- Australian cargo flow and rising bunker costs support Panamax routes

- South East Asian activity lifts Supramax despite subdued Indonesian demand

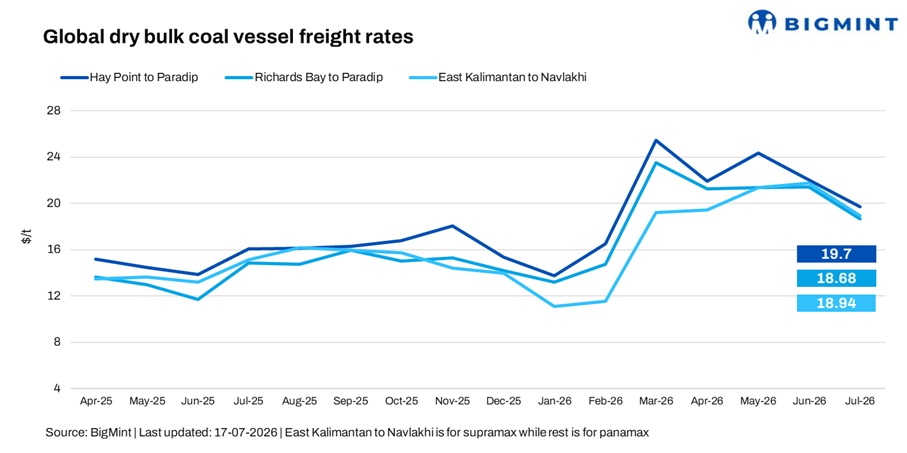

India’s dry bulk coal freight market maintained a firm undertone in the week ended 17 July 2026, with freight rates moving higher across both Panamax and Supramax segments. Active Australian coal fixtures, stronger South East Asian cargo activity and sharply higher bunker prices supported owners’ pricing, while limited prompt tonnage provided additional support across key routes.

The Panamax market remained resilient despite mixed regional fundamentals. Firm Australian cargoes and healthy South East Asian activity underpinned sentiment, although ample Pacific vessel supply continued to limit stronger gains.

A shipbroker told BigMint, “The freight market is moving sideways, with no clear bullish or bearish triggers. Cargo flow remains steady, but we are awaiting fresh enquiries before taking aggressive positions.”

The Supramax segment also strengthened during the week, supported by fresh South East Asian enquiries and firmer Indonesia round voyages. Rising bunker prices and monsoon-related operational delays further supported freight levels by keeping vessel operating costs elevated.

Another shipbroker said, “Freight rates are likely to maintain a firm-to-higher trend over the coming weeks. The ongoing monsoon is slowing vessel operations at some ports, while higher oil prices are pushing up bunker costs, both of which could lend further support to freight levels if cargo demand remains steady.”

Buying interest on the South Africa-India route remained subdued during the week. A trader told BigMint, “Demand for South African coal into India is still on the weaker side, so fresh fixtures are limited. Unless buying picks up, freight on the route is unlikely to move much higher.”

Overall, the dry bulk market presented a mixed picture during the week. While the Baltic Dry Index eased on weaker Capesize earnings, Panamax and Supramax remained comparatively firm, supported by stronger South East Asian activity and rising voyage operating costs.

Route-wise update

Market highlights

- Baltic Dry Index (BDI) drops w-o-w: The BDI fell 2.4% (70 points) w-o-w to 2,840 as of 16 July, from 2,910 a week earlier, as weaker Capesize earnings weighed on the broader dry bulk market. The Panamax Index edged up 0.2% (4 points) to 2,257, supported by firm Atlantic demand and stronger South East Asian activity, though ample vessel supply capped further gains. Meanwhile, the Supramax Index rose 1.8% (30 points) to 1,730, driven by stronger South East Asian cargo activity and firmer North Pacific and Australian round-voyage earnings.

- Brent crude futures rise w-o-w: Brent crude oil (September 2026 contract) climbed to $85.98/barrel (bbl) as of 17 July, up $9.33/bbl w-o-w from $76.65/bbl a week earlier. The increase was driven by rising geopolitical tensions, supply-side concerns, and stronger buying sentiment amid uncertainty over global crude availability.

- Bunker prices rise sharply w-o-w: Singapore’s Very Low Sulphur Fuel Oil (VLSFO) bunker prices increased by $112/tonne (t) w-o-w to $764/t as of 17 July, compared with $652/t a week earlier. The sharp increase tracked stronger Brent crude prices and heightened geopolitical tensions, pushing up voyage operating costs for shipowners.

- DCE coke futures decline w-o-w: Coke futures on the Dalian Commodity Exchange for the September 2026 contract fell to RMB 1,864/t ($275.20/t) as of 17 July, compared with RMB 1,913/t ($281.62/t) a week earlier. The decline reflected weaker market sentiment amid subdued steel demand, soft coke fundamentals, and continued uncertainty surrounding China’s steel production outlook.

Outlook

India-bound coal freight is expected to remain firm to range-bound in the near term. Higher bunker costs, monsoon-related delays and steady Australian and South East Asian cargo activity are likely to support freight levels, while fresh cargo enquiries will remain crucial for sustaining momentum. However, subdued South Africa–India coal demand may continue to cap gains on the route.

Leave a Reply