- Spot and future iron ore fines indices drop w-o-w

- Pellet inventory at Chinese ports remains unchanged

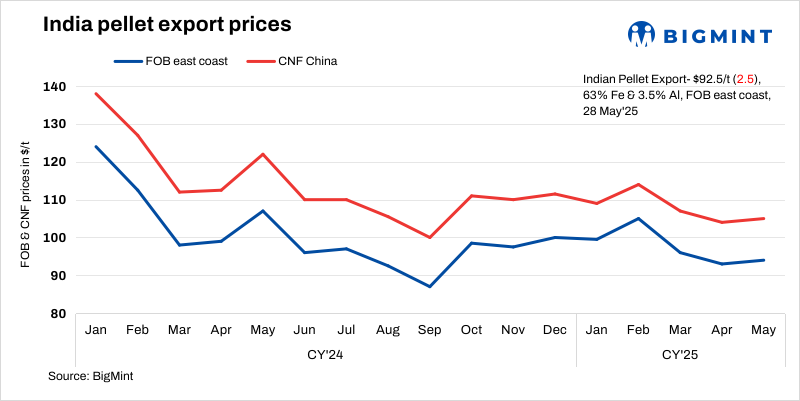

Pellet export prices from India remained under pressure this week, impacted by weaker market sentiment and a decline in both spot and futures iron ore indices.

Price update:

BigMint’s India pellet (Fe 63%, 3-3.5% Al) export index (FOB east coast) decreased by $2.5/tonne (t) w-o-w to $92.5/t on 28 May 2025 against the previous assessment on 21 May. Weaker demand for pellets from the eastern coast led to muted trades in this publishing window.

Chinese mills are currently seeking high-grade, low-alumina pellets and are securing supplies from other origins at viable prices. This has reduced the demand for Indian pellets in the export market.

Domestic vs. export market:

Indian sellers, on the other hand, are holding back on export offers, awaiting price improvement, as current bids remain significantly below workable levels. Some participants are also closely watching the outcome of a supply tender floated by a major Indian steelmaker for this month-end, which may influence short-term market direction.

Domestic prices exceeded export offers by INR 1,600/t ($19/t), with the spread widening by INR 150/t ($2/t) compared to last week, as domestic tags witnessed a drop w-o-w. Pellet (Fe63%) prices in Odisha’s Barbil were recorded at INR 7,650/t ($90/t) exw, down INR 50/t ($0.5/t) w-o-w. Meanwhile, ex-plant realisation in exports from Barbil stood at INR 6,050/t ($71/t) exw, fell by INR 200/t ($2.5/t).

Domestic pellet prices continue to offer better realisations compared to exports. However, sluggish demand in the semi-finished and downstream steel segments, coupled with elevated raw material costs, is making it difficult for sellers to conclude deals at higher price levels.

As a result, several exporters have adopted a wait-and-watch approach, refraining from concluding any export transactions until market conditions improve.

Meanwhile, recent talks of steel production cuts in China will also weigh on Indian pellet demand in the near future.

Rationale

- No confirmed deals from India’s east coast were recorded in this publishing window for T1 trade. Thus, this category was not taken into consideration for today’s price calculations and accorded 0% weightage in the index calculation. Click here for the detailed methodology.

- Nine (9) indicative prices were received, and seven (7) were considered for the calculation of the index and given 100% weightage.

Factors impacting pellet exports

Chinese iron ore fines prices down w-o-w: The benchmark iron ore fines index fell by $5/t w-o-w at $96/t CFR China on 27 May. The market has experienced notable fluctuations in recent days, with steel prices remaining low. Recent discussions about potential production cuts, along with the upcoming rainy season in China and the usual seasonal decline in downstream demand, are contributing factors to this trend.

DCE iron ore futures drop w-o-w: Iron ore futures on the Dalian Commodity Exchange (DCE) for the May 2025 contract fell by RMB 30/t ($4/t) w-o-w to RMB 698.5/t ($97/t) on 28 May. On a d-o-d basis, prices were under pressure.

Pellet inventory at Chinese ports remained almost unchanged w-o-w at 5.20 mnt on 22 May, as per data published by Steelhome.

Outlook

As per BigMint’s analysis, pellet export prices are expected to remain rangebound, and the likelihood of near-term export deals remains low unless there is a significant recovery in buying interest or price levels.

Leave a Reply