- Liquidity crunch continues to hinder scrap trade

- Rebar prices dip w-o-w but demand improves

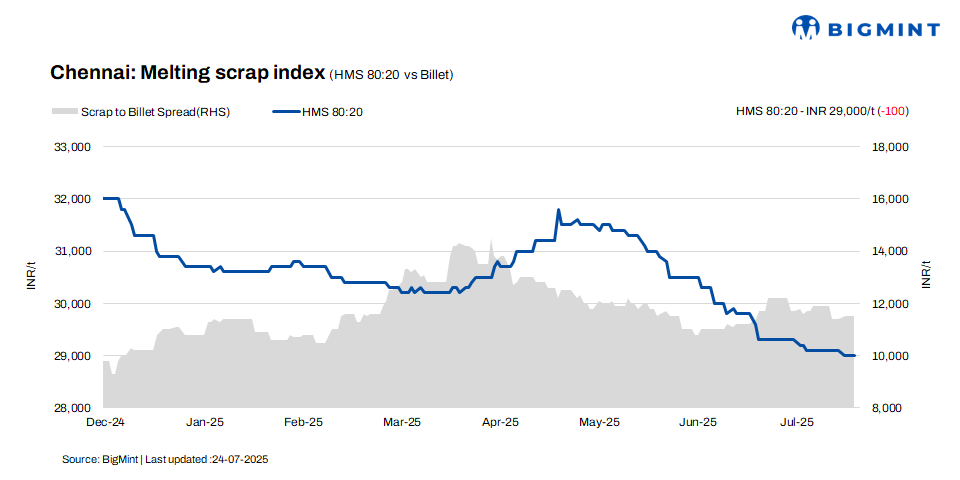

HMS (80:20) prices in Chennai softened by INR 100/tonne (t) w-o-w to INR 29,000/t, as per BigMint’s recent assessment, though d-o-d levels remained flat, indicating a cautious market sentiment.

Billet prices remained stable at INR 40,500/t on both d-o-d and w-o-w terms, reflecting balanced demand-supply conditions.

Rebar, while steady at INR 45,300/t on a d-o-d basis, saw a marginal w-o-w correction of INR 200/t, signalling some softness in downstream buying despite otherwise steady fundamentals.

Imported, domestic price trends

According to a scrap trader, current offers for shredded from Australia were at $355-360/t CFR Chennai, while HMS 80:20 was offered in the range of $335-340/t. However, bids softened by $5-10/t, reflecting cautious market sentiment. Market sources indicate that buyers prioritised spot bookings of readily available material, showing limited interest in pre-booking cargoes with extended delivery timelines.

In the Chennai market, domestic HMS (80:20) was traded at INR 29,000-29,500/t for spot deals with immediate payment, whereas transactions concluded on extended credit terms ranged slightly higher at INR 29,500-30,000/t. The prevailing trade band of INR 29,000-30,000/t underscores the premium associated with credit-based deals, highlighting the notable influence of liquidity conditions on pricing and transaction execution.

Buyer-supplier sentiments

The sponge iron supply chain witnessed minor constraints, with only select mills actively participating in merchant sales, thereby limiting availability. On the demand side, billets continued to witness healthy buying interest, and rebar demand strengthened compared to recent weeks, offering some stability to market sentiment. However, reports of incoming steel supplies from neighboring states exerted competitive pressure on local mills, discouraging any upward revision in their offer prices.

As per a scrap supplier, HMS (80:20) was traded within the range of INR 29,000-30,000/t, with price realisations influenced by varying payment terms. Liquidity constraints continued to weigh on market sentiment, although marginal improvement in finished steel trade activity was observed. This development raised cautious optimism that price stability or a gradual recovery may emerge in the near term, offering some support to the overall market.

Regional comparison

In the Jalna market of western India, rebar and HMS (80:20) prices rose by INR 200/t d-o-d each, reaching INR 43,500/t and INR 30,500/t, respectively, while billet tags saw a d-o-day increase of INR 400/t, settling at INR 39,800/t. An uptick in finished steel demand drove a notable improvement in trade activity. Scrap suppliers started quoting higher prices in response to the active demand for finished steel, but scrap availability at mills remained aligned with current production requirements.

Outlook

Market sources suggest that scrap prices are likely to remain range-bound in the near term, with possible fluctuations of INR +/-500/t. Given the improved trade activity and overall positive market sentiment, there is a likelihood of moderate upward movement in steel prices, offering potential support to overall market stability.

Leave a Reply