- Certain mills adjust charge mixes amid scrap shortages

- Semis, finished steel prices remain unchanged d-o-d

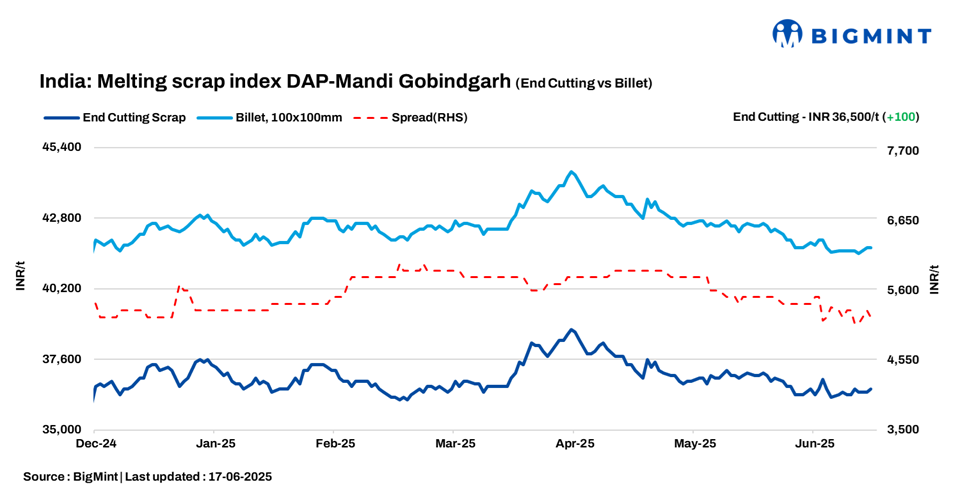

BigMint’s domestic end-cutting scrap index, tracking the Mandi Gobindgarh market, increased by INR 100/tonne (t) d-o-d to INR 36,500/t DAP on 17 June 2025.

Stringent GST inspections in Mandi significantly impacted the flow of scrap into the region, with most suppliers opting to limit high-volume transactions. As such, scrap shortages continued in the primary market.

In response to this constrained supply, medium-scale mills shifted to a 70:30 scrap-to-sponge iron ratio in their steelmaking processes to manage costs and maintain production. Meanwhile, larger mills remained reliant on scrap, maintaining an 80% scrap and 20% sponge mix due to higher melting efficiency and output quality.

Compounding challenges, slow sales in the finished steel segment led to an inventory build-up, adding further pressure on mill operations and working capital. Market participants remained watchful, as mills cautiously balanced raw material sourcing with demand-side constraints.

Alternative raw materials

Sponge iron (CDRI) prices in Mandi Gobindgarh remained unchanged d-o-d at INR 29,200/t DAP. Steel-grade pig iron prices in Ludhiana remained steady at INR 35,800/t DAP.

Steel market trends

Steel ingot prices in Mandi Gobindgarh held steady d-o-d at INR 41,700/t DAP, reflecting a balanced market with limited movements. Semi-finished steel prices across other key regions witnessed a modest decline of INR 100-200/t, driven by tepid demand and cautious buying.

Rebar prices in Mandi also remained unchanged d-o-d at INR 46,600/t exw, as trading activity stayed largely paused amid market uncertainty.

Overview of other markets

The Mumbai rebar (Fe 500) market was quiet, with prices holding steady at INR 44,300/t exw. Limited buying interest, which was driven by immediate requirements and pressured by heavy rainfall, contributed to the subdued sentiment. Meanwhile, scrap (HMS 80:20) was available at INR 30,700/t DAP, with the scrap-to-billet conversion spread at around INR 9,000/t.

The Durgapur market remained largely stable w-o-w. Prices followed a steady trend, although minor fluctuations were observed due to cautious buying activity. Demand for finished steel was weak, keeping market sentiment under pressure and contributing to price volatility. Most transactions were moderate, reflecting a careful approach from buyers who avoided large-scale bookings amid ongoing market uncertainties. Rebar prices in Durgapur rose by INR 200/t to INR 41,000/t exw, supported by a marginal improvement in buying activity. Billet prices remained unchanged d-o-d at INR 38,150/t DAP. Sponge iron (PDRI) prices witnessed a d-o-d increase of INR 150/t to INR 22,650/t DAP.

Upcoming scrap auctions

Price highlights

End-cutting-billets spread: In Mandi, the end-cutting scrap and billet spread stood at INR 5,200-5,500/t.

Domestic vs imported scrap: Imported melting scrap prices at Nhava Sheva Port were at $340-345/t, which equates to approximately INR 31,858/t (including freight). Today, local HMS (80:20) prices in Mumbai remained stable at INR 30,800/t DAP. Indicative prices of shredded from Europe stood at $360-$365/t CFR Nhava Sheva.

Raipur sponge iron-billet spread: The conversion spread (margin) between pellet-based DRI (P-DRI) and steel billets in Raipur stood at INR 14,950/t.

To check BigMint’s melting scrap assessment, pricing methodology, and specification documents, click here.

Leave a Reply