- High rebar inventories reduce demand for billets

- Persistent rainfall, liquidity crunch hinder trade

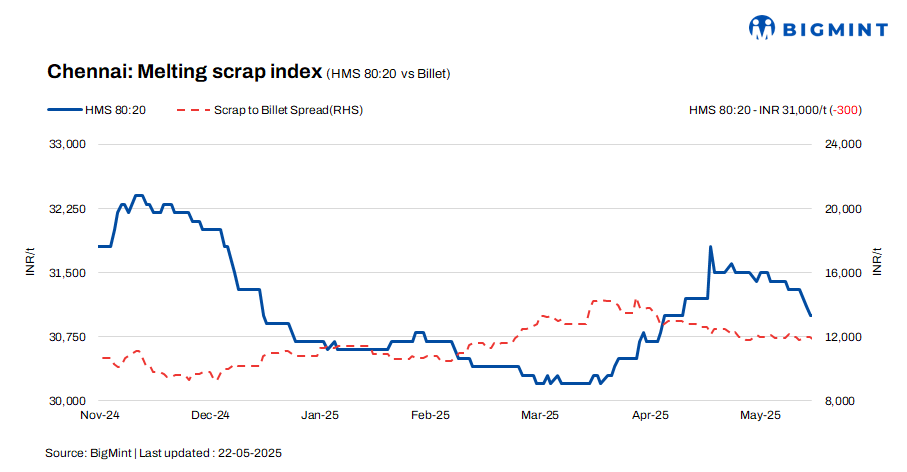

Chennai’s steel market witnessed a decline w-o-w but stability d-o-d, as per BigMint’s latest assessment. HMS (80:20) scrap prices decreased by INR 300/tonne (t) w-o-w to INR 31,000/t. However, there was no change d-o-d. Billet prices remained stable d-o-d but fell by INR 500/t w-o-w to INR 42,800/t. Rebar prices followed a similar trajectory, dropping by INR 200/t w-o-w to INR 47,800/t, with no d-o-d change. These trends indicate a modest drop in steel prices w-o-w, following tepid demand.

Imported, domestic scrap price trends

A scrap trader noted that offers for shredded from Australia were in the range of $365-370/t CFR Chennai, while those for HMS 80:20 were slightly lower, at $345-350/t. Meanwhile, demand for imported scrap was weak, with no significant deals observed.

Domestic HMS (80:20) prices in Chennai were at INR 30,500-31,000/t for spot deals with immediate payment. For transactions with extended credit, prices were slightly higher, at INR 31,000-31,500/t. Most offers and concluded deals fell within the INR 30,500-31,500/t band, indicating a stable pricing range in the domestic scrap market.

Buyer-supplier sentiments

A mill representative recently informed BigMint that trade activities in Chennai have slowed down over the past couple of weeks. This slowdown has been compounded by ongoing rainfall in the region. Currently, mills have about 15-20 days’ worth of rebar inventory, which has led to an increase in billet supply in the market. The combination of lower trade activity and higher billet availability contributed to the downtrend in the steel and scrap markets.

According to a scrap supplier, HMS 80:20 was priced at INR 30,500-31,500/t, depending on the payment terms. A liquidity crunch in the market has contributed to a slowdown in trade activity in recent weeks. Demand for billets and rebars has also declined, prompting mills to reduce their scrap buying prices in an effort to maintain their conversion costs.

Regional comparison

In the Jalna market of western India, billet prices saw a decrease of INR 200/t d-o-d to INR 42,300/t. Similarly, rebar prices dropped by INR 100/t d-o-d to INR 47,700/t. However, HMS 80:20 prices remained stable d-o-d at INR 32,700/t. Decent trade activity was observed across both the semi-finished and finished steel segments, while scrap supply at mills remained at a moderate level.

Outlook

Sources indicate that scrap prices are expected to remain range-bound in the short term, with potential fluctuations of INR +/- 500/t. This stability is largely attributed to ongoing uncertainty in the finished steel market, where both buyers and sellers are adopting a cautious approach. The cautious sentiment in the finished steel trade is likely to keep scrap prices within this limited range for the foreseeable future.

Leave a Reply