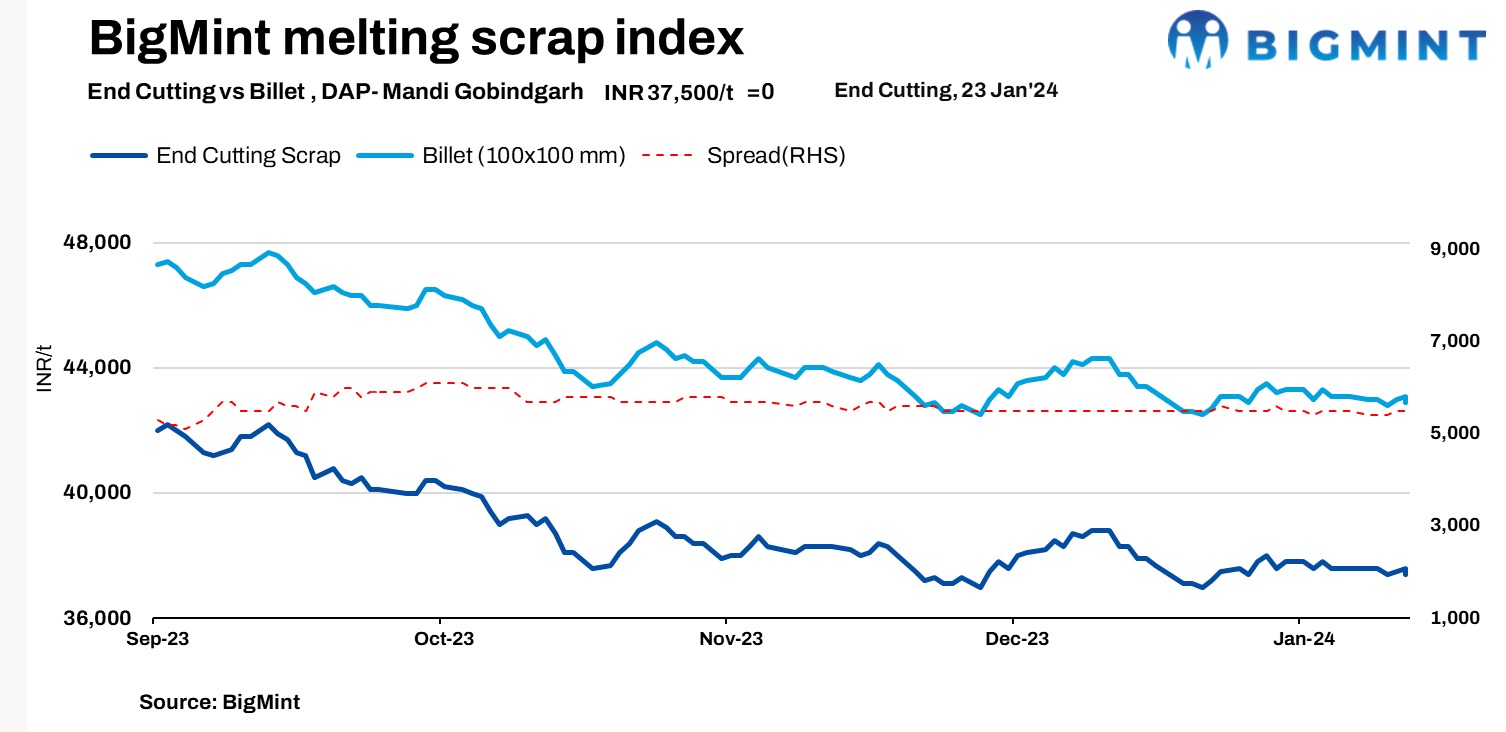

On 23 January, 2024, BigMint’s domestic steel scrap (end-cutting) index remained unchanged d-o-d, reaching INR 37,500/t on a delivered-at-plant (DAP) basis in Mandi Gobindgarh.

In the region, the semi-finished and finished steel markets experienced subdued conditions due to limited demand. The supply of scrap is currently constrained, leading mills to incorporate sponge iron into their charge mix. This adjustment is a response to the higher costs associated with imported scrap and a slightly slower supply of domestic scrap, as noted by a mill owner.

Semis’ market

Steel ingot prices in Mandi remained stable d-o-d at INR 42,900/t at the time of reporting and price normalisation. Meanwhile, prices of steel ingot in other key markets remained constant. The current market scenario indicated a lack of significant improvement in trade activity today, as buyers have chosen to remain silent in both the first and second halves of the trading session.

Raw materials price update

In Mandi, the prices for sponge iron (CDRI) experienced a decrease of INR 100/t, settling at INR 31,400/t. Concurrently, pig iron (steel grade) prices also saw a decline of INR 100/t, reaching INR 39,600/t DAP.

Snapshots of other markets

The stability continued in ship-breaking melting scrap prices in Alang, Gujarat, with no d-o-d change reported on 23 January, 2024. According to SteelMint’s analysis, HMS (80:20) prices were maintained at INR 34,100/t ex-yard. In the region’s trading session yesterday, semi-finished steel prices remained steady. Scrap suppliers chose to uphold firm offers today, given the presence of moderate buying inquiries at the existing price level.

In the Raipur steel market, there was a noticeable weakness in demand for both semi-finished and finished steel, contributing to a continuous decline in prices within the region. The market is experiencing minimal trade activity in steel scrap due to limited buyer participation, resulting in a substantial drop of around 200/t d-o-d in scrap prices.

Price highlights

End-cutting and billets spread: In Mandi, the end-cutting scrap and billets spread was at INR 5,000-5,500/t.

Domestic Vs imported scrap: Imported melting scrap prices at Nhava Sheva Port were at around $394-$397/t, which equates to approximately INR 35,210/t(including freight),while local scrap-HMS (80:20)-prices in Mumbai stood at INR 33,000/t stable d-o-d.

In India, the interest in purchasing imported scrap remained subdued due to a substantial price gap between offers and bids. Furthermore, the presence of more affordable alternatives in the domestic market, such as domestic scrap and sponge iron, have led buyers to adopt a cautious stance.

Shredded scrap offers from Europe were observed at approximately $410-$415/t CFR Nhava Sheva.

A steel mill official stated, “We have sufficient inventories until March, with a focus on domestic procurement. Additionally, we are opting for sponge iron in the charge mix for its cost-effectiveness. Consequently, there is currently no interest in booking imported scrap.”

Raipur sponge iron-billet spread: The current conversion spread (margin) from pellet-based DRI (P-DRI) to steel billets in Raipur stood at INR 13,200/t.

To see SteelMint’s melting scrap assessment, pricing methodology and specification documents, Click here

To provide feedback on this index or if you would like to contribute by becoming a data partner, please contact – info@steelmint.com.