- High petcoke prices push Indian buyers toward cheaper coal alternatives

- Over 2.5 mnt US coal en route signals strong fuel switching

The Indian petroleum coke market is facing a double shock of tightening supply and weakening demand, as cement manufacturers and industrial buyers shift toward thermal coal. Vessel manifest data highlights the scale of this transition, indicating that the shift is already underway rather than anticipated.

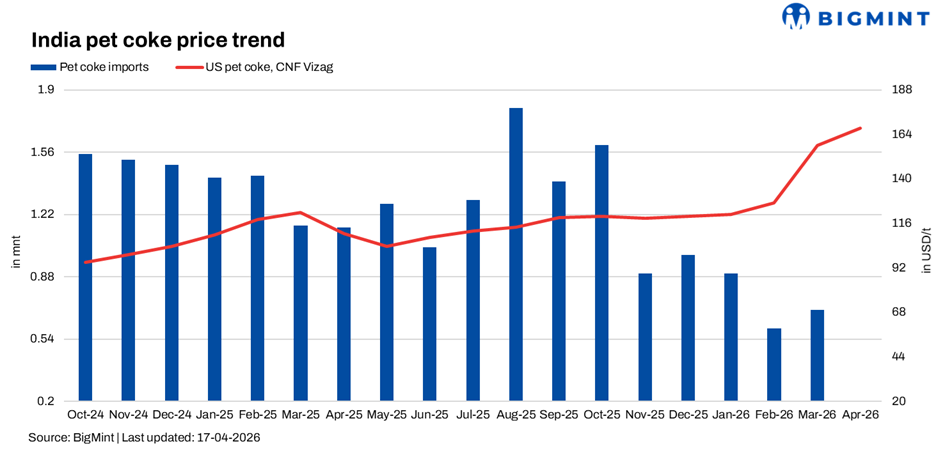

Market conditions reflect a widening bid-offer gap, with offers for US-origin 6.5% sulphur petcoke on a delivered India basis holding at $168-170/t, while bids remain closer to $155/t. This divergence has effectively stalled trade, with prices moving ahead of executable demand and rendering the market illiquid.

Coal inflows displace petcoke demand

The primary demand-side shift is now visible in physical flows. Over 2.5 mnt of US coal is currently en route to India across more than two dozen vessels, with arrivals scheduled between April and May 2026. This reflects a deliberate build-up of coal inventories by cement manufacturers and industrial buyers.

The retail segment has secured over 1.1 mnt of these volumes, while industrial consumers, including major cement manufacturers, account for more than 1.4 mnt. The scale and coordination of these purchases indicate active substitution rather than opportunistic buying.

Supply disruptions fail to translate into demand support

This shift toward coal is occurring despite tightening petcoke supply. US Gulf Coast 6.5% sulphur petcoke is assessed at around $103/t FOB, with delivered India cargoes near $158/t CFR, indicating firm global pricing.

However, supply-side disruptions have intensified. Ongoing hostilities have reduced Middle Eastern availability, with key refining complexes impacted. A fire at a major Gulf Coast refinery has delayed shipments from April to May, while a fire at a new Mexican refinery has raised concerns over potential damage to its coking unit. These disruptions, combined with an estimated reduction of over 5 million barrels per day in refining capacity, have tightened supply.

Despite this, cement manufacturers and industrial buyers have not responded with increased offtake, as elevated prices continue to deter purchases.

Buyers shift toward coal and inventory drawdown

Cement manufacturers and industrial buyers are actively executing a shift away from petcoke. Vessel data confirms significant coal procurement across both retail and industrial segments, with deliveries scheduled over the coming weeks. In parallel, some cement plants are reported to have reduced or eliminated petcoke usage, opting instead for coal and existing inventories.

The absence of transactions reflects both the wide bid-offer gap and expectations among buyers that prices will correct before re-entry. Additional supply remains in the pipeline, with multiple vessels scheduled for loading from the US East Coast through late April, further reinforcing the shift in fuel sourcing.

Outlook

The near-term outlook remains defined by limited trade activity, with prices expected to remain within the $155-170/t CNF India range.

Geopolitical developments have introduced uncertainty, with a recent ceasefire prompting a wait-and-watch approach. While risk premiums may ease, damage to Middle Eastern infrastructure could constrain supply for an extended period.

At the same time, incoming coal volumes are expected to ensure adequate stock levels for cement manufacturers and industrial buyers, reducing any urgency to return to petcoke. Unless prices correct toward the mid-$150s or lower, these buyers are likely to continue operating on coal and existing inventories.

The vessel data indicates that cement manufacturers and industrial buyers are not waiting for price adjustments. Instead, they are actively rebalancing their fuel mix toward coal. If sustained, this shift could alter India’s role in the global petcoke market, from a source of demand support to a limiting factor on prices.

Summary of Key Indian Market Indicators (April 2026):

The market remains inactive, with trading constrained by pricing misalignment. The coming weeks will determine whether supply-side disruptions force cement manufacturers and industrial buyers to return, or whether the current shift toward coal represents a more durable change in fuel strategy.

Leave a Reply