- Billet tags drop by INR 700/t w-o-w, stable d-o-d

- 27,000-t cargo arrived, may impact prices further

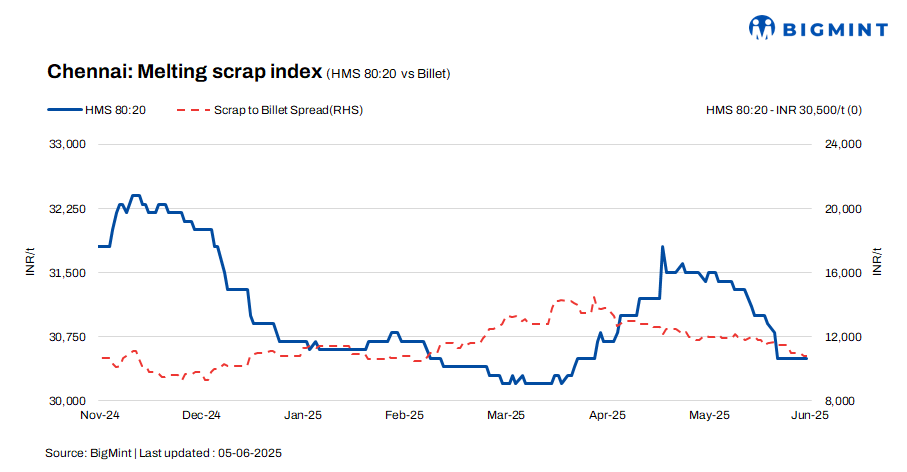

As per BigMint’s latest assessment, HMS (80:20) scrap prices in the Chennai market held steady both d-o-d and w-o-w at INR 30,500/tonne (t), amid subdued activity in the finished steel segment. Billet prices declined by INR 700/t on a weekly basis to INR 41,300/t, although they remained unchanged d-o-d. Similarly, rebar prices registered a modest weekly drop of INR 300/t to INR 47,000/t, with no daily movement observed.

Imported, domestic price trends

A scrap trader informed that offers for shredded scrap from Australia are currently in the range of $365-366/t CFR Chennai, while HMS 80:20 is being quoted at $345-350/t. Market sources have indicated that a vessel carrying approximately 27,000 tonnes of scrap reportedly arrived at Chennai Port during the current week. Confirmation of the cargo details is still awaited, but the arrival-if verified-could influence short-term sentiment and supply dynamics.

In the Chennai market, domestic HMS (80:20) scrap is currently trading at INR 30,000-30,500/t for spot transactions involving immediate payment. For trades with extended credit terms, prices are slightly higher, ranging between INR 30,500-31,000/t. The market trend indicates that most offers and concluded deals fall within the broader INR 30,000-31,000/t range, highlighting the influence of liquidity preferences and credit-based pricing dynamics.

Buyer-supplier sentiments

According to a mill representative, recent market conditions have led to a noticeable slowdown in steel trade activity, affecting both large infrastructure projects and retail-level transactions. This decline in finished steel demand is contributing to rising inventory levels at mills, heightening operational pressure. Should demand remain subdued, the market may be exposed to further downside risks in the near term.

According to a scrap supplier, HMS 80:20 scrap is currently trading in the range of INR 30,000-31,000/t, depending on payment terms. While scrap prices have remained stable, billet and rebar prices have seen downward adjustments. Ongoing liquidity constraints are putting pressure on raw material booking prices. With weakening demand for finished steel, mills may reduce procurement rates in the near term. Additionally, declining imported scrap offers are likely to weigh further on domestic market sentiment.

Regional comparison

In the Jalna market in western India, billet prices declined by INR 100/t to INR 40,900/t, while rebar prices registered a sharper drop of INR 400/t, settling at INR 46,100/t. HMS 80:20 scrap prices, however, remained stable at INR 32,200/t. The early onset of the monsoon has kept finished steel demand moderate and simultaneously disrupted scrap collection and supply chains. In response to limited scrap availability and to optimise conversion costs, mills are reportedly adjusting their charge mix by incorporating 20-40% of sponge iron.

Outlook

According to market sources, scrap prices are expected to remain range-bound in the near term, with anticipated fluctuations limited to INR +/-500/t. This stability is attributed to ongoing uncertainty in the finished steel trade, where cautious sentiment among both buyers and sellers is tempering activity. The prevailing market mood is likely to restrict price volatility and maintain a narrow trading range.

Leave a Reply