- Semi-finished steel prices drop by INR 500/t w-o-w

- Finished steel trades slow down in recent days

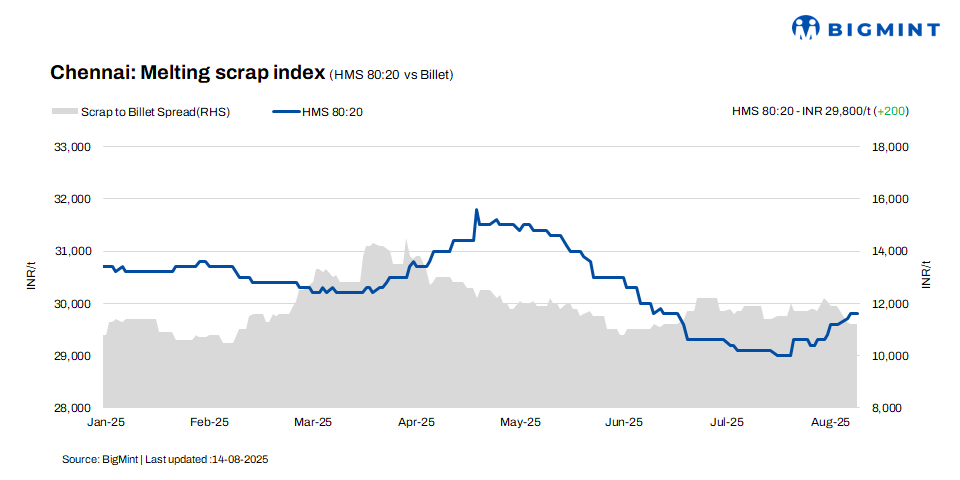

According to BigMint’s latest assessment, HMS (80:20) scrap prices in Chennai rose by INR 200/t w-o-w to INR 29,800/t, while remaining stable d-o-d. Billet prices held steady d-o-d but declined INR 500/t w-o-w to INR 41,000/t. Similarly, rebar prices were unchanged d-o-d but saw a w-o-w dip of INR 200/t to INR 45,500/t. The market is currently showing mixed signals, with firming scrap prices contrasting with softening finished steel prices.

Imported and domestic price trends

As per a scrap trader, imported shredded scrap is currently being offered at $360-365/t, while HMS (80:20) is priced at $335-340/t. However, Chennai’s imported scrap market remains sluggish, with buyers showing preference for more economical domestic alternatives such as sponge iron and locally available scrap, reflecting a cost-driven purchasing trend.

Domestic HMS (80:20) scrap prices are currently quoted in the range of INR 29,500-30,000/t for prompt payment transactions, while offers for extended credit terms have moved higher to INR 30,000-30,500/t. The majority of market offers and concluded deals fall within this INR 29,500-30,500/t range, indicating a stable pricing structure aligned with prevailing payment conditions.

Buyer-supplier sentiments

A mill representative informed BigMint that billet prices declined last week, influenced by falling prices in neighbouring states. Concurrently, trade activity in finished steel has slowed in recent days. Despite this, pellet-based sponge iron is being offered in Chennai at INR 27,000-27,500/t DAP, indicating stable demand for raw materials even amid weaker finished steel movement.

According to a local scrap supplier, domestic HMS (80:20) scrap prices are currently ranging between INR 29,500 and INR 30,500/t, with slight variations based on payment terms. Despite recent declines in billet and rebar prices, buyers are maintaining consistent scrap procurement levels, driven by tight supply conditions in the market.

Regional comparison

In the Jalna market of western India, prices for rebar, and HMS (80:20) remained stable at INR 44,000/t, and INR 31,000/t, respectively. While billet prices saw a small increase of INR 100/t to INR 40,200/t.Trade activity in finished steel has slowed in recent days. Amid this, mills have adjusted their input strategy, incorporating only 20–30% sponge iron in their charge mix, as scrap proves more readily available and cost-efficient.

Outlook

Despite the ongoing market slowdown, scrap prices are expected to remain range-bound in the near term, with fluctuations likely restricted to around INR +/-500/t. Key pricing drivers will include mill inventory levels, demand-side activity, and overall sentiment within the steel value chain.

Leave a Reply