- Range-bound scrap with slight downside bias

- Billet prices decrease by INR 500/t w-o-w

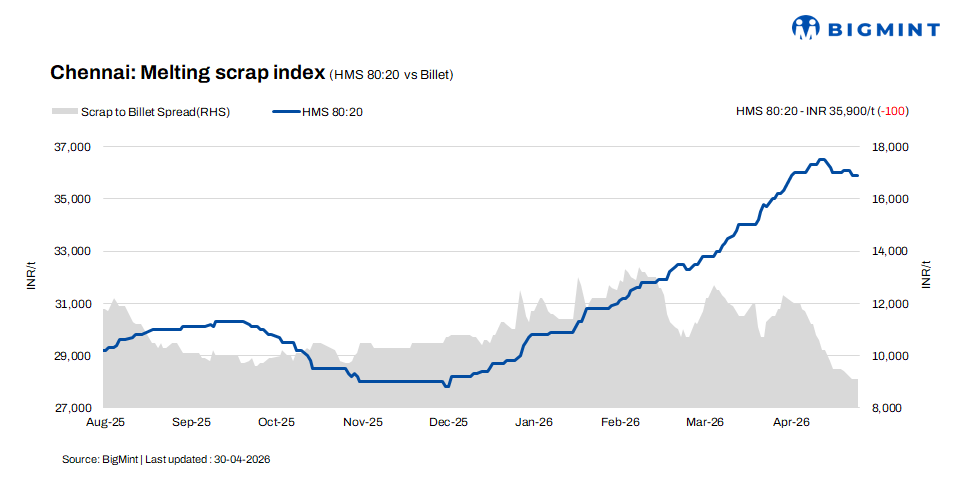

According to BigMint’s latest assessment, HMS (80:20) scrap prices declined by INR 100/t w-o-w to INR 35,900/t, while remaining stable on a daily basis. In the semi-finished segment, billet prices held steady d-o-d at INR 45,000/t, but recorded a weekly decline of INR 500/t, reflecting softer market sentiment.

Similarly, in the finished steel segment, rebar prices dropped by INR 200/t w-o-w to INR 51,500/t, with no change observed on a day-on-day basis. The overall trend indicates subdued demand and cautious buying activity, leading to mild corrections across steel and scrap markets.

Imported and domestic price trends

Market participants reported that Australia-origin shredded scrap was offered at $395-398/t CFR Chennai, while HMS (80:20) was quoted at $385-387/t CFR. However, buyers were bidding $5-10/t lower than prevailing offer levels, reflecting cautious market sentiment.

Despite this gap, a transaction was concluded, with 1,000 t of Costa Rica-origin HMS (60:20) booked at $342/t CFR Chennai. The deal indicates selective buying interest at lower price levels, while higher offers continue to face resistance. Overall, the market remains price-sensitive, with buyers preferring competitively priced cargoes.

In the domestic market, HMS (80:20) scrap prices were quoted at INR 35,500-36,000/t for spot deals with immediate payment. Transactions on extended credit terms were concluded at higher levels of INR 36,000-36,500/t. Overall, market activity remained largely concentrated within the INR 35,500-36,500/t range, with price variations driven by payment terms and mill-specific requirements. The trend reflects stable market conditions, with steady trading and balanced supply-demand dynamics.

Buyer-supplier sentiments

A mill representative noted that lower sponge iron offers from neighbouring states have made them more competitive compared to local merchant suppliers, prompting buyers to prefer procurement from outside markets, resulting in slower sales for local material. Meanwhile, billet traders are holding back inventories, anticipating a potential price increase after the state assembly election results on 4 May 2026.

On the demand side, rebar consumption remains slightly subdued, as several government projects are currently slowed down due to labour shortages. This has led to cautious buying activity in the finished steel segment, keeping overall market sentiment soft.

A scrap supplier indicated that HMS (80:20) prices are currently hovering in the range of INR 35,500-36,500/t, with variations depending on payment terms and mill-specific requirements. Extreme summer conditions have led to labour shortages, disrupting scrap processing activities and limiting effective supply.

At the same time, the continued decline in semi-finished and finished steel prices has prompted buyers to push for lower scrap procurement prices to maintain conversion margins. However, despite this pressure, ongoing commercial gas supply issues and slow processing are keeping scrap availability tight, preventing any sharp correction in prices.

Regional comparison

In the western India-based Jalna market, billet prices increased by INR 500/t to INR 44,000/t, while HMS (80:20) scrap prices rose by INR 300/t to INR 33,300/t. Conversely, rebar prices declined by INR 500/t to INR 49,000/t.

Market participants noted that rebar demand has weakened over the past few days, leading to a correction in prices. The divergence in price trends indicates stronger sentiment in the raw material and semi-finished segments, while the finished steel segment remains under pressure due to subdued consumption and slower trading activity.

Outlook

Chennai scrap prices are expected to remain range-bound with a slight downward bias, as weak billet and rebar demand continues to pressure sentiment. However, tight scrap availability due to gas and labour constraints may limit any sharp correction. Mills are likely to continue need-based procurement, with price movements expected to remain restricted within INR +/- 200-500/t.

Leave a Reply