- Rising steel stocks, production cuts impact scrap demand

- Mills currently holding 15-20 days of finished steel stocks

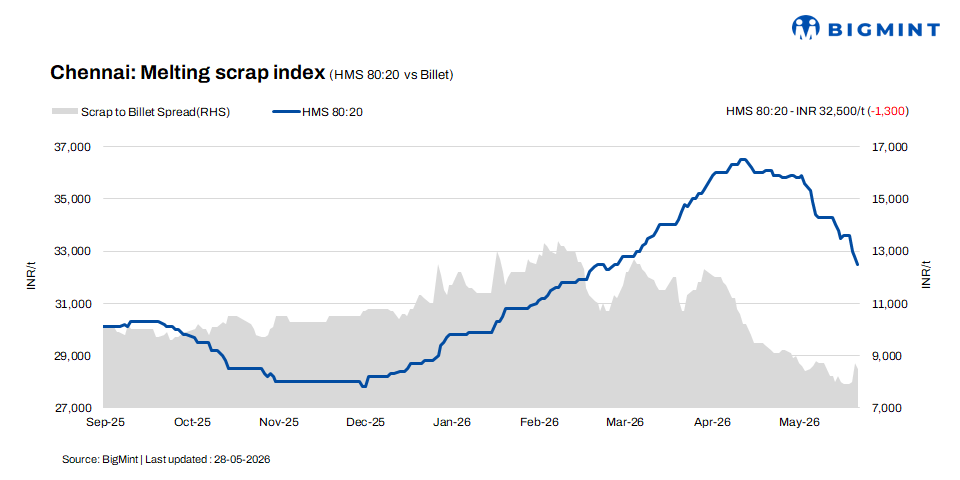

According to BigMint’s latest assessment, HMS (80:20) scrap prices in Chennai declined by INR 300/t d-o-d to INR 32,500/t, registering a w-o-w correction of INR 1,300/t. In the semi-finished segment, billet prices dropped by INR 500/t d-o-d to INR 41,000/t, registering a weekly decline of INR 1,000/t, reflecting softer market sentiment.

Similarly, in the finished steel segment, rebar prices fell by INR 1,500/t w-o-w to INR 47,500/t, while remaining unchanged d-o-d. The price trend indicates sluggish finished steel demand and cautious buying activity, which continue to pressure overall market sentiment.

Imported and domestic price trends

Market participants reported that Australia-origin shredded scrap was offered at $375-380/t CFR Chennai, while HMS (80:20) was quoted at $355-360/t CFR. However, buyers were bidding nearly $15-20/t lower than prevailing offer levels, reflecting cautious sentiment in the market.

According to sources, weak finished steel demand and the continued decline in steel prices have discouraged buyers from booking imported scrap at current offer levels. Market participants remain cautious about fresh purchases, anticipating further corrections in steel prices, which have continued to limit import buying activity.

In the domestic scrap market, HMS (80:20) prices were quoted at INR 32,000-32,500/t for immediate payment deals, while transactions involving extended credit terms were settled at INR 32,500-33,000/t.

Overall, trading activity remained largely confined within the INR 32,000-33,000/t range, reflecting balanced market conditions despite softer downstream steel demand. Variations in transaction prices were mainly attributed to payment terms and mill-specific volume requirements. Buyers continued to adopt a cautious procurement strategy, resulting in controlled and requirement-based trading activity across the market.

Buyer-supplier sentiments

According to sources, the Chennai steel market remains under pressure amid weak demand conditions. Despite production cuts and lower operating rates of around 60-70%, inventory levels continue to rise, with mills currently holding nearly 15-20 days of stock. Weak demand in the finished steel segment has significantly impacted material offtake, adding pressure on steel producers.

Additionally, billet demand remains sluggish, primarily due to subdued finished steel demand in the market. The slowdown in downstream consumption has continued to weigh on billet movement, prompting mills to maintain a cautious production approach. Overall, weak demand fundamentals and elevated inventories continue to pressure market sentiment in the region.

A market participant noted that HMS (80:20) scrap prices are currently ranging between INR 32,000-33,000/t, depending on payment terms and procurement volumes. Although scrap supply remains slow at mills, weak demand in the finished steel segment has compelled mills to reduce scrap procurement prices to maintain conversion costs and operating margins.

Meanwhile, higher imported scrap offer levels continue to discourage fresh bookings, as elevated landed costs remain unattractive for buyers. The combination of subdued steel demand, tight domestic scrap supply, and costly imports is creating operational challenges for producers, impacting production planning and overall market sentiment.

Regional comparison

In the Jalna market, billet and HMS (80:20) scrap prices remained unchanged d-o-d at INR 41,300/t and INR 33,500/t, respectively. While rebar prices fell by INR 100/t to INR 46,300/t. Market participants reported that trade activity has improved in recent days compared to the slower pace witnessed over the past few weeks, reflecting a modest recovery in sentiment.

However, fuel shortages continue to affect transportation logistics, resulting in limited availability of commercial vehicles in the region. Consequently, some mills are processing orders only when buyers arrange immediate transport for finished steel dispatches. On the raw material side, scrap supply remains moderately tight, as suppliers are reluctant to release material at lower price levels.

Outlook

The near-term outlook for the Chennai scrap market remains cautious, with subdued finished steel demand and elevated inventories continuing to pressure sentiment. At the same time, limited scrap availability and higher imported scrap costs are expected to support domestic prices. Mills are likely to continue need-based procurement to manage conversion costs. Overall, prices are expected to fluctuate within INR +/- 200-500/t.

Leave a Reply