- Indian importers adopted wait-&-watch approach

- Limited vessel availability seen in the Pacific basin

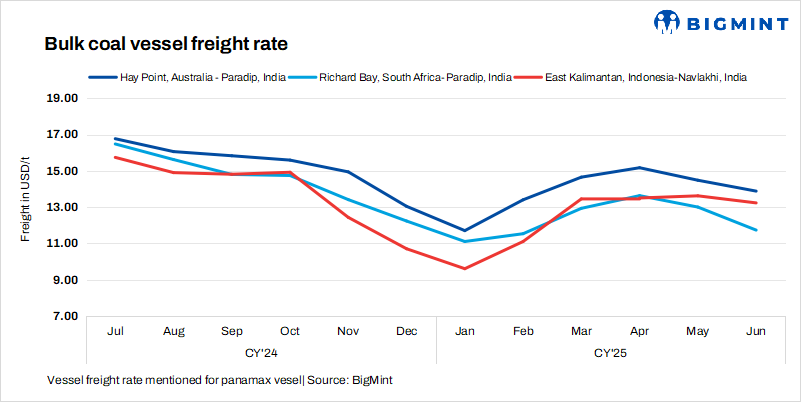

Panamax coal freight rates to India exhibited mixed trends on a weekly basis. Freight rates rose on the Australia and Indonesia routes due to improved cargo demand. In contrast, rates on the South Africa route declined amid softer activity. Overall, market sentiment remains volatile, influencing regional rate movements.

The mixed sentiment in Panamax coal freight to India can be attributed to contrasting dynamics across the Atlantic and Pacific basins, as well as evolving regional energy developments.

From the Pacific basin, stronger coal demand ex-Australia and Indonesia continued to lend support to Panamax freight. Australian shipments, in particular, have driven a bullish tone with rising volumes and tight vessel supply. However, market participants have grown cautious about sustaining this momentum amid increasing operational costs and potential delays in project delivery, especially in Australia. Moreover, steady demand from North Pacific trade routes added to rate firmness, but the slower pace of new cargo replenishment in some pockets slightly dampened the overall outlook.

Adding to the complexity is the shift in India’s domestic energy strategy. With India aggressively expanding its renewable capacity-particularly hydropower and pumped storage, the long-term outlook for coal imports is increasingly uncertain.

Notably, portside thermal coal inventories in India recorded a marginal weekly decline, falling to 15.87 mnt during week 25 of CY’25 from 16 mnt in the previous week. The reduction was driven by subdued arrivals at select ports, despite some locations witnessing fresh replenishments.

Baltic indices fall w-o-w except BSI: Vessel demand indicators saw a downtrend w-o-w except for the Baltic Supramax Index, with the Baltic Dry Index (BDI) decreasing by 279 points to 1,689 as of 23 June. The Baltic Panamax Index (BPI) also fell by 51 points to 1,350 points compared to 1,401 points a week earlier. However, the Baltic Supramax Index (BSI) inched up by 37 points w-o-w to settle at 973.

Route specifications

- Australia-India rates rise: Freights from Australia to India rose by $0.6/t w-o-w, with BigMint’s assessment indicating that rates for Hay Point Port to Paradip were at $14.1/dry metric tonne (dmt). Sources informed that RINL booked two Panamax vessels from Australia to Gangavaram at $16.85-17.05/t, with shipment scheduled for 11-25 July.

- South Africa-India freights fall: Freights from the Richards Bay Coal Terminal (RBCT) to Paradip decreased w-o-w by $0.3/t to $12.3/t. Freight rates fell due to reduced coal demand from India amid monsoon slowdown and high portside inventories. Limited fresh cargoes and wider bid-offer spreads also contributed to the softness. Additionally, vessel oversupply in the region led to rate pressure.

- Indonesia-India freights climb: Freights for coal shipments from East Kalimantan to Paradip rose by $0.8/t to $13.6/t w-o-w amid tighter vessel availability and active restocking by Indian buyers ahead of peak monsoon. Renewed demand for low-CV coal made Indonesian cargoes attractive, boosting spot activity.

Leave a Reply