- Firm demand and tight prompt supply support sentiment

- Muted fixtures, weak enquiries weigh on rates amid ample tonnage

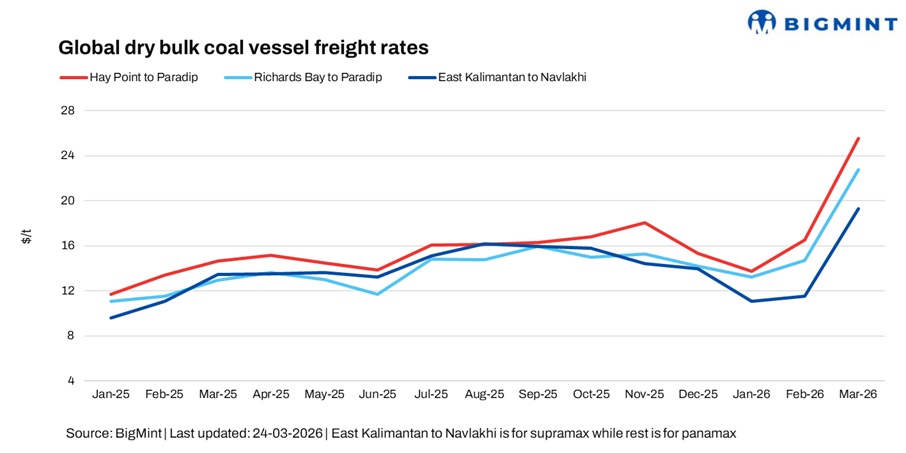

Dry bulk coal freight rates showed a mixed trend w-o-w as of 24 March, supported by firm demand and tight prompt vessel supply, while weak cargo activity and ample tonnage weighed on sentiment amid bunker volatility. Bunker prices rebounded after the previous session’s decline, with volatility persisting amid ongoing geopolitical tensions despite a temporary pause in military action.

The Baltic Dry Index edged lower, reflecting softer sentiment amid slower fixing activity and cautious chartering despite steady cargo flows. Panamax and Supramax segments also saw mild pressure, indicating subdued momentum across the dry bulk market.

A shipbroker said, “Yesterday there was a correction in bunker prices, but it is difficult to take a call at this moment; rates are volatile.”

Route wise updates:

In the Atlantic basin, tightening prompt vessel availability supported sentiment, though subdued activity and limited market impetus capped stronger momentum. Market participants indicated that activity remained slow, with one broker noting, “Market is a bit dull. Traders are hoarding cargoes and waiting for the market to fall.”

Adding to the cautious tone, sources indicated that the Supramax segment continued to face pressure due to muted fixtures and weak tonnage demand, alongside ample vessel availability. Overall activity remained thin, reflecting limited fresh enquiries.

A market source said, “No recent fixtures to be honest. Charterers are postponing their laycan.” adding that trading information remained limited.

Another source told BigMint, “It’s a difficult time for charterers to move cargo, with only urgent requirements being fixed. We should have a clearer picture in the next few days.”

The source added that fixture visibility remains limited, with brokers seeing little activity and some headowners fixing directly with charterers, indicating a quieter and less transparent market.

Reflecting mixed sentiment, another ship broker said, “Freight sentiments, I feel, are sideways to a little upwards.”

Outlook

Freight sentiment is expected to remain mixed in the near term, with tight vessel availability supporting some segments, while weak enquiries and ample tonnage continue to pressure others. Market participants are likely to stay cautious amid bunker uncertainty, with clearer direction expected as demand visibility improves.

Leave a Reply