- Tight domestic scrap supply supports prices

- Billet tags drop by INR 500/t w-o-w, stable d-o-d

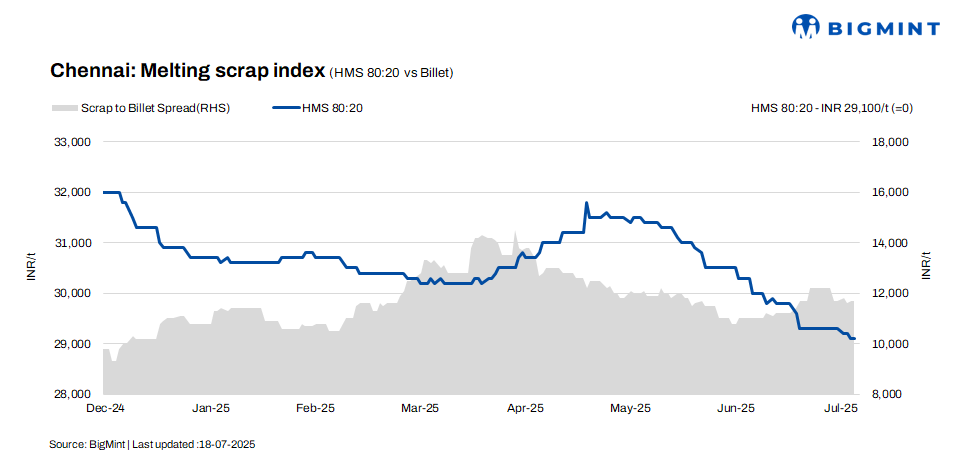

As per BigMint’s latest assessment, HMS (80:20) scrap prices in the Chennai market held steady both d-o-d and w-o-w at INR 29,100/tonne (t), amid subdued activity in the finished steel segment. Billet prices declined by INR 500/t on a w-o-w basis to INR 40,500/t, although they remained unchanged d-o-d. Similarly, rebar prices registered a modest w-o-w drop of INR 500/t to INR 45,500/t, with no d-o-d movements observed.

During the past week, billet and rebar prices witnessed a w-o-w decline, reflecting weak market sentiment and reduced buying interest from downstream sectors. However, HMS scrap prices remained largely stable despite this correction, supported by limited supply in the market and steady procurement from mills. This divergence indicates a temporary disconnect between the finished steel and scrap markets.

Imported market trends

India’s imported ferrous scrap market remained subdued as oversupply and limited buying interest continued to weigh on sentiments. Buyers remained cautious amid weak finished steel demand and bearish price expectations.

Bulk offers from the US were heard at $350-355/t CFR for shredded, $345/t for HMS 80:20, and $355-360/t for bonus grade. However, bids lagged at $340/t for shredded and $335/t for HMS, leaving most negotiations inconclusive.

Meanwhile, UK-origin HMS 80:20 hovered at $330-335/t CFR, under pressure from cheaper domestic scrap.

Australian shredded was offered at $365-370/t CFR Chennai, while HMS 1 was heard at $345-350/t. Despite a slight uptick in inquiries, actual trade remained limited as sellers held firm on prices, resisting further downside.

Ample availability and lower prices of domestic scrap continued to pull buyers away from imports, reinforcing the cautious market tone.

Domestic market trends

In Chennai, domestic HMS (80:20) was traded at INR 28,500-29,000/t for spot deals involving immediate payments. Meanwhile, transactions concluded on extended credit terms fetched slightly higher prices, closing in the range of INR 29,000-29,500/t. The prevailing trade range of INR 29,000-30,000/t highlights the credit premium in the market, underlining how liquidity dynamics are directly influencing pricing and deal finalisation.

As per a mill representative, trade momentum in the Chennai market has notably softened in recent weeks, with finished steel demand sustaining at moderate levels. To align production with current market conditions, some mills have scaled back operations to around 70-80% capacity utilisation. Meanwhile, sponge iron prices remained relatively stable, although merchant market activity was subdued, with limited offers from suppliers.

Outlook

Market sources suggest that scrap prices are expected to remain range-bound, with a potential dip of around INR 500/t in the coming days. This trend is driven by the ongoing decline in semi-finished and finished steel prices, which is exerting downward pressure on scrap values.

Leave a Reply