- Weak cargo visibility pressures Panamax and Supramax segments

- Bunker-driven volatility continues to disrupt fixing and sentiment

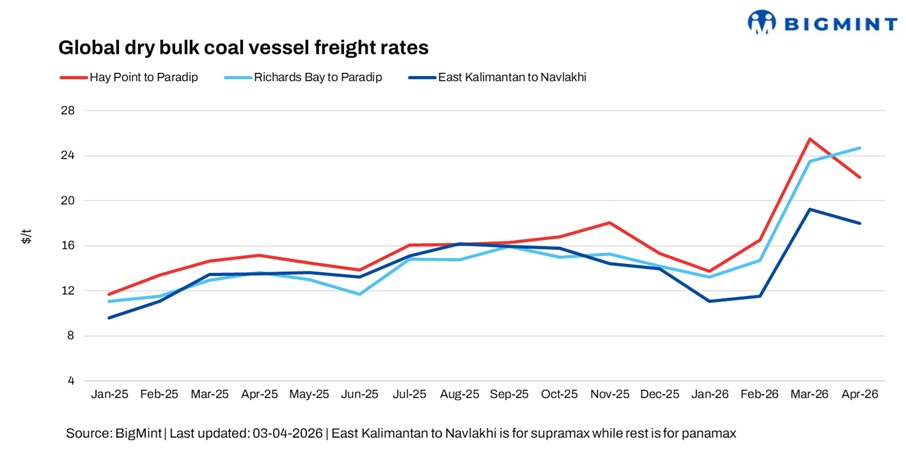

Dry bulk coal freight rates to India softened in the week ended 3 April, amid limited cargoes and subdued fixtures, with higher vessel availability and uneven demand pressuring rates despite slightly easing crude.

Market participants pointed to a clear imbalance between cargo and tonnage. A shipbroker said, “Cargo volume is down, vessel availability is more, bunkers taking all profit — very few fixtures are happening.”

“Market is very uncertain at the moment, and there are limited cargoes,” another broker noted, highlighting weak enquiry levels.

Bunker price fluctuations continued to play a decisive role in fixing activity. A charterer said, “Market is going up and down on a daily basis because of bunkers,” underscoring the difficulty in concluding deals amid shifting fuel costs.

Another charterer added, “If the conflict eases, bunker and freight may decline, but for now everyone remains in wait-and-watch mode,” reflecting cautious positioning by market participants.

Route-wise updates

Market highlights

- Bunker prices gain w-o-w: Bunker prices gained by $31/t w-o-w to $890/t on 3 April, supported by higher crude oil prices, supply tightness in key bunkering hubs, and firm demand from the shipping sector.

- Baltic index rises w-o-w: The Baltic Index increased by 52 points w-o-w to 2,066 on 03 April, supported by gains in Panamax, which rose by 14 points to 1,784, and Supramax, which edged up by 19 points to 1,224, indicating modest improvement in dry bulk activity.

- DCE coke futures drop w-o-w: Coke futures on the Dalian Commodity Exchange decreased by around RMB 83.5/t ($12.13/t) w-o-w to RMB 1,670/t ($242.54/t) on 03 April, reflecting softer steel demand and limited mill restocking, which weighed on downstream coal trade sentiment.

- Brent crude futures remain volatile: Brent crude oil (June 2026 contract) was last assessed at $109.03/bbl on 2 April, with no further updates as markets remained closed for the Good Friday holiday. Market remained volatile throughout the week.

Outlook

Coal freight rates to India are expected to remain weak in the near term, as limited cargo visibility and ample tonnage continue to pressure the market. While easing crude may cap further downside in bunkers, persistent volatility and cautious participation are likely to keep fixing activity subdued.

Leave a Reply