- CIL’s offtake dips y-o-y in Nov’25 amid cautious procurement

- Production drops 4%, offtake declines 2% y-o-y in Apr-Nov’25

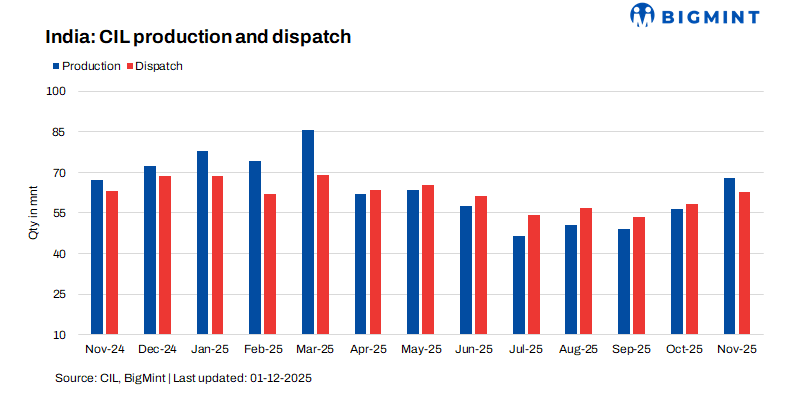

Coal India Limited (CIL) posted an increase in coal production in November 2025, with subsidiaries SECL and MCL logging growth. However, production declined y-o-y during April-November 2025, reflecting shifting demand dynamics. Logistical constraints, localised challenges, and selective capacity utilisation strategies influenced operations during both periods.

CIL records growth y-o-y in Nov’25

CIL achieved 68 mnt of coal production in November 2025, posting 1.2% growth y-o-y. Growth was bolstered by strong contributions from SECL and MCL, which recorded y-o-y gains of 18.6% and 5.4%, supported by improved mine availability and enhanced evacuation systems. Conversely, ECL, BCCL, NCL, and WCL experienced declines due to land acquisition delays, environmental bottlenecks, and operational constraints.

Coal offtake moderated to 62.7 mnt, reflecting a marginal 0.3% y-o-y contraction. The muted lifting indicates cautious procurement by power and industrial sectors, which continued to rely on existing inventories and blended coal strategies.

Production, offtake decline y-o-y in Apr-Nov’25

During the April-November 2025 period, CIL produced 453.5 mnt of coal, registering a 3.7% decline. Offtake stood at 478.9 mnt, down 2.0% y-o-y, as utilities maintained adequate stock buffers amid stable demand conditions. While BCCL, CCL, and WCL registered notable production declines, gains at SECL and MCL partially cushioned the impact, reinforcing their strategic role in CIL’s supply network.

Factors influencing the weaker performance y-o-y include the following:

- Operational leverage in key units: Enhanced mechanisation and streamlined supply chains supported efficiency gains in high-performing subsidiaries, such as MCL and SECL.

- Subdued offtake due to weak demand: Stable power sector inventories and moderate industrial coal use kept dispatches aligned with requirement-based procurement.

Strategic takeaways

CIL’s performance signals a deliberate pivot from uniform expansion to targeted, efficiency-oriented growth. The company continues to balance supply effectively without price distortion, underscoring disciplined operational management.

Outlook

The near-term trajectory remains demand-sensitive. Winter power consumption trends, subsidiary-level operational recovery, and potential restocking by steel and cement industries will determine the pace of coal lifting. Despite performance disparities, CIL’s strong asset base and resilient production in key subsidiaries position it for gradual, demand-aligned improvement as the fiscal year progresses.

Leave a Reply