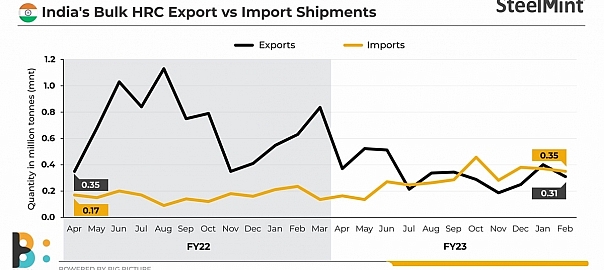

India’s bulk HRC exports touched 3.72 million tonnes (mnt) over April 2022-February 2023, as per data maintained with SteelMint, dropping 50% against 7.50 mnt recorded over April 2021-February 2022.

Country-wise shipments

Vietnam stood as the largest importer at 0.86 mnt (1.43 mnt) but volumes fell 40% in the period under review. Italy followed with 0.78 mnt (1.22 mnt), down 36% y-o-y. The UAE showed a 45% drop at 0.5 mnt (0.92 mnt). Turkiye showed a 61% decline at 0.34 (0.87 mnt) while Belgium’s imports showed the steepest plunge of 67% to 0.27 mnt (0.83 mnt).

Notably, HRC/plates accounted for the highest share of 65% in India’s total steel exports of 5.90 mnt in the 11-month period under review.

Factors that dragged down bulk HRC exports

Export duty impact: Imposition of the 15% export duty in May 2022, gave a jolt to Indian steel exports, where the bulk of the share belongs to flat steel. For instance, the share of flats in the entire steel exports basket in calendar 2021 was almost 60% and 70% in 2022.

HRC volumes, which had started rising with the onset of the Russia-Ukraine war, touching 0.63 mnt in February 2022 and 0.84 mnt in March, tapered off from July 2022 at 0.21 mnt, down 58% against 0.51 mnt in June. This trend persisted till December 2022. The average monthly volumes over April-February, 2022-23 were 0.37 mnt against 0.68 mnt in the same months in the previous fiscal. Around 0.51 mnt exported in June 2022 were shipments of previous bookings.

However, exports started picking up from January 2023 with removal of the duty in November 2022.

EU market became subdued: A large volume of India’s bulk HRCs were being exported to the European Union since Covid struck in 2020. However, after panic buying in March 2022, the Continent became silent amid high energy and gas prices, inflation and subdued demand.

Exports to Italy, Belgium. Spain and the UK decreased 36%, 67%, 69% and 34% respectively in the period under review.

Turkiye, which sold value-added HRCs to the EU, also lowered buying amid the same factors challenging the EU with imports dropping 61% y-o-y.

Southeast Asia demand drops: Eventually Indian mills concentrated on Middle East and South East Asia markets like Vietnam but overall domestic demand for finished steel in the latter also dropped because of Covid resurgence and slow infra development.

Imports

India’s bulk HRC imports over April-February rose a whopping 75% to 3.20 mnt against 1.83 mnt in the same period in the previous fiscal.

Imports arrived much to the concern of Indian mills mainly from South Korea and Vietnam.

If imports averaged 0.17 mnt in April-February 2021-22, these touched 0.29 mnt in the same period in FY23.

In October 2022, imports hit a high of 0.46 mnt, the same month in which trade-level HRCs ruled at around INR 56,800/t ($692/t) but landed prices from FTA countries were at a little above $600/t (around INR 50,000-51,000/t in rupee parity). Imported landed prices remained higher than Indian domestic HRC offers persistently over August-November, 2022. End-users were encouraged to import due to price viability.

Outlook

The rise in Chinese steel spot and futures prices, higher realisations from Europe and limited export allocations could fetch higher prices for Indian mills and sustain the HRC exports momentum.

Leave a Reply