- Sponge iron prices increase by INR 1,670/t w-o-w

- Semis, finished steel prices improves by INR 1,580-1,850/t

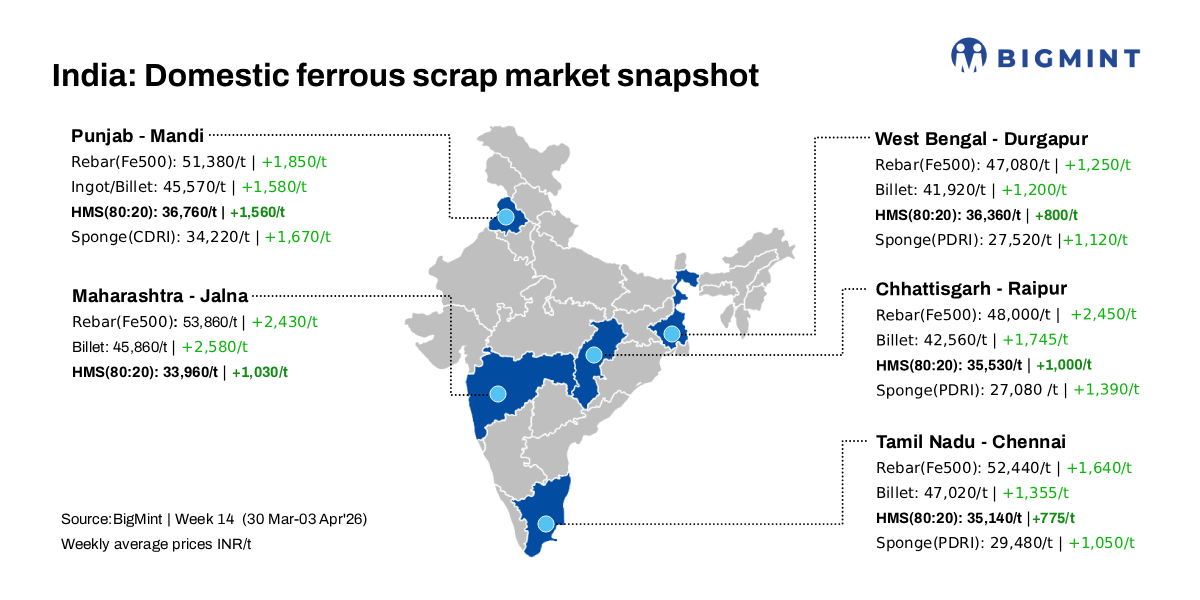

BigMint’s domestic end-cutting scrap index, tracking the Mandi Gobindgarh market, improved by INR 200/tonne (t) d-o-d to INR 40,000/t DAP on 03 April. On a weekly basis, prices surged by INR 1,560-1,760/t, supported by tightening scrap availability and improved demand across semi-finished and finished steel segments.

Scrap inflows into Mandi Gobindgarh remained restricted, as suppliers held back material anticipating further price gains. Concurrently, disruptions in imported scrap arrivals-particularly from the Middle East amid geopolitical tensions-have exacerbated shortages across northern India. HMS suppliers capitalised on limited availability, commanding premiums and pushing regional prices higher. Additionally, the ongoing gas crisis has altered raw material preferences, further supporting scrap demand.

A mill owner informed ” That rising oil and gas prices are expected to elevate production costs across the steel value chain, reinforcing upward pressure on finished steel prices.”

Raw materials and steel segment trends

Sponge iron prices in Mandi declined marginally by INR 100/t d-o-d to INR 34,500/t, although they rose INR 1,670/t w-o-w amid improved demand. Pig iron prices in Ludhiana fell by INR 500/t d-o-d but recorded a sharp weekly increase of INR 2,820/t.

In the steel segment, ingot prices in Mandi increased by INR 100/t d-o-d to INR 46,000/t, up INR 1,580/t w-o-w. Rebar prices remained steady at INR 51,900/t, registering a weekly gain of INR 1,850/t, while HR strip prices softened marginally by INR 100/t d-o-d to INR 47,000/t but surged INR 2,525/t over the week.

Overview of Alang market

On 3 April, 2026, Gujarat’s Alang ship-breaking melting scrap prices dropped INR 200/t d-o-d, with BigMint pegging HMS (80:20) at INR 37,300/t ($403/t) ex-yard; semi-finished steel eased INR 100-200/t on subdued prior trade, as Bhavnagar IF mills’ average demand led suppliers to cut offers, while a local ship breaker highlighted a 40% drop in activity due to the ongoing gas crisis.

Upcoming scrap auctions

Price highlights

End-cutting to billet spread: In Mandi, the spread between end-cutting scrap and billets stood in the range of INR 5,900-6,300/t.

Domestic vs imported scrap: Imported melting scrap prices at Nhava Sheva Port were assessed at $380/t-385/t, approximately INR 37,782/t (inclusive of freight). HMS (80:20) prices in Mumbai remained stable d-o-d at INR 35,700/t DAP. Indicative prices of shredded from Europe stood at $400/t-$405/t CFR Nhava Sheva.

Raipur sponge iron-billet spread: The conversion spread (margin) between pellet-based DRI (P-DRI) and steel billets in Raipur stood at INR 15,700/t.

Leave a Reply