- EBITDA per tonne increases by up to 40% y-o-y in Q1FY’26

- Strong housing, infra demand prompt strong capacity growth

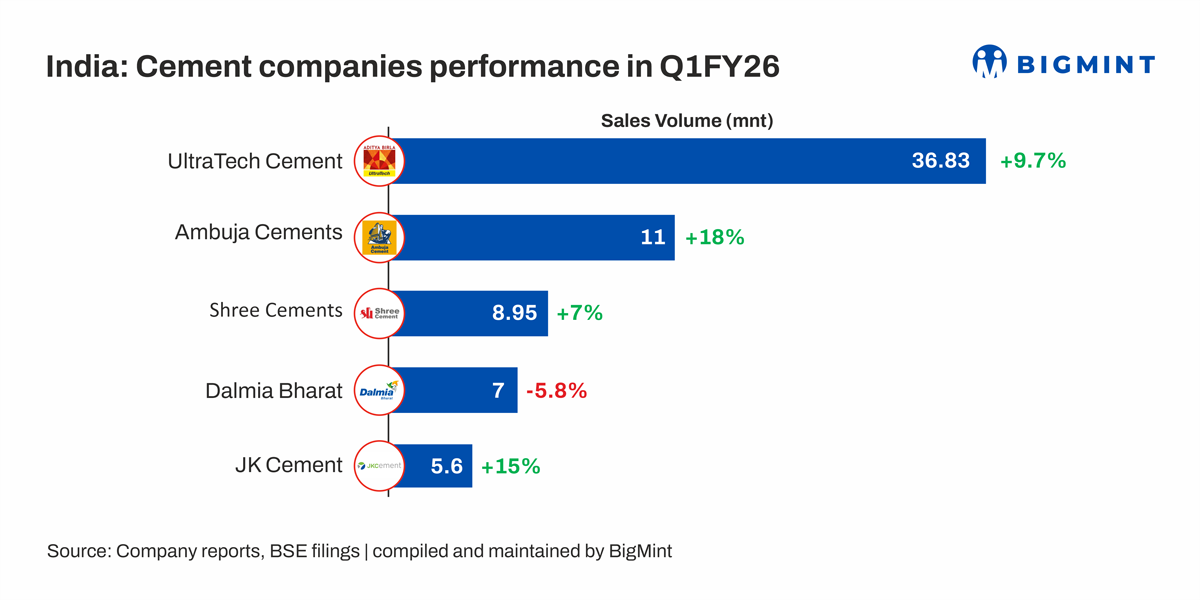

India’s leading cement companies reported mixed sales and financial performance in Q1FY’26, with strong y-o-y growth and q-o-q moderation due to seasonal pressures. UltraTech Cement’s sales volumes rose 10% y-o-y to 36.83 million tonnes (mnt), while Ambuja, Shree, and JK Cement saw y-o-y gains of up to 17% y-o-y in sales volumes and up to 40% in EBITDA per tonne. Only Dalmia Bharat witnessed a y-o-y decline in sales, while Shree Cement recorded a 1% dip in EBITDA per tonne.

Q-o-q, sales volumes declined by up to 10% due to the monsoon and high base effects. However, cost efficiencies, lower fuel expenses, and operational improvements kept margins supported.

Notably, companies continued expansion with new capacities, ready-mix concrete (RMC) plants, clinker and grinding units, and wall putty projects, positioning the sector to capture long-term demand from housing, infrastructure, and smart city developments.

Company-wise performance

1. Ultratech Cement’s consolidated sales volumes rose 9.7% y-o-y to 36.83 million tonnes (mnt) in Q1FY’26 from 31.95 mnt in Q1FY’25. On a q-o-q basis, volumes dropped 10% to 36.83 mnt in Q1FY’26 as compared with 41.02 mnt in Q4FY’25. Domestic grey cement sales were up 8.7% y-o-y at 34.64 mnt in Q1FY’26.

EBITDA per tonne improved to INR 1,248 ($14/t) in Q1FY’26, a 37% increase over INR 911 ($10/t) in Q1FY’25, whereas the same dropped 2% q-o-q from INR 1,270 ($14/t) in Q4FY’25. Cost efficiencies supported this y-o-y growth, with fuel costs at INR 871/t, power costs at INR 356/t, and logistics costs at INR 1,158/t.

The company expanded its cement capacity to 197.5 million tonnes per annum (mtpa) and is on track to reach 212.2 mtpa by FY’27. With housing and infrastructure demand expected to remain strong, the company is confident of sustaining growth and further improving margins.

2. Ambuja Cement delivered a strong operational performance in Q1FY’26. Standalone cement sales volumes reached 10.5 mnt, up 17% y-o-y from 9 mnt in Q1FY’25. However, compared to 11.6 mnt in Q4FY’25, the same declined by 9%.

The company posted a standalone EBITDA of INR 872, a 35% increase y-o-y, supported by higher volumes, better pricing, and improved operational efficiency. In Q1FY’26, EBITDA per tonne stood at INR 827, down 8% from INR 898 in Q4FY’25 but up by 16% from INR 714 in Q1FY’25.

Looking ahead, the company expects strong demand from housing, infrastructure, and smart city projects while continuing to focus on cost leadership and sustainability.

3. Shree Cement’s total sales volume rose 7% y-o-y to 8.95 mnt in Q1FY’26. In Q1FY’26, EBITDA per tonne edged down 1% y-o-y to INR 1,175.

3. Shree Cement’s total sales volume rose 7% y-o-y to 8.95 mnt in Q1FY’26. In Q1FY’26, EBITDA per tonne edged down 1% y-o-y to INR 1,175.

On the expansion front, the company is progressing as per schedule on its integrated cement unit projects in Jaitaran, Rajasthan (3.0 mtpa) and Kodla, Karnataka (3.0 mtpa). Once commissioned, the company’s cement production capacity will increase to 68.8 mtpa, moving closer to its long-term target of 80 mtpa by 2028.

The company is also expanding its RMC footprint, having increased its plant count from 15 at the start of FY’26 to 21 currently, with a goal of reaching 50 plants by year-end.

4. JK Cement’s total sales volumes rose 15% to around 4.98 mnt in Q1FY’26 as against 4.33 mnt in Q1FY’25, with growth led by the grey cement segment, while white cement volumes remained stable.

EBITDA per tonne increased 23% y-o-y to INR 1,247 in Q1FY’26 as against INR 1,014 in Q1FY’25 due to lower fuel costs, improved realisations, operational efficiencies and a trade mix of around 68% in Q1FY’26.

The company plans to set up a new wall putty unit with a capacity of 6 lakh mtpa near Nathdwara, Rajasthan, at a cost of INR 195 crore, targeted for commissioning by FY’27. The expansion is aimed at meeting rising demand, supported by an expected 9% CAGR growth in wall putty volumes, and will benefit from strong logistics connectivity and proximity to raw material sources.

5. Dalmia Bharat’s total cement sales volume stood at 7 mnt in Q1 FY26, down 5% y-o-y from 7.4 mnt in Q1FY’25 and lower by 19% q-o-q compared to 8.6 mnt in Q4FY’25.

The company delivered its highest-ever quarterly EBITDA of INR 883 crore, with EBITDA per tonne rising 40% y-o-y to INR 1,261 in Q1FY’26 from INR 901 in Q1FY’25. The same was up by 36% q-o-q from INR 926 in Q4FY’25. The company incurred capex of approximately INR 612 crore during Q1FY’26.

The company also announced an INR 3,287 crore investment to set up a 3.6 mtpa clinker unit and 6 mtpa grinding unit at Kadapa, Andhra Pradesh, along with a 3 mtpa bulk terminal at Chennai. Meanwhile, the 3.6 mtpa clinker expansion at Umrangso is in the advanced stage, and the 6 mtpa Belgaum-Pune project is progressing as planned. Fuel consumption cost declined from $106/t in Q1FY’25 to $100/t in Q1FY’26, whereas raw material costs increased.

Note: Sales volumes and EBITDA per tonne figures have been rounded off in this article.

Leave a Reply