- CIL production drops amid weak subsidiary output

- Dispatches remain stable despite uneven demand trends

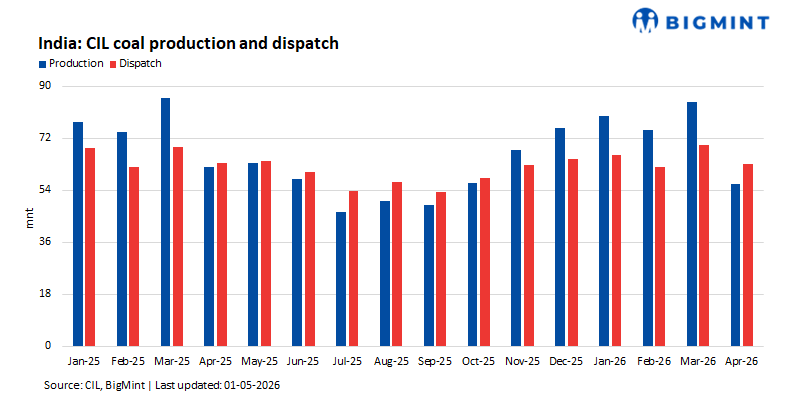

Coal India Limited (CIL) reported a notable contraction in coal production for April 2026, with output at 56.1 million tonnes (mnt), reflecting a 9.7% year-on-year (y-o-y) decline from 62.1 mnt in April 2025. On a sequential basis, production fell sharply by 33.6% from 84.5 mnt in March 2026. This decline is largely attributable to the typical post-March normalization, as March output is usually elevated due to year-end targets, alongside operational constraints and lower working days at the start of the fiscal year.

Dispatches show relative resilience despite softer output

Coal dispatches stood at 63.2 mnt in April 2026, marking a relatively modest decline of 2% y-o-y compared to 64.5 mnt in April 2025, while also dropping 9.1% month-on-month (m-o-m) from 69.5 mnt in March 2026. The less pronounced fall in dispatches versus production suggests continued drawdown of inventories and steady demand from key consuming sectors, even as supply tapered following the fiscal year-end surge.

Subsidiary-level output weakness weighs on overall production

The overall production decline was driven by significant output reductions across major subsidiaries. Northern Coalfields Limited (NCL), Mahanadi Coalfields Limited (MCL), and Bharat Coking Coal Limited (BCCL) recorded steep y-o-y declines of 23.6%, 13.9%, and 41.3%, respectively, likely due to mine-specific operational challenges, lower stripping activity, and logistical constraints. Western Coalfields Limited (WCL) and Eastern Coalfields Limited (ECL) also registered moderate declines, while Central Coalfields Limited (CCL) remained largely stable, indicating a mixed operational landscape across regions.

In contrast, South Eastern Coalfields Limited (SECL) stood out as the sole major subsidiary posting growth, with production rising 9.3% y-o-y. The increase can be attributed to improved mine productivity, better evacuation infrastructure, and relatively stable operating conditions, which helped partially offset declines seen across other subsidiaries.

Mixed dispatch trends reflect demand-supply adjustments

At the subsidiary level, dispatch performance remained uneven. MCL and SECL reported healthy growth in offtake at 7.2% and 4.1% y-o-y, respectively, supported by strong demand and efficient logistics.

However, this was offset by sharp declines in dispatches from BCCL (-26.7%), CCL (-12.4%), and NCL (-12.5%), reflecting weaker production and possibly subdued lifting by end-users. ECL posted a moderate increase of 4.6%, while WCL remained broadly stable with a marginal dip.

Outlook

The April performance reflects a seasonal reset following the March peak, rather than a structural demand slowdown. While production may remain range-bound in the near term due to operational and seasonal factors, steady dispatch levels indicate underlying demand resilience. Future trends will hinge on monsoon-related disruptions, inventory levels at power plants, and the pace of industrial consumption.

Leave a Reply