigMint that while material movement has improved, it continues to remain slow and cautious in the near term.

Outlook

Market sentiment is showing gradual improvement, but near-term price direction is expected to remain largely mill-driven rather than demand-led. Tight availability of thinner gauges and sustained raw material support continue to limit downside risks. Project-related procurement may provide incremental demand support, particularly for coated flat steel; however, any price upside is likely to be gradual, as buying remains selective and the conversion of enquiries into confirmed orders continues to progress at a measured pace.

Leave a Reply