- Freight strengthens amid carrier rate hikes and capacity constraints

- Persistent bid-offer gap keeps India’s scrap imports under pressure

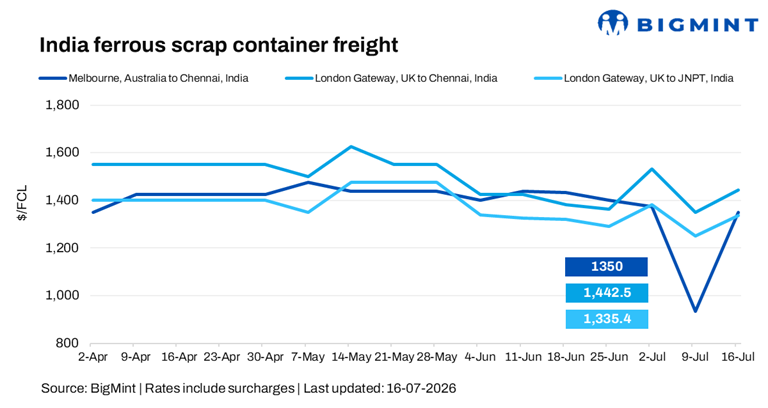

India-bound ferrous scrap container freight rates strengthened in the week ended 16 July amid carrier actions and tight capacity. However, a wide bid-offer gap, poor import economics, and renewed geopolitical tensions continued to weigh on buying interest, keeping container bookings subdued.

A shipbroker informed, “Although freight rates have risen amid container shortages, rates remain negotiable on a case-by-case basis, particularly for shippers with consistent cargo volumes or strong carrier relationships, allowing them to secure more competitive pricing.”

Another shipbroker stated, “Shipping lines continue to quote varied freight rates, while space remains tight across several carriers. Meanwhile, weak ferrous scrap import demand in India continues to weigh on buying activity, limiting overall market momentum.”

“Freight rates have increased significantly over the past week, driven by carrier rate adjustments and tight vessel capacity. The quoted rates reflect prevailing market levels for budgeting purposes and are inclusive of all applicable surcharges, including the General Rate Increase (GRI), Peak Season Surcharge (PSS), and Low Sulphur Surcharge (LSS), a source mentioned.

An Australia-based shipbroker said, “Despite lower scrap prices, Australian traders remain active in the export market, with several cargoes being booked at loss-making levels.”

Meanwhile, UK container freight sentiment remained firm as exporters maintained higher offer levels amid elevated freight costs. Shipments increasingly shifted towards other South Asian markets on stronger buying interest, while India-bound trade remained subdued due to weak demand.

Route-wise update

Market highlights

- CFI drop w-o-w amid easing front-loading and improving vessel supply: The Container Freight Index (CFI) decreased by 142.05 points w-o-w to 3,184.82 points on 10 July 2026, down from 3,326.87 points on 3 July. The decline reflects a modest correction following the recent sharp rally, driven by easing front-loading demand and improved vessel availability.

- Bunker prices rise w-o-w: Bunker prices stood at $768/tonne (t) on 16 July, a w-o-w increase of $102/t against $666/t, supported by higher crude oil prices amid renewed geopolitical tensions in the Middle East, along with stronger refining margins and increased demand for marine fuels. The increase added to operating costs for shipowners, keeping freight sentiment firm.

Outlook

India-bound ferrous scrap freight rates are expected to remain firm in the near term, supported by tight container availability, carrier capacity management, and elevated bunker costs. However, freight movements will continue to depend on shipping line pricing strategies and space availability across key trade lanes.

On the demand side, India’s scrap imports are likely to remain subdued as a persistent bid-offer gap and weak import viability keep buyers cautious. Unless import economics improve or finished steel demand strengthens, booking activity is expected to remain limited despite firm freight rates.

Leave a Reply