- Imported scrap trading remains muted amid unviable offers

- Rebar inventories rise to 30-40 days; mills focus on stock liquidation

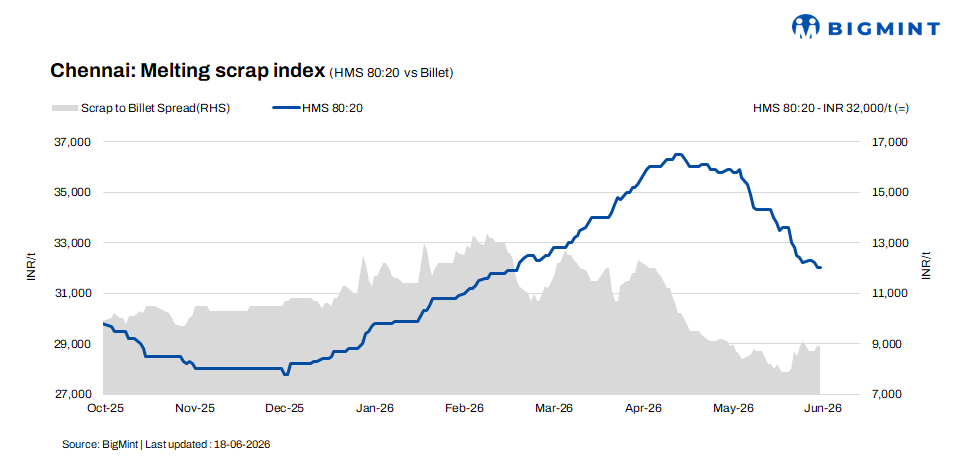

HMS (80:20) scrap prices in Chennai remained largely stable w-o-w at INR 31,800-32,200/t, according to BigMint’s latest assessment, reflecting balanced domestic availability and cautious procurement by mills. In the semi-finished segment, billet prices improved by around INR 200/t w-o-w to INR 41,200/t, supported by slightly better buying activity and improved sentiment in the downstream market.

On the finished steel side, demand for billets and rebars remained subdued. Market sources indicated that weak offtake from infrastructure and project segments continued to weigh on steel consumption, prompting mills to closely monitor production levels and inventories.

Imported and domestic price trends

Market participants reported that Australia-origin shredded scrap was offered at $380-385/t CFR Chennai, while HMS (80:20) was quoted at $355-360/t CFR. Despite the ongoing shortage of quality scrap in the domestic market, buying interest for imported material remained subdued.

Sources indicated that buyers continued to bid nearly $15-25/t below prevailing offer levels, reflecting cautious sentiment and limited appetite for fresh bookings. Additionally, domestic scrap continues to be more economically viable than imported material, discouraging significant import activity in the Chennai market.

In the domestic market, HMS (80:20) scrap prices were quoted at INR 31,800-32,200/t for immediate payment deals, while credit-based transactions were concluded at slightly higher levels depending on payment terms and volumes.

Overall, trading activity remained concentrated within the INR 31,800-32,200/t range, reflecting stable supply-demand fundamentals. Variations in deal prices were primarily driven by payment terms, grade specifications, and mill-specific procurement requirements. Market participants continued to adopt a need-based purchasing strategy amid subdued finished steel demand.

Buyer-supplier sentiments

According to market participants, mills are under increasing pressure to liquidate rebar inventories, which have risen to around 30-40 days amid weak offtake from infrastructure and construction sectors. The buildup in finished steel stocks has prompted several producers to focus on inventory reduction rather than fresh production, keeping demand for billet and scrap largely need-based despite stable raw material prices.

Outlook

The Chennai scrap market is expected to remain largely stable in the near term. While billet prices have shown some recovery from recent lows, demand recovery in the finished steel segment remains gradual. Stable domestic scrap availability and the limited viability of imported scrap due to elevated landed costs are likely to provide support to prices. Mills are expected to continue need-based procurement while focusing on inventory management and closely monitoring rebar demand and conversion economics. Scrap prices are likely to remain stable within a narrow range, with any movement expected to be limited in the near term.

Leave a Reply