- Sponge iron prices decrease by INR 390/t w-o-w

- Semis, finished steel prices dip by INR 360-580/t

BigMint’s domestic end-cutting scrap index, tracking the Mandi Gobindgarh market, declined by INR 200/tonne (t) d-o-d to INR 35,100/t DAP on 12 December 2025.However, the index decreased by INR 400/t w-o-w as steel prices continued to edge down.

Scrap prices in Mandi Gobindgarh declined by around INR 400/t-500/t on a weekly basis, tracking a muted buying trend throughout the week. Weak demand for finished steel further dampened scrap procurement by mills, as they continued to grapple with substantial inventory pressure in both semi-finished and finished steel.

Mandi Gobindgarh, a key secondary steel hub, once again saw scrap prices slip to a three-week low, underscoring the persistent softness in market sentiment. The ongoing squeeze on conversion margins from semis to finished steel is adding to the pressure on local steelmakers, limiting their appetite for fresh scrap bookings and keeping overall trading activity subdued.

Alternative raw material prices

Sponge iron (CDRI) prices in Mandi dropped by INR 200/t d-o-d to INR 28,400/t (DAP). On a w-o-w basis, prices declined by around INR 390/t.

Similarly, steel-grade pig iron prices in Ludhiana remained stable d-o-d at INR 34,800/t (DAP) but w-o-w prices dipped by INR 160/t.

Steel market

Semi-finished steel (ingot/billet) prices in Mandi Gobindgarh slipped by INR 200/t d-o-d to INR 39,800/t (DAP), weighed down by weak demand and narrowing conversion margins. Ingot prices across key production centres also softened further by INR 200–500/t d-o-d, while in Mandi ingot prices declined by INR 580/t w-o-w.

Rebar (Fe 500) prices in Mandi edged down by INR 200/t d-o-d to INR 44,600/t ex-works, marking a fall of around INR 360/t w-o-w.

Meanwhile, HR strip prices fell by INR 200/t d-o-d to INR 40,300/t ex-works, with weekly prices down by INR 630/t.

Peek into eastern India

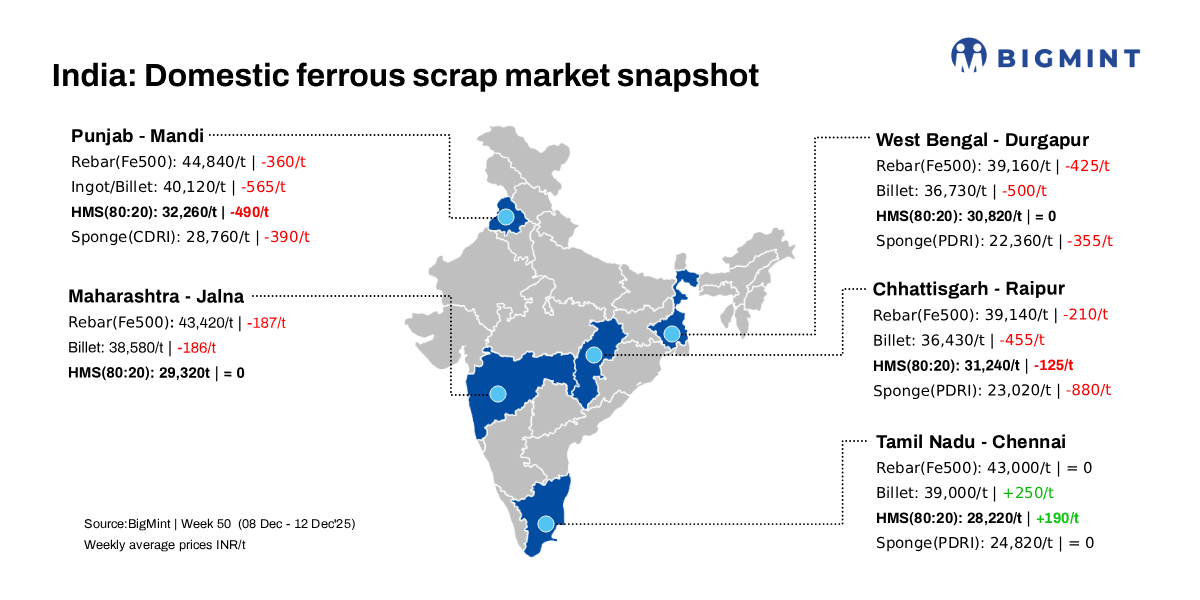

In Durgapur, billet prices softened by INR 150/t to INR 36,600/t, accompanied by a INR 200/t correction in rebar prices to INR 38,900/t. HMS (80:20) scrap prices continued to hover at INR 30,800/t, showing no major change. Market activity for finished steel remained muted, while scrap supply saw partial interruption as suppliers resisted lower bids and preferred to hold back material.

Upcoming scrap auctions

Price highlights

End-cutting to billet spread: In Mandi, the spread between end-cutting scrap and billets stood in the range of INR 4,600-4,900/t.

Domestic vs imported scrap: Imported melting scrap prices at Nhava Sheva Port were assessed at $318-$320/t, approximately INR 31,074/t (inclusive of freight). HMS (80:20) in Mumbai remained stable d-o-d at INR 30,300/t DAP. Indicative prices of shredded from Europe stood at $348-350/t CFR Nhava Sheva.

Raipur sponge iron-billet spread: The conversion spread (margin) between pellet-based DRI (P-DRI) and steel billets in Raipur stood at INR 13,550/t.

To check BigMint’s melting scrap assessment, pricing methodology, and specification documents, click here.

To check BigMint’s melting scrap assessment, pricing methodology, and specification documents, click here.

To provide feedback on this index or if you would like to contribute by becoming a data partner, please contact – support@bigmint.co

Leave a Reply