- Demand slows as Chinese mills conclude pre-holiday restocking

- Sellers focus on domestic sales due to better realisations

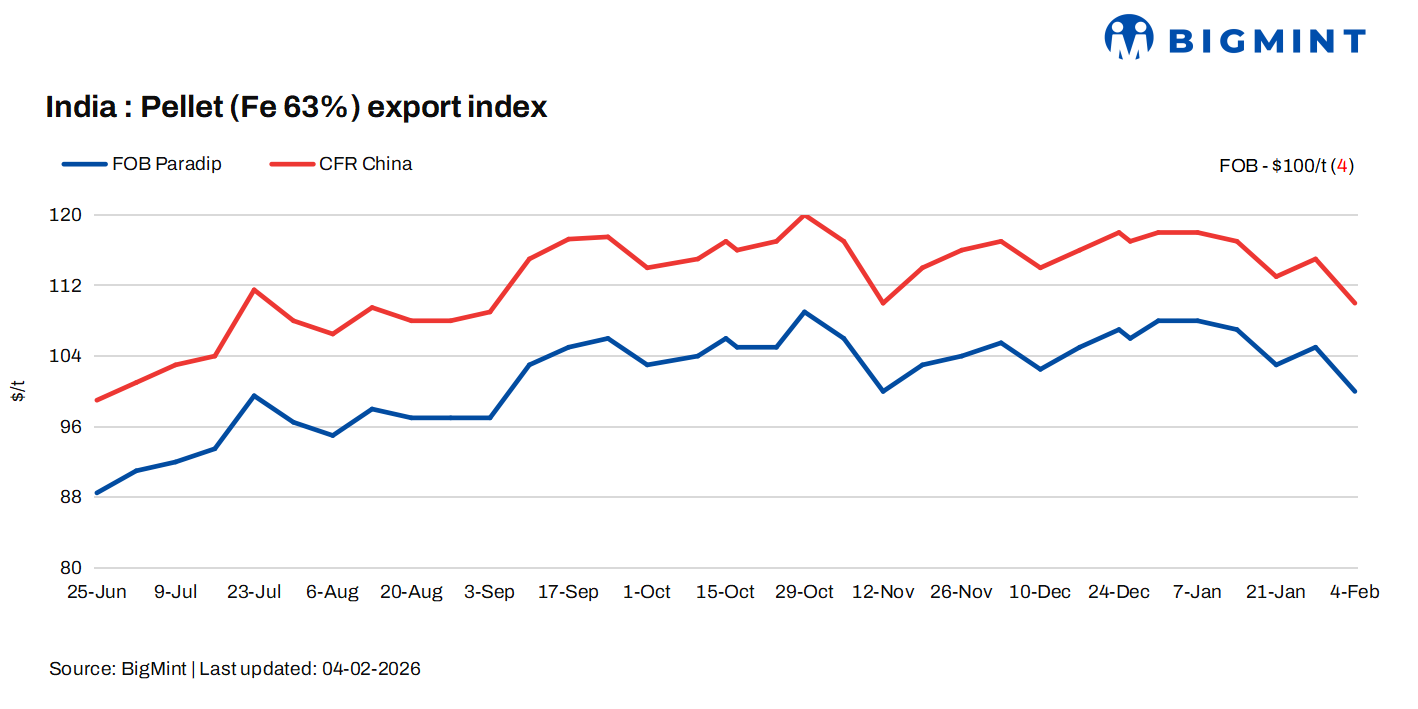

Indian pellet export prices dropped by $4/tonne (t) w-o-w on 4 February 2026 in recent export deals for higher-grade pellets. Broader market sentiment remained cautious, though improved realisations for premium-grade cargoes provided boosted overall export sentiment.

Price update

BigMint’s India pellet (Fe 63%, 3-3.5% Al) export index fell by $4/t w-o-w to $100/t FOB east coast on Wednesday. The index has hit over a two-month low as similar levels were seen in mid-November 2025.

Two pellet export deals were recorded by BigMint since the beginning of the week. One deal for 75,000 t of Fe 62.5% material from an east coast-based supplier was concluded at around $110-111/t CFR China for March laycan. Another deal for Fe 63% was concluded at $108/t FOB by a southern India-based player.

Market updates

According to industry participants, although some pellet export deals were concluded this week, sentiment weakened, driving a $4/t decline in prices. Traders said buying interest remained largely confined to cost-effective options, with Chinese mills turning increasingly cautious. An international seller said, “Deals were closed, but Chinese mills are still searching for cheaper options, especially for Fe 62-63% grade pellets.”

Sources highlighted a persistent bid-offer gap in the export market for normal Fe 63% pellets, as suppliers continued to seek higher realisations to offset firm raw material costs, while buyers resisted higher premiums. A trader informed BigMint, “There is still a mismatch between what buyers are willing to pay and what suppliers are asking for normal-grade pellets.” Traders added that the market is being pressured by falling iron ore prices in China, which has weighed further on pellet demand and capped any upward movement.

A producer noted that while higher-grade pellets saw relatively better interest earlier, overall buying has slowed as most Chinese mills have largely finalised their pre-Lunar New Year holiday restocking, reducing urgency for fresh bookings. Mills are also focusing on cost control amid shrinking steel margins, further limiting appetite for higher-priced cargoes.

Meanwhile, several Indian pellet producers are continuing to prioritise domestic sales over exports due to better realisations. A producer based in Odisha said a major share of output is being diverted for captive use, thereby restricting availability in the export market.

Domestic vs export market

Domestic prices exceeded export realisations by around INR 1,350/t ($15/t), with the gap widening w-o-w. Pellet (Fe63%) prices in Odisha’s Barbil were recorded at INR 8,750/t ($97/t) exw, falling by INR 100/t ($1/t) last weekend. The hike post OMC’s recent iron ore fines auction has supported pellet offers. Meanwhile, the ex-plant realisation in exports from Barbil dropped by INR 600/t ($6/t) w-o-w to INR 7,300/t ($81/t) exw.

Rationale

- One confirmed deal from India’s east coast was recorded in this publishing window for T1 trade but was not taken for calculation. Thus, this category was allotted 50% weightage for today’s price calculations. Click here for the detailed methodology.

- Eight (8) indicative prices were received, and seven (7) were considered for the calculation of the index and given a balance 50% weightage.

Factors impacting pellet exports

- Chinese iron ore fines prices drop w-o-w: The benchmark iron ore fines Fe 61% index edged down by $1/dmt w-o-w to $102/dmt CFR China on 3 February. Market sentiment weakened on rising port stocks, possible steel output cuts, and soft demand. Spot activity was thin after mills completed pre-Lunar New Year restocking, while falling futures kept buyers on the sidelines in expectation of further price declines.

- DCE iron ore futures soften w-o-w: Iron ore futures on the Dalian Commodity Exchange (DCE) for the May 2026 contract closed at RMB 781/t ($112/t) on 4 February, weakening slightly by RMB 4/t ($1/t) w-o-w.

Outlook

Leave a Reply