- Chinese Lunar holiday likely to slow export trade

- Domestic scrap shortages fail to support prices

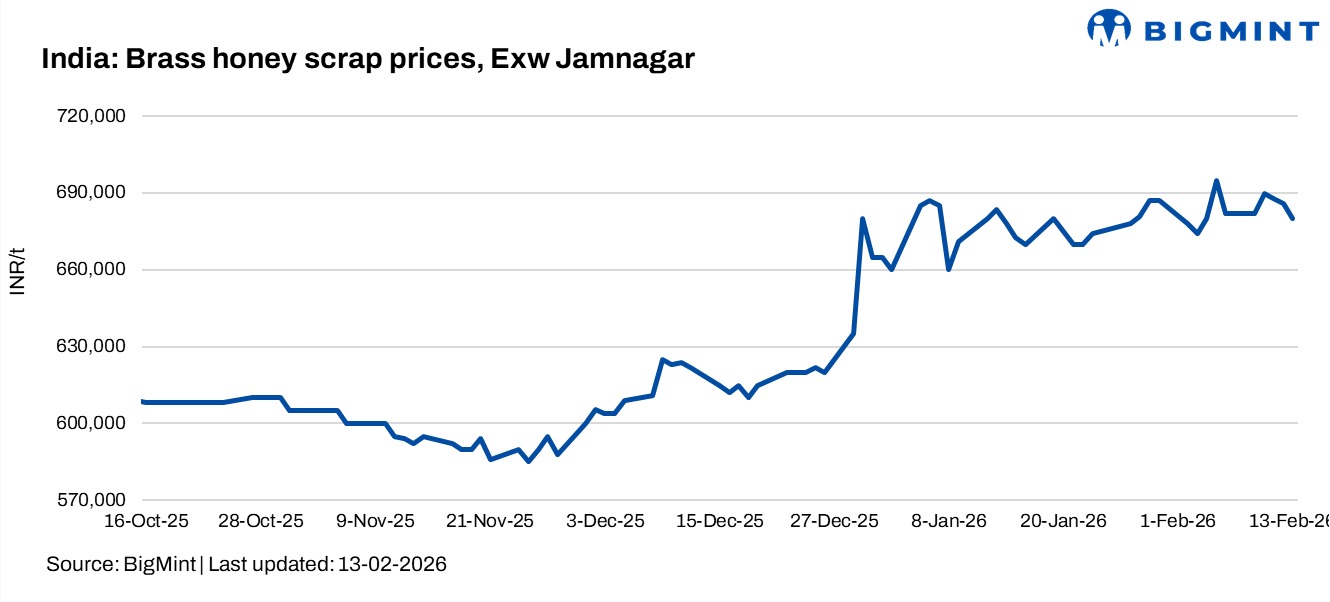

Domestic brass honey scrap prices moved lower w-o-w. BigMint assessed brass honey, exw Jamnagar, Gujarat, at INR 680,000/tonne (t) on 13 February, down INR 15,000/t from INR 695,000/t a week ago.Market participants indicated that brass honey scrap prices edged higher during the first week of February, assessed at INR 695-900/kg ex-Jamnagar, as new trades actively took place after the slowdown in January due to the start of the new year. Moreover, record-high London Metal Exchange (LME) prices urged market participants to sell material immediately.

However, scrap prices fell this week, as major export markets such as China are all set to remain inactive for the Lunar New Year holidays. In the domestic market, while material was sold out, subdued export sentiment pulled down prices. Rising copper price volatility also made secondary producers more cautious.

Market insights

On the export side, brass honey ingots are currently being quoted at 50% of LME on an FOB basis, with trades also discussed on a CIF China basis.

Trade activity is expected to slow further as China heads into the Lunar New Year holidays next week. Export inquiries have started thinning, and market participants expect muted transactions during the festive period. Overall sentiment remains cautious, with participants closely monitoring post-holiday demand signals and inventory restocking trends across global markets.

Market participants anticipate subdued trade volumes this month, with clearer direction likely only after holiday-related inventory adjustments and fresh import inquiries resume.

In India, ongoing brass scrap shortages pushed material into a premium as well, with deals being concluded above prevailing market benchmarks. Supply tightness continues to influence pricing sentiment overall.

Many brass manufacturers in Jamnagar and nearby clusters purchased only against confirmed orders.

Domestic indications stood around INR 680,000/t at today’s levels on an ex-Jamnagar basis. However, bid-offer disparities remained wide, as buyers continued to seek discounts amid cautious procurement strategies. Payment delays and liquidity concerns in the domestic market added pressure, limiting aggressive buying interest across major consuming regions.

Outlook

Overall sentiment in India is steady but not aggressive. While supply tightness can support prices, weak demand from small casting units and exporters and liquidity constraints will cap upside momentum. Market participants expect trade to remain moderately weak, with better clarity likely after export demand from China normalises post-holidays.

Leave a Reply