- Improving economics to boost petcoke demand during H2FY’27

- Premium producers may favour US NAPP coal for its low sulphur content

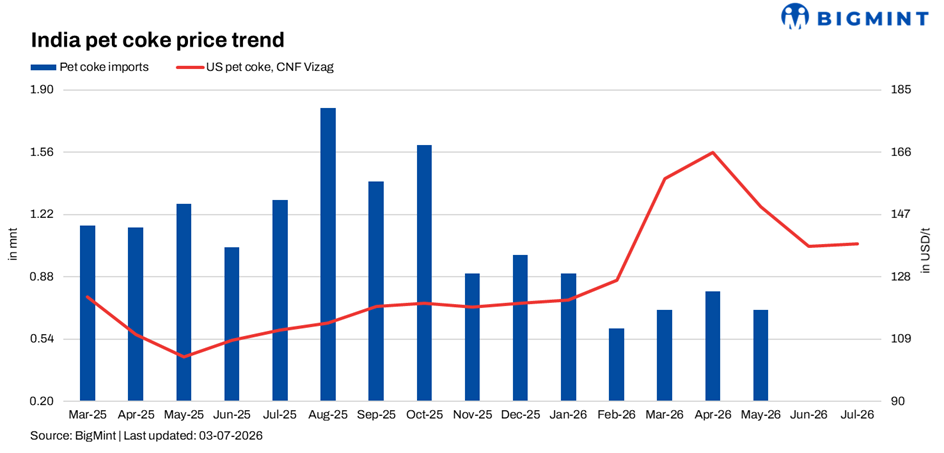

India’s imported fuel market serving the cement sector has entered a new phase following a sharp correction in international petroleum coke prices. After rallying to multi-year highs during May, petcoke prices have retreated by more than $20/t, restoring much of their cost advantage over imported thermal coal. The correction comes as India’s cement demand enters its seasonal monsoon slowdown, domestic coal availability remains comfortable, and cement producers increasingly focus on protecting margins.

While improving economics are expected to encourage greater petcoke consumption during the second half of FY’27, imported US high-CV coal continues to retain a strategic position. Premium cement manufacturers continue to value US Northern Appalachian (NAPP) coal for its low sulphur, stable combustion characteristics, and operational flexibility, while the retail market continues to absorb significant volumes despite subdued buying by large consumers.

With comfortable Coal India supplies limiting discretionary imports, the market is becoming increasingly selective, with buyers balancing fuel economics against operational performance.

Petcoke prices largely stable w-o-w but remain lower than May highs

Global fuel-grade petcoke prices remained largely stable during the latest assessment on 1 July 2026. FOB US Gulf Coast 4.5% sulphur remained unchanged w-o-w at $81/t, while 6.5% sulphur eased marginally by $0.5/t to $75/t. In Turkiye, CFR 6.5% sulphur prices declined by $1/t to $114.5/t, reflecting subdued buying interest.

In India, however, prices edged slightly higher. CFR India 6.5% sulphur increased by $0.5/t w-o-w to $135/t, while CFR west coast India 8.5% sulphur rose by $1/t to $135/t. Despite the marginal increase, delivered prices remained around $20-25/t below the highs recorded in May, significantly improving petcoke’s competitiveness against imported thermal coal.

The recent correction is expected to provide relief to Indian cement producers. According to industry channel checks, lower imported petcoke prices could reduce fuel costs by around INR 100/t of cement, with the benefit likely to be reflected from Q3 FY’27 as lower-cost cargoes replace earlier purchases.

Lower fuel costs arrive at opportune time for cement producers

The timing of the correction is significant. Industry demand remained healthy during June, growing in the high-single digits y-o-y, while pan-India cement prices remained broadly stable. However, with the onset of the southwest monsoon, construction activity has entered its seasonal slowdown, placing renewed pressure on producer margins.

Against this backdrop, lower imported petcoke prices are expected to partially offset rising input costs.

The cement industry is also witnessing a gradual shift towards sweating existing assets rather than aggressive capacity additions. As a result, fuel procurement strategies are increasingly focused on lowering operating costs while maintaining kiln efficiency.

US high-CV coal continues to occupy premium position

Despite petcoke’s improving competitiveness, imported US Northern Appalachian (NAPP) coal continues to command steady demand among premium cement manufacturers. US high-CV coal prices strengthened marginally during the latest assessment. FOB Baltimore 6,900 NAR increased by $0.45/t to $87.25/t, while FOB New Orleans 6,000 NAR also rose by $0.45/t to $86.50/t, supported by firm export fundamentals.

In contrast, India’s retail NAPP (ex-port) prices softened by around INR 500/t w-o-w to INR 13,900-14,000/t from INR 14,000-14,500/t. The correction reflected cautious monsoon-season buying and softer international sentiment. Despite the decline, current price levels remained attractive for consumers seeking high-calorific-value fuel, low sulphur emissions, and consistent kiln performance. Its excellent flame stability, easier kiln control, and superior blending flexibility continue to justify its use despite the recent narrowing of the price differential with petcoke.

Retail market continues to absorb significant volumes

India’s retail market for imported US high-CV coal remained resilient despite selective procurement by large cement producers. Weekly retail lifting increased to 103,893 t in the week ended 29 June from 93,088 t a week earlier and remained close to the 100,000 t mark throughout June, indicating steady demand from downstream industries.

Retail inventories at major western ports declined sharply to 206,196 t by 29 June from 406,155 t in the week ended 15 June, a drawdown of nearly 200,000 t within two weeks. The sustained decline reflected continuous movement of material into the domestic market despite slower fresh imports, highlighting healthy demand from smaller cement plants, lime producers, refractory manufacturers, brick kilns, and other industrial consumers purchasing through the domestic trading network.

Competition between petcoke and US coal intensifies

The sharp correction in petcoke prices has materially improved its competitiveness within the Indian cement sector.

For cost-conscious producers, imported petcoke once again offers a compelling economic proposition owing to its very high calorific value and improved landed economics. This is likely to encourage a gradual increase in petcoke consumption once lower-priced cargoes begin arriving during the September quarter.

However, US high-CV coal continues to occupy an important premium segment of the market. Many integrated cement producers continue to value its superior combustion characteristics, lower sulphur content and operational flexibility, particularly where kiln stability and product quality are critical.

Rather than completely substituting one fuel for another, many producers are expected to optimise their fuel mix by increasing petcoke’s share while retaining a proportion of premium US coal to maintain operational efficiency. The result is likely to be a more balanced fuel portfolio rather than a wholesale shift towards any single fuel.

Comfortable domestic coal continues to limit import demand

Despite the improving economics of imported fuels, Indian buyers remain in no hurry to build inventories.

Comfortable domestic coal availability, healthy stock levels, and the onset of the monsoon have significantly reduced spot procurement activity across the imported fuel market.

At the same time, broader Asian thermal coal markets continue to remain under pressure as both Chinese and Indian buyers adopt a wait-and-watch approach amid expectations of further price corrections. Improving Indonesian export availability and lower freight costs have also contributed to the softer sentiment.

Consequently, most cement producers are expected to continue purchasing selectively rather than aggressively rebuilding inventories.

Outlook

India’s imported fuel market is expected to remain comfortably supplied through the monsoon period, with domestic coal continuing to cap discretionary imports.

Petcoke appears well positioned to regain market share as the sharp decline in international prices begins flowing through to cement manufacturers’ fuel costs during Q3FY’27. The expected reduction of around INR 100/t in cement production costs should provide a meaningful cushion against seasonal margin pressures.

At the same time, US high-CV coal is expected to retain its premium position among quality-conscious consumers. Strong retail offtake and continued inventory drawdowns indicate that demand remains fundamentally healthy despite cautious buying by large cement producers.

Over the coming quarter, fuel procurement strategies are therefore expected to focus less on outright substitution and more on optimising fuel blends. Lower-priced petcoke is likely to capture incremental demand on economic grounds, while US NAPP coal should continue to command a premium among consumers seeking superior combustion performance and operational reliability.

Leave a Reply