- Alternate raw material prices stable d-o-d

- Semis, finished prices dip by INR 100-200/t

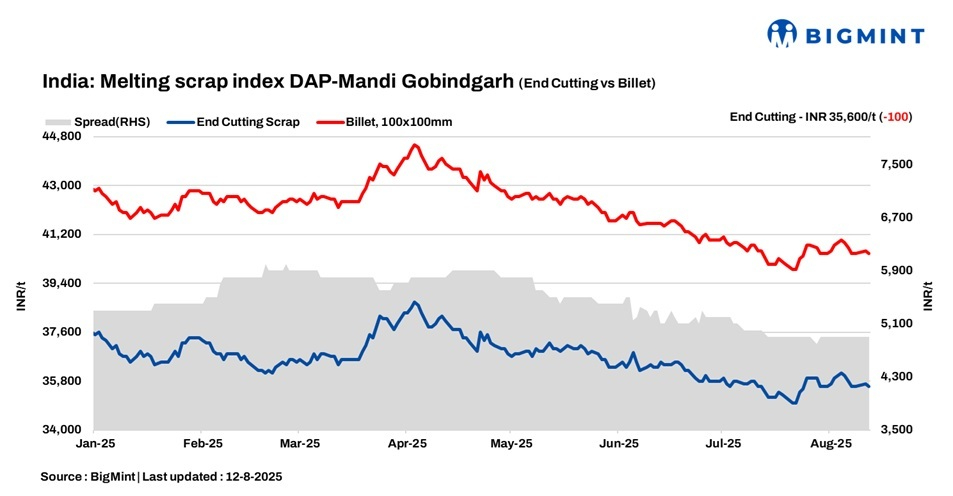

BigMint’s domestic end-cutting scrap index, tracking the Mandi Gobindgarh market, decreased by INR 100/t d-o-d to INR 35,600/t DAP on 12 August 2025.

The Mandi steel market witnessed a slight dip in scrap prices, primarily driven by weak buying activity. Additionally, persistent rainfall in the region contributed to sluggish market movement.

A mill owner informed “With a holiday expected later in the week, most mills had already secured their scrap requirements earlier, leading to reduced activity in the latter half. On the supplier side, large-volume deals remain limited, as sellers are cautious due to long credit cycles and delayed payments, exacerbated by bank closures during the extended holiday period.”

Imported scrap offer

Raw materials

Sponge Iron prices in Mandi remained stable d-o-d at INR 30,000/t DAP, indicating consistent demand in the raw material segment.

Pig iron prices in Ludhiana continued to hold firm for the sixth consecutive day, maintaining a steady level at INR 35,800/t DAP.

Steel market trend

The semi-finished steel market in Mandi Gobindgarh observed a marginal correction, with ingot prices easing by INR 200/t d-o-d, now quoted at INR 40,500/t DAP.

Across major steel-producing regions, daily price fluctuations ranged between INR 50-250/t, indicating a cautiously optimistic sentiment in the market. While the overall trend shows minor adjustments, market participants remain watchful of upcoming demand cues.

In the finished steel segment, rebar (Fe500) prices declined slightly by INR 100/t, and are currently assessed at INR 45,500/t ex-works. Overall, market sentiment remains range-bound, with minor fluctuations observed throughout the week, according to mill sources.

Overview of Jalna market

In the Jalna market of western India, billet, rebar, and HMS 80:20 prices remained steady at INR 40,100/t, INR 44,000/t, and INR 31,000/t, respectively. Recent days have seen a slowdown in trade activities for finished steel in the region. With scrap offering better availability and cost-effectiveness, mills are now using just 20–30% sponge in their production mix, shifting preference toward scrap-based inputs.

Upcoming scrap auctions

Price highlights

End-cutting-billets spread: In Mandi, the end-cutting scrap and billet spread stood at INR 4,800-5,200/t.

Domestic vs imported scrap: Imported melting scrap prices at Nhava Sheva Port were at $332/t-$333/t, which equates to approximately INR 31,392/t (including freight). HMS (80:20) prices in Mumbai remained steady at INR 31,500/t DAP today. Indicative prices of shredded from Europe stood at $365/t CFR Nhava Sheva.

Raipur sponge iron-billet spread: The conversion spread (margin) between pellet-based DRI (P-DRI) and steel billets in Raipur stood at INR 13,200/t.

To check BigMint’s melting scrap assessment, pricing methodology, and specification documents, click here.

Leave a Reply