- Projects do need-based buying, avoid bulk purchases

- Liquidity squeeze further limits trade activities

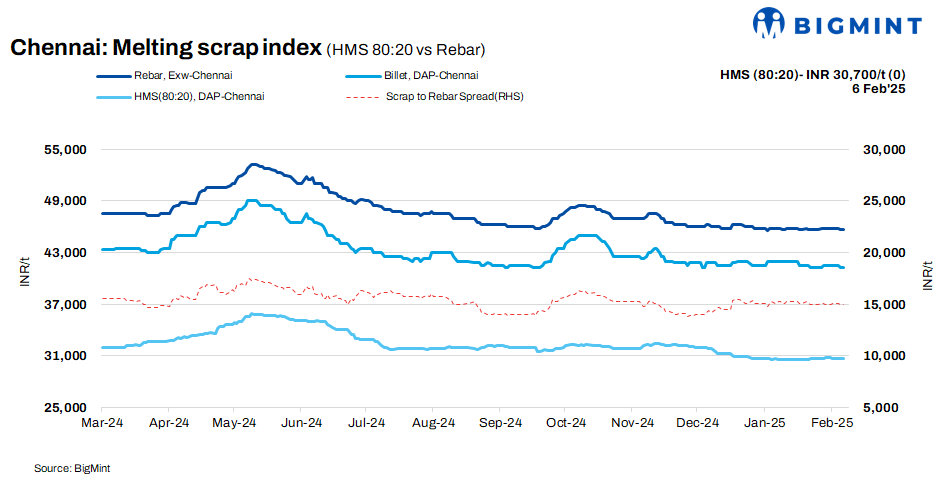

According to BigMint’s latest assessment, prices of HMS (80:20) in Chennai decreased by INR 100/t w-o-w, reaching INR 30,700/t. Despite this drop, prices remained stable on a d-o-d basis. Billet prices held steady d-o-d at INR 41,200/t but experienced a minor reduction of INR 300/t w-o-w. Rebar prices also remained unchanged on a d-o-d basis at INR 45,700/t, but decreased by INR 100/t over the week. Overall, the market sentiment remained cautious along with moderate trade activity.

Imported, domestic market trends

According to a scrap trader, shredded scrap offers from Australia are priced at $360-365/t, CFR Chennai, while HMS 80:20 is offered at $350-355/t. Despite these offers, demand remains weak, as buyers are opting for more affordable domestic scrap, which is priced lower than the imported material.

Domestic prices of HMS (80:20) scrap are currently quoted between INR 30,500/t and INR 31,000/t for buyers with seven-day payment terms. For transactions involving extended payment terms, the price range is INR 31,000-31,500/t. The bulk of offers fell within the INR 30,500-31,000/t range, and most deals were finalized within this band, reflecting stable market conditions.

Buyer-supplier sentiments

A mill representative told BigMint that the demand for finished steel remains subdued, with buyers refraining from bulk purchases. Instead, they are focusing on need-based procurement. Currently, demand is being driven primarily by project-based requirements.

Another market source informed BigMint that mills are currently selling rebar for projects at INR 44,500-45,000/t, while retail prices are being quoted at INR 45,500-46,000/t. Major mills are offering billets at discounted prices for advance payments, opting for this approach instead of selling at higher rates with credit terms.

A scrap supplier said that HMS (80:20) scrap prices in the domestic market are currently hovering at INR 30,500-31,500/t, depending on payment terms. Some mill owners have started quoting as low as INR 30,000/t, but supply at this price level is limited. The market is currently experiencing a liquidity squeeze, which has led to reduced trading activity, particularly in the finished steel sector in recent weeks.

Regional comparison

In the western India-based Jalna market, billet prices increased by INR 200/t d-o-d to INR 41,600/t. Meanwhile, HMS 80:20 prices saw a d-o-d decline of INR 300/t, settling at INR 31,500/t. Rebar prices remained stable d-o-d at INR 46,800/t. Overall, trade activity in the finished steel sector remained average, with mills reporting moderate scrap supply.

Outlook

While the market is currently experiencing a slowdown, scrap prices are expected to remain within a narrow band in the near term, with potential variations of INR +/- 500/t. Market conditions will play a crucial role in influencing these price movements in the short term.

Leave a Reply