- Semi-finished prices drop by INR 500/t w-o-w

- Improved trade in steel drives up scrap offers

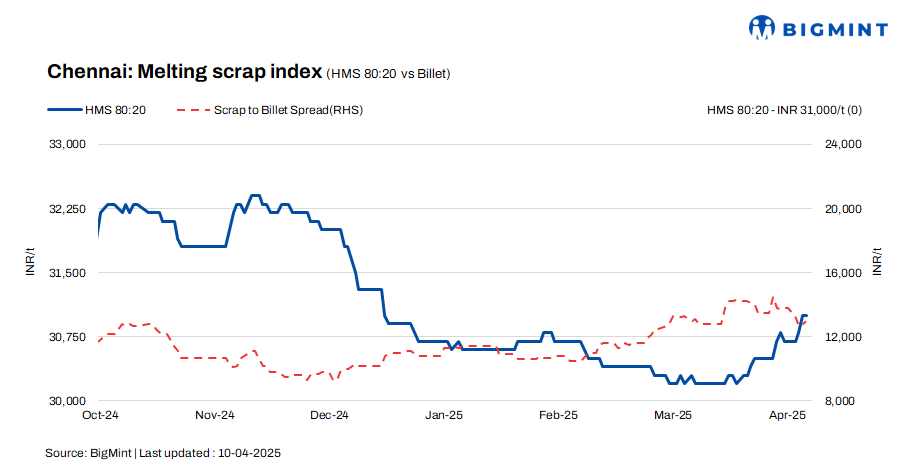

HMS (80:20) scrap prices in Chennai rose by INR 200/t w-o-w, to INR 31,000/t, as per BigMint’s latest assessment. On a d-o-d basis, prices held steady.

Billet prices recorded a w-o-w drop of INR 500/t, and are currently hovering at INR 44,000/t, though these increased by INR 200/t d-o-d.

Rebar prices remained unchanged w-o-w but witnessed a modest uptick of INR 200/t d-o-d, bringing the current level to INR 48,700/t. The market is reflecting mixed sentiments, with scrap prices firming up, billets showing partial recovery, and rebar holding steady with slight daily gains.

Imported, domestic price trends

Chennai’s imported scrap market continues to remain sluggish, as buyers are showing a clear preference for more cost-effective domestic alternatives such as sponge iron and local scrap. Currently, Australian HMS is being offered at $365/t CFR Chennai, while shredded scrap offers are in the range of $385-390/t CFR. Market sources indicate that a Chennai-based mill is in negotiations for a potential bulk purchase of 20,000-22,000 t of CR busheling scrap from South Korea, though the deal is still under discussion and not yet finalised.

Domestic HMS (80:20) scrap prices are currently trading in the range of INR 31,000-31,500/t for buyers making immediate payments. For transactions involving extended credit terms, prices have increased to INR 31,500-32,000/t. The bulk of market offers are concentrated in the INR 31,000-31,500/t range, with most deals being concluded at these levels. This reflects the prevailing pricing structure and steady market sentiment, particularly for prompt-payment transactions.

Buyer-supplier sentiments

A mill representative informed BigMint that billet prices experienced a decline last week due to a sharp drop in prices from neighbouring states. However, this week has seen a recovery in demand in Chennai, with additional support coming from renewed buying interest in the down south market. This regional demand is helping stabilise and support billet prices in Chennai. Meanwhile, some mills have previously booked imported scrap shipments arriving this month. With current imported scrap offers on the higher side compared to more competitive domestic prices, buyers are now shifting focus toward domestic scrap procurement and pausing further import bookings.

According to a local scrap supplier, HMS (80:20) scrap prices in the domestic market are currently trading in the range of INR 31,000-32,000/t, with slight variations, depending on payment terms. Over the past month, billet and rebar markets have seen consistent improvement in both demand and pricing. During this period, scrap prices remained stable, moving within a narrow range. This upward trend in finished steel has now started to reflect in scrap pricing, which is showing signs of going up.

Regional comparison

In the Jalna market, billet prices increased by INR 200/t to INR 43,900/t. HMS (80:20) scrap also saw a minor price rise of INR 100/t, now at INR 32,900/t. Rebar prices, however, remained unchanged at INR 49,300/t. The market observed moderate trade activity in finished steel, while scrap prices stayed within a narrow range. Most buyer bids for HMS scrap were reported between INR 32,700-33,200/t, indicating a balanced outlook with controlled pricing momentum in the regional market.

Outlook

As demand for semi-finished and finished steel continues to improve in the region, market participants are maintaining an optimistic outlook on the steel sector’s performance in the near term. Despite the ongoing preference for domestic scrap over imported alternatives, the positive sentiment in the steel market is likely to support a gradual upward movement in scrap prices. However, any price increases in scrap are expected to remain within a limited range due to the relatively higher cost of imported scrap compared to domestic.

Leave a Reply