- Mixed trends prevail in raw materials

- Finished steel demand improves slightly

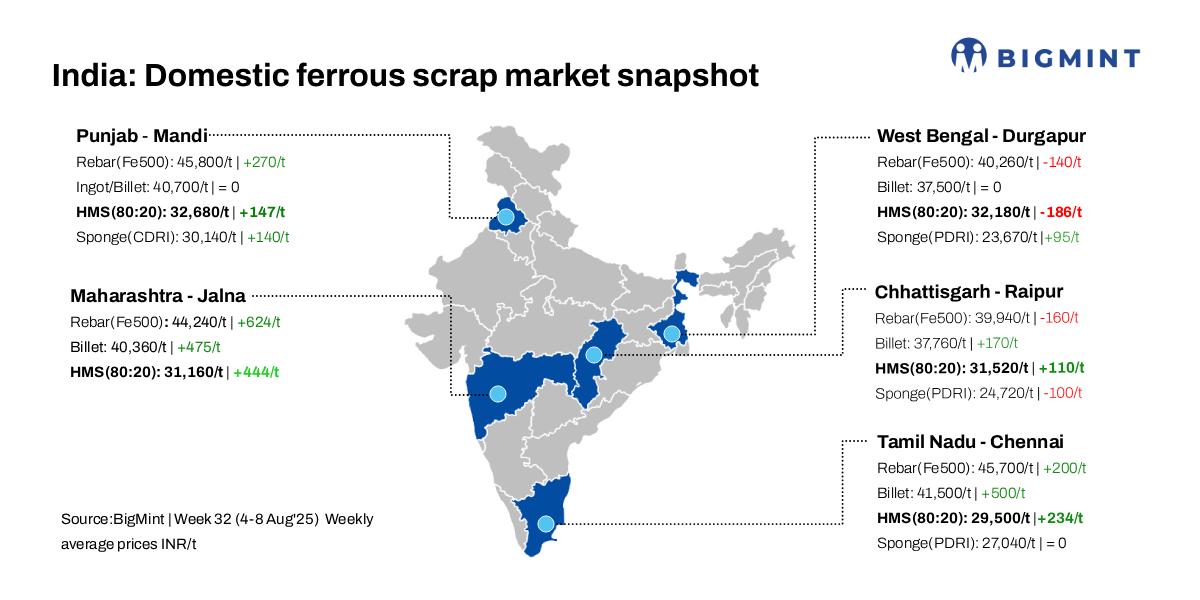

BigMint’s domestic end-cutting scrap index, tracking the Mandi Gobindgarh market, remained stable d-o-d at INR 35,600/t DAP on 8 August 2025. Scrap prices in the Indian market saw a modest rise of INR 100-165/t on a weekly basis, supported by steady but moderate demand from the secondary steel sector.

In Mandi Gobindgarh, a key hub for secondary steel production, market participants are hopeful of a further uptick in scrap prices in the coming week. Sentiment is being buoyed by slight improvements in the finished steel market compared to the previous week, signaling potential for a gradual recovery in pricing momentum.

While overall buying activity remains cautious, the consistent demand has helped maintain price stability in the scrap segment.

About Imported scrap market

The imported steel scrap market remains largely unviable for Indian buyers, with trading activity staying muted due to high import costs and a persistent gap between bids and offers.

A Mandi steel maker informed “Currently, imported scrap offers stand at around $365/t for shredded scrap from Europe, while HMS 1 from Bahrain is being quoted at an indicative $345/tonne CFR West Coast India. However, these prices remain unappealing to most Indian mills given local availability and cost considerations.”

Raw material prices

Sponge iron (CDRI) prices in Mandi Gobindgarh extended their downward trend for the third consecutive day, dropping by another INR 100/t today. The material is currently assessed at INR 29,900/t DAP. Despite the recent dip, sponge iron prices have increased by INR 140/t on a weekly basis, reflecting earlier market strength.

In contrast, pig iron prices in Ludhiana (Punjab) have remained stable for the fourth straight day, assessed at INR 35,800/t DAP. However, on a w-o-w basis, pig iron prices have declined by INR 230/t, largely due to weak buying sentiments in the market.

Steel market trends

The semi-finished steel market in Mandi Gobindgarh remained steady d-o-d, settling at INR 40,500/t DAP.Ingot prices in the region recorded a marginal week-on-week increase of INR 67/t. On a daily basis, prices across key steel market hubs witnessed a decline of INR 100-200/tonne. However, some regions reported stable pricing, indicating a mixed market trend.

Rebar (Fe 500) prices in the finished steel market saw a slight decline of INR 100/t day-on-day, now at INR 45,600/t ex-works. However, on a weekly basis, prices reflect an overall gain of INR 267/t. This rise is attributed to a pickup in trade activity and active bookings observed during the mid-week, offering some support to market sentiment despite generally moderate demand.

Overview of Durgapur market

Billet offers in the Durgapur market held steady at INR 37,300/t, while rebar saw a minor correction of INR 100/t, settling at INR 39,800/t. HMS 80:20 scrap declined further by INR 200/t to INR 32,000/t. Overall trade remained moderate during today’s session. Despite firm offers for pig iron and scrap from sellers, buyers submitted lower bids, reflecting cautious sentiment driven by only average demand in finished steel.

Upcoming scrap auctions

Price highlights

End-cutting-billets spread: In Mandi, the end-cutting scrap and billet spread stood at INR 4,800-5,200/t.

Domestic vs imported scrap: Imported melting scrap prices at Nhava Sheva Port were at $335/t, which equates to approximately INR 31,537/t (including freight). HMS (80:20) prices in Mumbai remained stable at INR 31,300/t DAP today. Indicative prices of shredded from Europe stood at $365/t CFR Nhava Sheva.

Raipur sponge iron-billet spread: The conversion spread (margin) between pellet-based DRI (P-DRI) and steel billets in Raipur stood at INR 13,100/t.

To check BigMint’s melting scrap assessment, pricing methodology, and specification documents, click here.

Leave a Reply