- Pacific and Atlantic rates fall as demand weakens and vessel supply rises

- RBCT outage, soft demand, and low bunker costs pressure coal freight

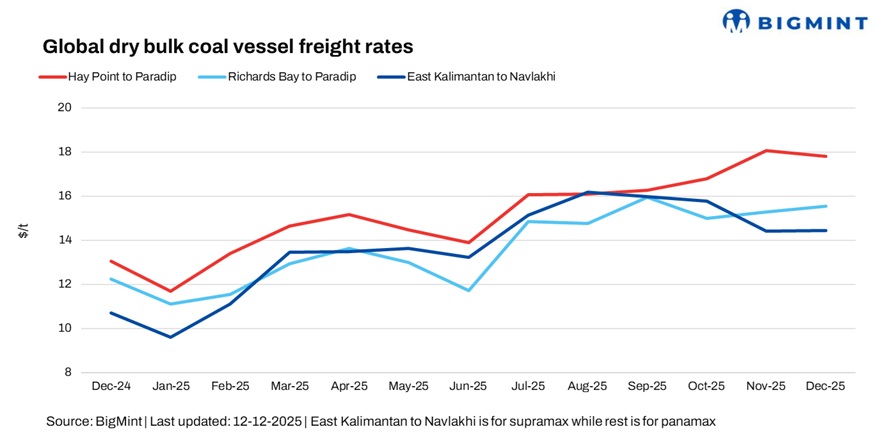

Dry bulk coal freight rates to India have softened overall in the week ended 12 December, with both Pacific and Atlantic trades reflecting weaker underlying demand and expanding vessel availability. In the Pacific basin, earlier support from prompt tonnage tightness has given way to downward pressure as coal enquiry recedes and vessel lists lengthen, prompting owners to adjust offers lower. This softer sentiment aligns with broader market trends showing easing coal shipments globally and weaker dry bulk cargo flows, which have reduced freight demand on key Asia-Pacific routes.

In the Atlantic, freight rates continued to correct sharply, driven by subdued activity and a lack of fresh fixtures. Export volumes have slowed, and tonnage supply has outpaced cargo stems, pushing index readings and rate ideas lower across Panamax and Supramax segments. The combination of light demand and ample vessel availability has left little room for upward momentum, reinforcing the overall downtrend in freight costs from Atlantic load regions to India.

A shipbroker said, “With export volumes slowing and vessel supply outpacing cargo demand, market sentiment has turned slightly bearish, leaving limited room for any upward movement in Panamax and Supramax freight rates.”

Coal freight rates on the Australia-India route declined this week, weighed down by limited fixtures and bid-offer disparity, with SAIL remaining the only notable Indian buyer in the market. Activity was markedly lower compared with previous weeks, as most charterers stayed on the sidelines amid weak steel market sentiment. High inventories and cautious buying behavior – coupled with expectations of upcoming mill price announcements – kept demand muted. With few fresh enquiries and no competitive bidding pressure, owners were forced to soften their rate ideas, contributing to the downward movement.

Freight rates on the South Africa-India route fell sharply w-o-w, weighed down by subdued demand and ample vessel availability. The market was further affected after coal loading operations at Berth 801 of Richards Bay Coal Terminal (RBCT) were halted due to strong winds damaging the Mantakraft loader, prompting a force majeure declaration on 2 December, according to BigMint. The shutdown is expected to last around 14 days, temporarily curbing coal exports from one of South Africa’s main gateways, which shipped about 25 million tonnes to India in 2024. This disruption may tighten supply temporarily, but with limited cargo enquiry, rates remained under pressure.

Supramax freight rates on the Indonesia-India route fell this week, reflecting lower enquiry levels and a limited number of fixtures from Indian buyers. With fewer cargoes being booked and prompt vessel availability increasing, owners were forced to reduce rate ideas. Activity on Indonesia-China flows also remained quiet, further contributing to the softening in the Supramax market.

Weaker fuel demand pulls bunker prices lower

Bunker prices eased slightly this week as overall fuel demand weakened and supply improved at major ports. With fewer vessels fixing cargoes and shipping activity slowing, fuel buying also dropped, leading to softer marine fuel prices. Normally, higher fuel costs support freight rates, but this week’s small decline — combined with weak cargo demand and plenty of available vessels — meant bunkers offered very little support to the freight market.

Coal freight faces pressure amid weak demand and high vessel supply

The coal freight market this week saw softer demand and rising vessel availability, shifting the overall supply-demand balance. Fewer cargo enquiries from Indian buyers and slower export activity from Australia, South Africa, and Indonesia increased open tonnage, prompting owners to lower rate ideas. This imbalance kept freight levels under pressure, with limited upward momentum expected until cargo flows pick up or prompt vessel supply tightens.

Route-wise updates

- Australia (Hay Point)-India (Paradip), Panamax: Freights from Australia to India fell w-o-w by around 1.34/dry metric tonne (dmt) to $17.10/dmt.

- South Africa (Richards Bay)-India (Paradip), Panamax: Panamax freights on the South Africa to India route edged down w-o-w by $0.64/dmt to $15/dmt.

- Indonesia (East Kalimantan)-India (Navlakhi), Supramax: Supramax coal freights on the Indonesia to India route stood at $14/dmt, a decrease of $0.70/dmt, w-o-w.

Meanwhile, the Baltic Exchange’s dry bulk indices for Panamax and Supramax vessels weakened notably this week, with the Panamax index dropping sharply by 139 points w-o-w to 1,724, while the Supramax index fell by 54 points to 1,387. The steep decline in the Panamax index reflects subdued demand across key coal and grain routes, coupled with abundant vessel availability that pushed owners to reduce offers to secure employment. Similarly, the downturn in the Supramax index suggests softer enquiry levels and improving tonnage supply, which weighed on rates and underscored the broader weakness in dry bulk market sentiment.

Outlook

Freight rates to India are likely to remain under pressure over the course of December, as weak cargo demand and ample vessel availability continue to weigh on the market. While temporary disruptions, such as the RBCT force majeure, may tighten supply briefly, any significant upward movement in rates is unlikely until cargo volumes pick up or prompt vessel availability decreases.

Leave a Reply