- HRC imports fall 40%, semis rise fourfold

- Imports from Japan, China drop by 38-53%

- India stays net importer but deficit shrinks

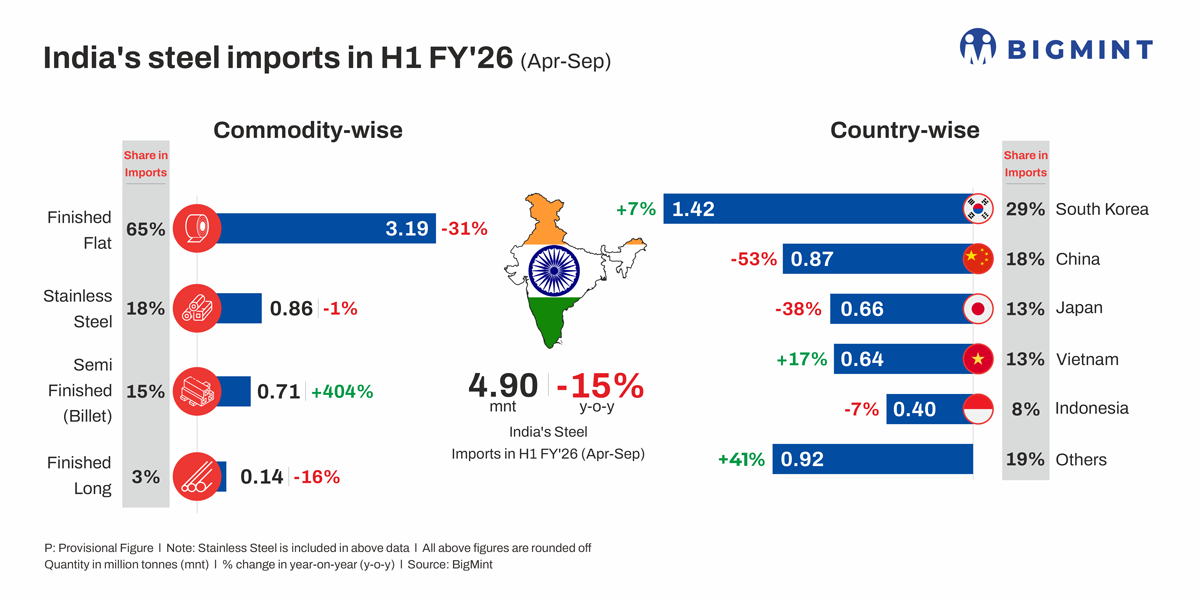

Morning Brief: Indian steel imports (including stainless steel) dropped by 15% y-o-y in H1FY’26, with stricter trade norms stalling inflows from key regions. Imports totalled 4.90 million tonnes (mnt) in H1FY’26 compared to 5.78 mnt in the year-ago period, as per provisional data maintained with BigMint.

Commodity-wise scenario

India’s finished flat carbon steel imports stood at 3.19 mnt in H1FY’26, down by a steep 31% y-o-y. Hot-rolled coil (HRC) arrivals declined by 40% to 1.39 mnt, hit by the safeguard duty. Galvanised steel and electrical steel were down 25% and 23%, respectively.

Semi-finished imports increased by over 400% to 0.77 mnt. This was the only category to witness a strong increase.

Finished long imports totalled 0.14 mnt, down 16% y-o-y.

Stainless steel imports decreased by 7% to 0.81 mnt, on the back of an 18% drop in finished flat arrivals.

Country-wise break-up

South Korea, with which India has a free-trade agreement (FTA), was the top steel exporter to India during H1FY’26. Volumes grew 7% y-o-y to 1.42 mnt.

Next was China, with 0.87 mnt, reflecting a steep 53% drop y-o-y. Japan, another FTA partner, shipped 0.66 mnt, down 38% y-o-y. The implementation of the safeguard duty has helped India reduce inflows from China and Japan.

Shipments from Vietnam totalled 0.64 mnt, a 17% increase y-o-y. Largely, semi-finished products such as slabs have been arriving from Vietnam due to HRCs carrying higher landed costs due to the safeguard duty and, recently, the anti-dumping duty. Moreover, Vietnamese mills also possess valid Bureau of Indian Standards (BIS) licences to export slabs to India. The existence of an FTA has also facilitated rising imports from Vietnam.

Arrivals from Indonesia climbed up by 7% to 0.40 mnt. Notably, Russian shipments surged manifold to 0.33 mnt due to competitive pricing offered by exporters.

India remains net importer in H1FY’26

India continued to be a net importer in H1FY’26, logging a trade deficit of 0.47 mnt. This is despite a 40% rise in export volumes to 4.43 mnt.

However, the 0.47 mnt gap indicates substantial progress in lifting exports while scaling down imports. The volume is much lower than the 4.38 mnt recorded in FY’25.

Factors influencing Indian steel imports in H1FY’26

Safeguard duty increases landed cost of imports: Following the implementation of the 12% safeguard duty, landed costs of flat steel imports have consistently remained higher than domestic prices. For example, domestic HRCs (INR 49,500/t exy-Mumbai) were cheaper by around INR 7,500/t compared to Chinese imports (INR 57,088/t) in terms of landed costs. The gap widened to INR 8,000/t in early October, due to a steeper decline in domestic prices.

Additionally, the landed cost of imports from Japan (INR 52,445/t) was higher by around INR 3,000/t in early September.

Anti-dumping duties foster caution: India has also announced anti-dumping duties on HRCs from Vietnam and electrical steel from China.

Additionally, in early October 2025, the government initiated an anti-dumping investigation into cold-rolled stainless steel flats imports originating in China, Indonesia, and Vietnam.

These protectionist measures have made buyers cautious about sourcing imports due to their higher costs.

India tightens raw material quality mandate: As a non-trade barrier, the government has mandated that raw materials used in the manufacturing of imported steel adhere to BIS quality norms. Although implementation has been deferred and certain exemptions have been provided, the move is expected to reduce India’s import burden by curbing the entry of cheap, substandard material.

Meanwhile, India has also delayed BIS licence renewals of Chinese steelmakers.

Outlook

The near-term outlook for Indian steel imports remains simple: Volumes may continue to fall in the near future, given the impact of trade barriers and tightened quality norms. In the case of HRCs, the wide price differential between overseas-origin and domestic material will keep import demand low. However, grades that are inaccessible in India will continue to be sourced from overseas, though in the medium term, this trend may start waning with the development of indigenous manufacturing units.

Leave a Reply