- Steel scrap prices drop INR 665-825/t w-o-w

- Semis, finished steel prices decrease by INR 700/t

BigMint’s domestic end-cutting scrap index, tracking the Mandi Gobindgarh market, declined by INR 100/t to INR 34,700/t DAP on 29 August 2025.

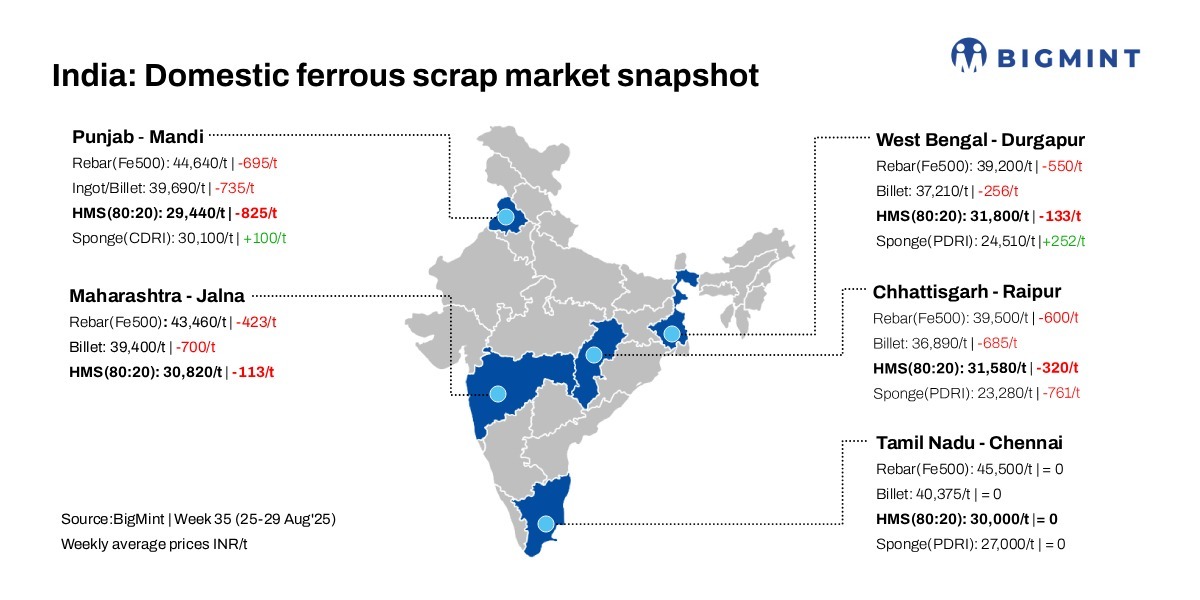

Steel scrap prices in Mandi Gobindgarh have dropped by INR 665-825/t on a weekly basis, driven by muted demand and limited activity in the market. The ongoing monsoon season has disrupted operations and further dampened sentiments across the iron and steel value chain. Both semi-finished and finished steel products are witnessing sluggish offtake, with no significant recovery in sight. Mills continue to face tepid buying interest, contributing to a bearish outlook in the near term.

Imported scrap offers face bid-offer mismatch

This weakness has filtered into Indian markets, where import offers for HMS 1 scrap from Bahrain and South Africa origins on the West Coast are being quoted at $340-342/t CFR. However, Indian sellers are offering the same material at $330/t, leading to a bid-offer disparity of around $10-12/t.

Ample inflows of domestic scrap from neighbouring states have added to the supply glut in Mandi Gobindgarh, where buying activity remains cautious. With adequate availability in the region, local buyers are negotiating aggressively, leading to subdued procurement rates. On the global front, steel market sentiment continues to be weighed down by lacklustre demand and persistent weakness in international prices, further reinforcing bearish pressure on the domestic scrap market.

Raw material

The sponge iron (CDRI) market in Mandi Gobindgarh declined by INR 100/t on the day, closing at INR 30,000/t DAP after a two-day halt. Despite this dip, prices remain INR 100/t higher w-o-w. In contrast, steel-grade pig iron prices in Ludhiana held steady d-o-d at INR 35,500/t DAP but recorded a marginal weekly decline of INR 125/t, reflecting a moderately soft tone.

Steel market trends

Semi-finished steel prices in Mandi Gobindgarh slipped by INR 200/t to INR 39,500/t DAP, tracking sluggish demand and low conversion margins. Across key production hubs, ingot prices fell by INR 100-400/t, with Mandi witnessing a weekly drop of INR 726/t, underscoring continued buyer resistance.

The finished steel segment remains under pressure as well. Rebar (Fe500) prices in Mandi fell by INR 100/t to INR 44,400/t ex-works, marking a weekly decline of INR 695/t. Mills cite lacklustre infrastructure and construction demand as key factors for the ongoing weakness.

Upcoming scrap auctions

Price highlights

End-cutting-billets spread: In Mandi, the end-cutting scrap and billet spread stood at INR 4,800-5,200/t.

Domestic vs imported scrap: Imported melting scrap prices at Nhava Sheva Port were at $332-$334/t, which equates to approximately INR 31,668/t (including freight). HMS (80:20) prices in Mumbai remained stable d-o-d at INR 30,800/t DAP today. Indicative prices of shredded from Europe stood at $365/t CFR Nhava Sheva.

Raipur sponge iron-billet spread: The conversion spread (margin) between pellet-based DRI (P-DRI) and steel billets in Raipur stood at INR 13,450/t.

To check BigMint’s melting scrap assessment, pricing methodology, and specification documents, click here.

Leave a Reply