- Bid-offer disparity persist in Europe-India route

- Australian scrap export to India fall amid weak buying interest

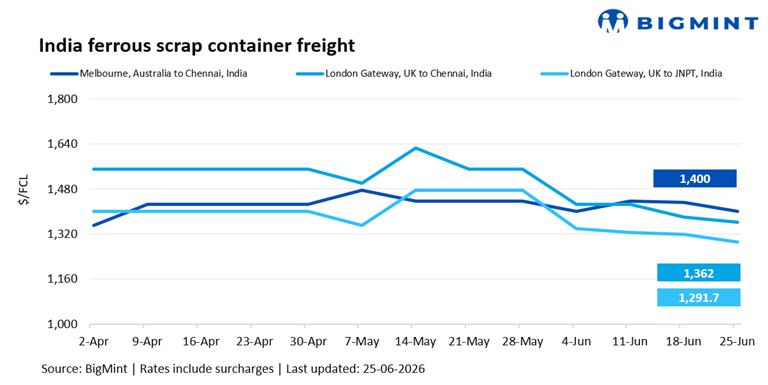

India-bound ferrous scrap container freight rates remained under pressure in the week ended 25 June across major regions. Import sentiment stayed weak as mills largely stayed on the sidelines amid unviable offers and subdued finished steel demand.

Buyers continued to seek lower prices, while limited trading activity and expectations of softer freight rates kept procurement cautious.

“The UK-JNPT corridor typically commands lower freight than the UK-Chennai route, making the current spread commercially reasonable. That said, further negotiation may be possible depending on carrier selection, shipment size, and contractual terms such as free time”, a source said BigMint.

Meanwhile, UK scrap export sentiment remained weak across South Asia amid cautious buying, subdued steel demand, and expectations of further price corrections, keeping trading activity limited due to a persistent bid-offer gap on the UK-India route.

Similarly, the Australia-India scrap export market continued to face sluggish conditions, with negligible activity reflecting weak demand and a lack of spot transactions.

Route-wise update

Market highlights

- CFI remain supportive amid geopolitical risks: CFI rose by 136.47 points w-o-w to 3,121.69 points on 18 June from 2,985.22 points on 12 June, supported by robust pre-peak season cargo demand, front-loading ahead of tariff changes, tight vessel capacity, and continued carrier capacity management, which sustained upward pressure on spot rates across key east-west trade lanes.

- Bunker prices firm w-o-w: Bunker prices stood at $684/tonne (t) on 25 June, an increase of $26/t w-o-w. Bunker sentiment turned firmer during the week as crude oil prices rebounded amid renewed geopolitical uncertainty in the Middle East and expectations of tighter near-term fuel supply. However, easing tensions in the region and improved shipping conditions continued to limit sharper gains, keeping market participants cautious.

Outlook

Near-term scrap vessel freight outlook remains cautiously firm. While current rates are under pressure due to weak mill demand and a wide bid-offer gap, seasonal buying and gradual restocking could support activity. Tighter vessel availability on select routes may also provide some support.

However, gains are likely to be limited by subdued steel demand and price-sensitive buyers. A sustained recovery will depend on improved scrap import demand and stronger fixture activity across key routes like UK-India and Australia-India.

Leave a Reply